Global| Dec 18 2018

Global| Dec 18 2018German IFO Gauge Is Weaker Than Expected in December

Summary

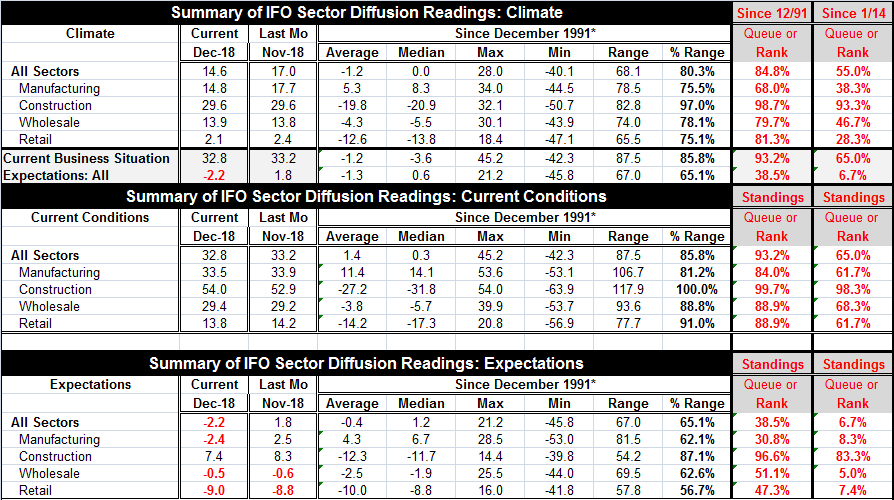

The widely watched German IFO gauge weakened noticeably in December. Most IFO readings deteriorated. The exceptions are easier to denote than listing the ones that obeyed the rule. Construction overall and current conditions were flat [...]

Should We Worry? No...But Do Pay Attention

The widely watched German IFO gauge weakened noticeably in December. Most IFO readings deteriorated. The exceptions are easier to denote than listing the ones that obeyed the rule. Construction overall and current conditions were flat or higher in December. And all three wholesaling metrics improved. Everything else crashed and burned in December.

The widely watched German IFO gauge weakened noticeably in December. Most IFO readings deteriorated. The exceptions are easier to denote than listing the ones that obeyed the rule. Construction overall and current conditions were flat or higher in December. And all three wholesaling metrics improved. Everything else crashed and burned in December.

Business climate- still overcast

The climate assessment is varied in December. While the rank standings on the longer timeline are mostly very firm-to-strong. There is an exception and that comes from overall expectations. The current business situation has a stunning 93rd percentile standing on the long timeline, but expectations have a disturbing 38th percentile standing on that same timeline. Switching gears to the shorter timeline since January 2014, we find that the all-sector assessment for climate falls to its 55th percentile from 84.8%. Manufacturing has a 38th percentile standing and retailing has a 28th percentile standing; both of these are unnerving. Wholesaling, with a 46.7 percentile standing, is below its median (for this period). Only construction is strong on the short timeline with a 93.3 percentile standing. Expectations on the short timeline are exceptionally low.

Outlook is shaky; divided: expectations

Despite the improvement in wholesaling, the sector joins retailing, and manufacturing with a negative expectations reading. Only construction has a positive sector expectation reading; even so, the construction metric deteriorated in December. The queue standings or rank standing metrics for expectations show weak readings for everything except construction. On the full period (to December 1991), the all-sector ranking is in its 38th percentile. But evaluated vs. readings back to January 2014, the all-sector standing is in its 6.7 percentile, weaker less 7% of the time! To put this in context, the chart shows that the climate readings have mostly been rising during this shorter period; thus, making it a tougher standard for comparison. In particular, there are no low 'lows' since there is no recession since 2014.

Here we want to make both points. (1) That sector indexes are quite weak by the standards we have been used to since 2014- about the last five years and the period for which readily available PMI data from Markit can be assessed. However, on a broader timeline (back to December 1991), the readings are still modest but not nearly as worrisome- at least in most cases. The full period 38.5 percentile standing for all sectors is below its median (of 50) by quite a large mark. Manufacturing has a 30th percentile standing, also quite weak. But wholesaling, despite absolute weak diffusion readings, is still above its long-term median at a standing of 51.1%. And retailing, while below its median standing at its 47.3 percentile, is close to its median- putting it close to 'normal.' Still, most of this is not really good only the construction sector to have been good and stable, resisting for the most part weakness elsewhere in the shorter period. In the short period, all expectations ranking except for construction are below their 10th percentile.

Current conditions are 'firm'

Current conditions show a differing dilemma with still quite strong and solid rank standings on the long period and much more modest conditions when compared to the environment since January 2014- modest but firm. Construction is still strong regardless of the timeline. But on the shorter timeline, sectors are all evaluated with standings somewhere in their respective 60th percentile decile (60% to 69.9%). And this is a moderate reading that is 10 to 20 percentile points above its median in terms of the standing, but not as solid as readings in the 70th percentile decile or as strong as readings in the 80th or 90th deciles. But it is not a threatening reading and is at some low point on the Goldilocks scale. Retailing and manufacturing, two very key sectors, have the weakest current standings (61.7%, both) but are still moderate.

RELAX!!

The German data and EMU data have been weakening and they are only very weak by recent standards. There has been a substantial revival in the works and analysis must allow for growth to ebb and flow. Getting overly excited about every deceleration in growth and enamored of each acceleration is not a good idea. At some point, growth comes back to average because that's what 'average' is (the fancy term is 'mean reversion'). The two columns in red on the far right in the IFO table are meant to underscore just that. The mean since 2014 is one set of numbers for these indicators while the mean since 1991 is another set of numbers. And since these are based on diffusion metrics, there is no sense that there has been any shift in the underlying trends. Diffusion simply tells the proportion of respondents where activity is expanding vs. contracting (or expected to). The percentile standings I calculate simple resolve those data into rankings to make sense of them and to allow various diffusion readings to be compared.

Various IFO metrics – nearly all show backtracking

There is a German deceleration in place. And there are many risk factors in the outlook as we have enumerated in recent reports. Risk is in the air. So is slowdown. But it is because of market reactions falling stocks and a flattening U.S. yield curve that this 'slowdown' is accompanied also with concern. And there is the uncertainty of policy, especially on trade. I am not arguing to make the theme song 'Don't worry, be happy' just to put the risk and the evaluation of conditions in their proper perspective. I hope the rankings above help you to do just that.

In the U.S., the Fed is still data-dependent. Is the Fed prepared to do that? Is it prepared to put risks in their proper perspectives or is it on auto pilot?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief