Global| Jan 25 2021

Global| Jan 25 2021German IFO Gauge Weakens Again

Summary

The IFO climate diffusion gauge fell to -0.6 in January after posting a 5.2 reading in December. The chart (tracking the IFO indexes instead of the diffusion gauges reported in the table) shows clear deterioration is afoot again. On [...]

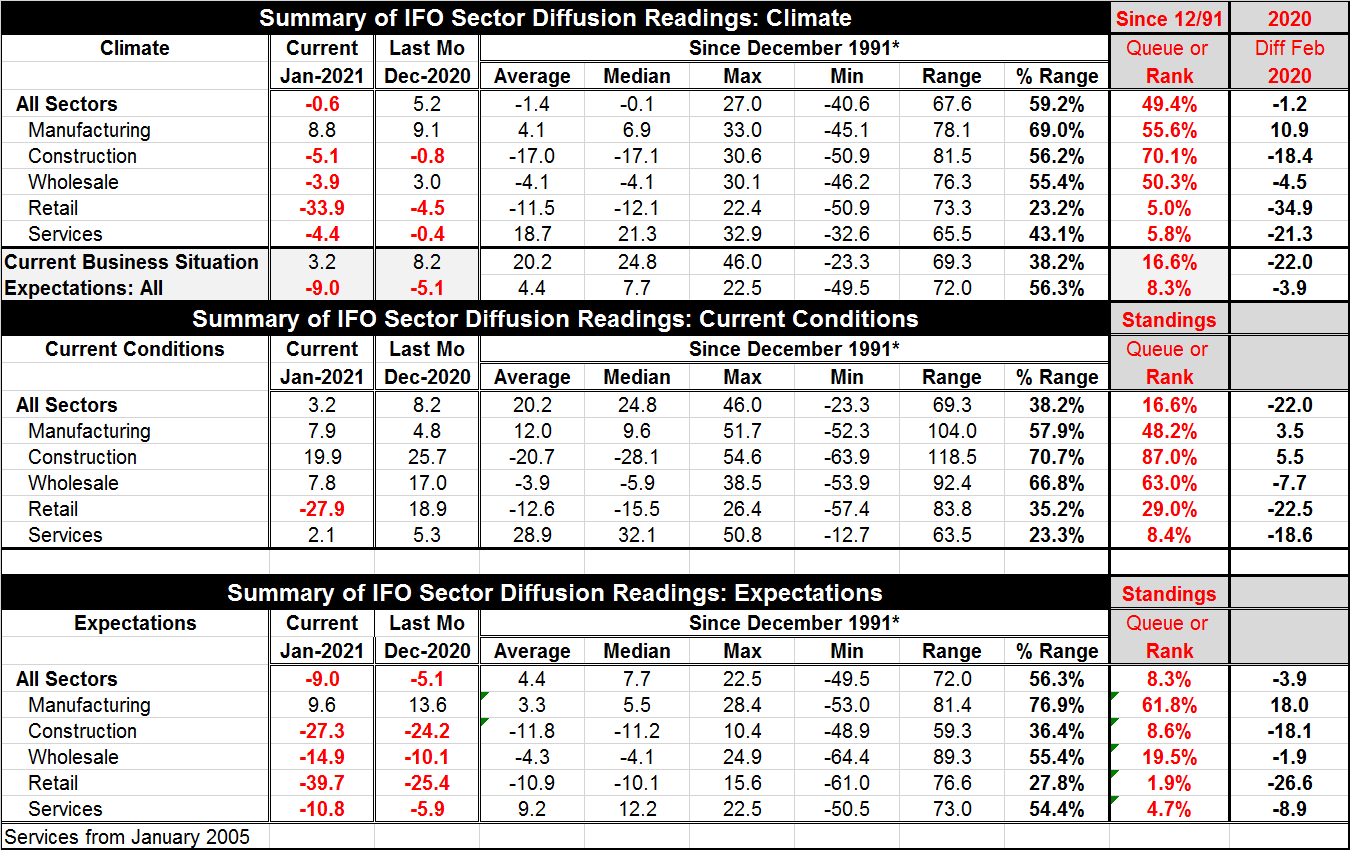

The IFO climate diffusion gauge fell to -0.6 in January after posting a 5.2 reading in December. The chart (tracking the IFO indexes instead of the diffusion gauges reported in the table) shows clear deterioration is afoot again. On the month, all industry readings eroded. Retail plunged from -4.5 in December to -33.9 in January. The services climate reading fell to -4.4 from -0.4. On data back to 1991, retailing and services have 5-6-percentile queue readings, implying that they are as bad or worse only 5% to 6% of the time. Despite weakening, three climate gauges are above the 50% mark: wholesaling, manufacturing and construction. Construction is especially solid with a 70.1 percentile standing, Manufacturing is at a 55.6 percentile standing.

The IFO climate diffusion gauge fell to -0.6 in January after posting a 5.2 reading in December. The chart (tracking the IFO indexes instead of the diffusion gauges reported in the table) shows clear deterioration is afoot again. On the month, all industry readings eroded. Retail plunged from -4.5 in December to -33.9 in January. The services climate reading fell to -4.4 from -0.4. On data back to 1991, retailing and services have 5-6-percentile queue readings, implying that they are as bad or worse only 5% to 6% of the time. Despite weakening, three climate gauges are above the 50% mark: wholesaling, manufacturing and construction. Construction is especially solid with a 70.1 percentile standing, Manufacturing is at a 55.6 percentile standing.

Current conditions weaken

Current conditions in January weakened in the IFO gauge. The weakening was broad engulfing all sectors except manufacturing; that industry moved up smartly from a 4.8 reading in December to 7.9 in January. However, the overall current index still fell to 3.2 this month after rising to 8.2 in December. The services reading weakened further by 3.2 points month-to-month, construction weakened by 5.8 points, wholesaling fell by 9.2 points, but retailing was hammered stepping back by 46.8 points month-to-month form +18.9 in December to -27.9 in January.

Expectations worsen

Expectations worsened month-to-month with the all sector index, falling by 3.9 points to -9.0 in January from -5.1 in December. Industry step backs were present across the board, ranging from a small 3.1-point reduction for construction to a 14.3-point loss month-to-month in retailing, where the expectation reading slipped to -39.7 in January.

Industry queue standings

The queue standing for the overall current index is at its 16.6 percentile with expectations at their 8.3 percentile. While expectations have a lower standing, both series are exceptionally weak. In the current index, construction and wholesaling have standings above their 50% percentile placing them above their historic medians while manufacturing comes close to a neutral reading with a standing at its 48.2 percentile. The services sector, with its 8.4 percentile standing, is the weakest current reading. Expectation’s queue standings have only manufacturing above its historic median at 61.8%. All the rest of the percentile standings in expectations are below their respective 20th percentiles with three below their respective 10th percentiles.

Since the virus struck

Comparing January 2021 levels to February 2020 finds climate lower across the board with the exception being manufacturing that is stronger by 10.9 points. The current index has a weaker all-industry headline on the basis of three weaker sectors compared to February 2020 and two stronger ones. Stronger are manufacturing and construction. Weaker are wholesaling, retailing and services. In addition to the split picture for current conditions, expectations show weakness everywhere except for manufacturing; that industry-gauge improved sharply and contrarily on the month gaining 18 points over February 2020. There is a small step down for expectations in wholesaling, a moderate deterioration for services and striking weakness in construction and retailing compared to February 2020.

The virus lingers and spreads

And none of this is surprising with the virus sweeping through Europe. The U.K. now has the highest per capita death toll. France may need a third nationwide lockdown. The Dutch are even experiencing rioting by people who resent their new curfew. So the current situation in January is being adversely impacted and as of late-January conditions appear to be worsening across much of Europe. However, at home, German cases are improving. German infections peaked on December 23; and while they are still high, the number of daily infections has been falling regularly since then. The deaths curve peak on December 29, 2020 and it has been slipping lower more gradually but that is also a steady decline. Still, Germany is worried and is projecting that the U.K. variant of the virus, a variant that is now deemed to be more virulent as well as more communicable will become the dominant strain of the virus in Germany. That keeps health officials wary despite news of trending progress.

On balance, Germany is still being hard hit by the virus and the outlook into February is not clear. The trends seem to be moving in the right direction alright. But there is concern about this variant of the virus that could alter those trends. German health officials are wary and they are keeping the economy on pause for longer. Germany lockdown measures have been extended through February 14.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief