Global| Feb 23 2016

Global| Feb 23 2016German Ifo Expectations Turn Sharply Lower

Summary

The Ifo index for Germany has turned sharply lower as the expectation index has weakened abruptly in February. All sector indicator weakened except for construction where spending on housing for migrants may be a stimulating factor. [...]

The Ifo index for Germany has turned sharply lower as the expectation index has weakened abruptly in February. All sector indicator weakened except for construction where spending on housing for migrants may be a stimulating factor. While expectations fell sharply, the business situation was judged to have improved on the month.

The Ifo index for Germany has turned sharply lower as the expectation index has weakened abruptly in February. All sector indicator weakened except for construction where spending on housing for migrants may be a stimulating factor. While expectations fell sharply, the business situation was judged to have improved on the month.

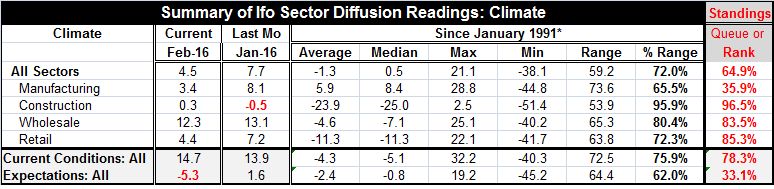

The all-sector index fell to 4.5 in February from 7.7 in January. Manufacturing fell to 3.4 from 8.1. Wholesaling fell to 12.3 from 13.1. Retailing stepped back sharply to 4.4 in February from 7.2 in January. Only construction's sector climate reading improved in February, rising to 0.3 from -0.5. The overall business situation index improved to 14.7 from 13.9 while expectations in February worsened, falling to -5.3 from 1.6. The business expectation index has fallen harder in one month only 2.7% of the time historically. The all-sector and manufacturing drops in February have been steeper only about 10% of the time. These are relatively severe one month drops.

This is a widespread show of weakness. Moreover, now a number of measures have fallen to levels that actually are weak; several sectors retain claims to ongoing strength. For example, manufacturing has rank standing in only its 35th percentile; it is weak. The all-sector index stands in its 64th percentile, a very moderate standing. Yet, wholesaling is still stronger only 17% of the time and retailing is stronger only 15% of the time. Construction is stronger less than 4% of the time. These are still quite solid readings. The business situation index is stronger only 22% of the time while the expectations index is weaker only 33% of the time.

The Ifo has become more decidedly mixed across sectors. The expectation reading is weak enough to be troubling- weaker only one time in three, historically. Yet, three sectors are still quite solid in their rankings. Only manufacturing is weak and it has taken a huge step back in February. Retailing, however, with a still strong standing, has fallen from a local peak of 14.8 in September of last year to a reading of 4.4 in February. Momentum is giving ground fast in the sector. Wholesaling was at 15.2 in November of last year and has fallen to 12.3. Manufacturing was as strong as a 12.3 reading in December and has slipped to 3.4 in February. This is a considerable amount of slippage from recent highs in these three key sectors and it underscores the loss of momentum as an additional factor to flag.

This month the ZEW index has showed slippage in step with the Ifo. Moreover the Ifo slippage is broad and actual weakness is palpable in several sectors. Still, it is `climate' that is slipping and German current conditions are still improving.

The weakening is something that is in train and that has not hit the real time economy hard, yet. But it seems about to make its impact. The climate measure by sector has fallen substantially and from recent high readings. There has been this deterioration in expectations and it seems to be creeping toward hampering the actual business situation. The business situation index has eroded. It was as high as 18.5 in August of last year. But now it is down to 14.7 even with a slight rebound this month. Germany appears to be losing momentum. If it is, that means that the ECB's planned or talked about effort at stimulus will be fighting against the tide of encroaching weakness instead of adding to other forces of forward momentum. That development will make its chance of success less likely. A weaker German economy is unequivocal bad news.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief