Global| Jul 27 2020

Global| Jul 27 2020German IFO Gauge Improves; Expectations Improvement Paves the Way Ahead

Summary

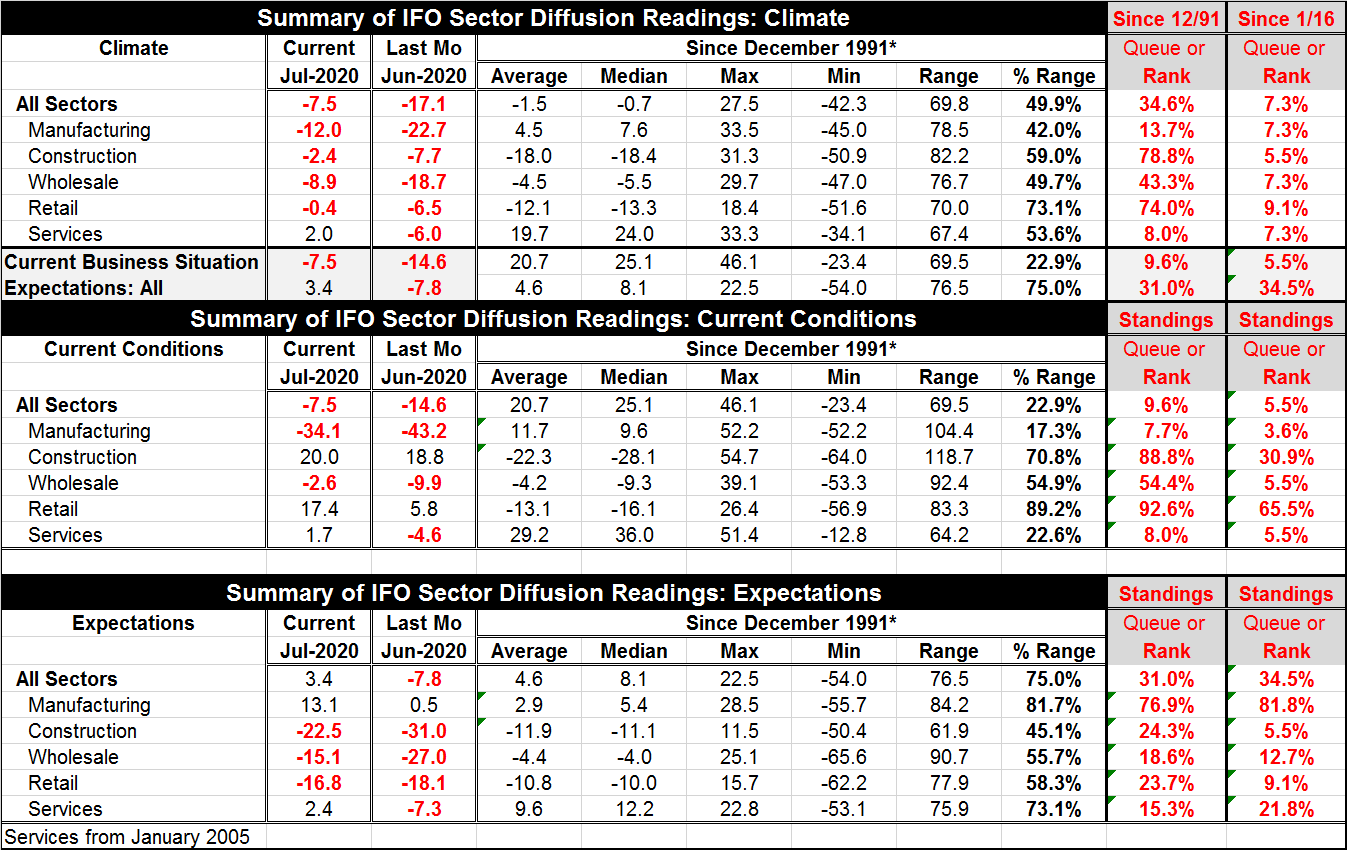

The German IFO diffusion index moved up to -7.5 in July from -17.1 in June. The queue standings of the index since 1991 is at its 34.6 percentile; since 2016 it is lower at its 7.3 percentile. On either historic comparison, it is a [...]

The German IFO diffusion index moved up to -7.5 in July from -17.1 in June. The queue standings of the index since 1991 is at its 34.6 percentile; since 2016 it is lower at its 7.3 percentile. On either historic comparison, it is a weak reading despite the sizeable monthly bounce. The index is up on gains in the current conditions index as well as the expectations index. Expectations have crossed to a net positive reading in July but still carry a below median queue ranking. The message for this month is clearly that there is some nice improvement but still a long way to go.

The German IFO diffusion index moved up to -7.5 in July from -17.1 in June. The queue standings of the index since 1991 is at its 34.6 percentile; since 2016 it is lower at its 7.3 percentile. On either historic comparison, it is a weak reading despite the sizeable monthly bounce. The index is up on gains in the current conditions index as well as the expectations index. Expectations have crossed to a net positive reading in July but still carry a below median queue ranking. The message for this month is clearly that there is some nice improvement but still a long way to go.

Economic climate stepped up with sizable improvement in all sectors- no exceptions. The overall climate index improved by 9.6 points month-to-month with manufacturing improving by the most a 10.7 point rebound. Construction improved by just 5.3 points month-to-month, the smallest monthly gain for a climate sector, but ranked over the longer period it is the strongest reading in July compared to its history of values back to 1991. And retailing that only improved 6.1 points month-to-month also has a strong historic queue standing at its 74th percentile on data back to 1991. Of course, over the shorter span (since January 2016), all rankings are lower because during this more recent period the German economy was doing so well.

The current index has moved to a 9.6 percentile standing on its longer evaluation period while expectations have climbed to a 31.0 percentile standing and posted a net positive value in July.

For current conditions, the index has improved to -7.5 in July from -14.6 in June. While the overall standing is only at its 9.6 percentile on its long period evaluation since 1991, several components like retailing (92.6%) and construction (88.8%) are actually quite strong by longer term historic standards but still only at moderate queue standings compared to where they have been since 2016. However, manufacturing and services are still substantially lagging with very low queue standings.

Expectations show across the board improvement as well. The all-sector reading has a positive value as do sector values for manufacturing and services. These are the two weakest sectors by rank in the current index. The smallest improvement expected is for retailing which has the strongest long-term queue ranking for the current index.

Clearly, the current situation is improving and expectations are advancing. The sectors that have improved the least are expected to begin to catch up. There is no evidence of overall pessimism or of sector pessimism. The virus hit world trade hard and we see that in the manufacturing indexes. However, there are still concerns in Germany about how the virus will develop and that continues to nag the outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief