Global| Jul 25 2013

Global| Jul 25 2013German IFO Edges Higher in July - Still It Looks Like a Plateau to Me

Summary

The German IFO index saw the business climate reading moved to 106.2 in July from 105.9 in June, a gain of 0.3%. The current situation metric gained to 110.1 from 109.5, a rise of 0.6%. However, business expectations that are looking [...]

The German IFO index saw the business climate reading moved to 106.2 in July from 105.9 in June, a gain of 0.3%. The current situation metric gained to 110.1 from 109.5, a rise of 0.6%. However, business expectations that are looking ahead to the next six months took a setback, dropping back to 102.4 from 102.5, a loss of 0.1 percentage points. Year-over-year business climate is up by 2.9% while the current situation is weaker by 1.3% and business expectations are up by 7.2%. The business climate index is in the 76th percentile of its ordered queue, the current situation is in the mid-75th percentile of its ordered queue while business expectations are more modest sitting at about the 60th percentile of their ordered queue. In short the levels of these metrics range from moderate to relatively strong yet momentum which seems also seems moderate-to-strong over 12-months is lacking over shorter horizons. And its expectations that are more moderate and current conditions that are relatively strong.

The German IFO index saw the business climate reading moved to 106.2 in July from 105.9 in June, a gain of 0.3%. The current situation metric gained to 110.1 from 109.5, a rise of 0.6%. However, business expectations that are looking ahead to the next six months took a setback, dropping back to 102.4 from 102.5, a loss of 0.1 percentage points. Year-over-year business climate is up by 2.9% while the current situation is weaker by 1.3% and business expectations are up by 7.2%. The business climate index is in the 76th percentile of its ordered queue, the current situation is in the mid-75th percentile of its ordered queue while business expectations are more modest sitting at about the 60th percentile of their ordered queue. In short the levels of these metrics range from moderate to relatively strong yet momentum which seems also seems moderate-to-strong over 12-months is lacking over shorter horizons. And its expectations that are more moderate and current conditions that are relatively strong.

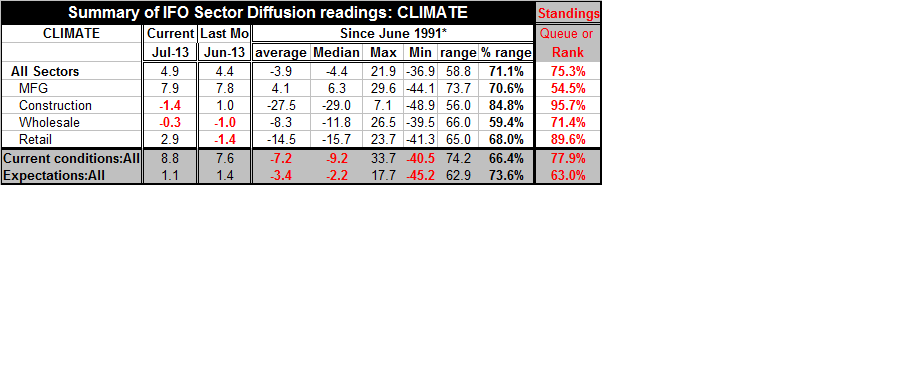

The table above looks at sectors using the up-to-date diffusion indices. The all-sector diffusion index rises this month to 4.9 from 4.4 in June. Manufacturing has edged just slightly higher to 7.9 in July from 7.8 in June. Construction reverses from a +1 reading in June from -1.4 reading in July. The wholesaling sector continues to show contraction but improves slightly with the -0.3 reading in July compared with a -1.0 reading in June. Retailing crosses the line from a -1.4 to a positive 2.9, a relatively sharp month-to-month switch in value. The diffusion metric for current conditions improves to 8.8 from 7.6 while, the expectations reading slips to 1.1 in July from 1.4, previously.

We can also evaluate the IFO diffusion indices for business climate by placing them in their historic queue or rank of values. On that basis construction is the strongest sector in the 95th percentile of its historic queue, followed by retailing at the 89th percentile of its historic queue; next in line ranks wholesaling at the 71st percentile, followed by manufacturing in the 54th percentile. The overall all-sector index is in the 75th percentile. The all-industry current conditions index sits in its 78th percentile with expectations at the 63rd percentile. These readings are roughly similar to the standings on climate current conditions and expectations derived from the index treatment in the chart above.

On balance when we look at the German economy, we see that there was a downturn in the recession and financial crisis that bottomed, depending on the sector, in late 2008 or 2009. That was followed by an expansion. The peak came somewhere around early 2011. Since then, conditions begin to slip again and a slipped until early 2012. From that point there has either been a recovery that gave way to the recent flat spot or a minor recovery and a longer flat spot. That describes the dilemma in deciding where the German economy geos next.

The retail sector's gain on the month in making the switch from -1.5 to +4.3 is a switch that is exceeded only about 20% of the time. The construction sector has eroded for four straight months. Manufacturing, after taking a sharp fall in April, as had three months of recovery but is still has not gained back when it lost in April. Wholesaling has been erratic in recent months. All this is making the economy's path a bit difficult to pin down.

The chart on the sector indices tells a good story on the pattern of recovery, which is described above. It seems to leave the German economy well below its cycle trough and still below its cycle peak but without much momentum. The Bundesbank seems to be relatively more concerned about the future now that the German economy has made its recovery from its confrontation with bad weather and some severe local flooding.

While the Bundesbank continues to have concerns about the German economy and sees weaker growth ahead, data today seem to show improvement all around (excepting construction) although most of it mild. Not only did the IFO index rise in Germany, but European signals mostly improved, too. Spain and the UK saw some improved GDP numbers in the second quarter. In the case of the UK, a stronger growth rate was posted, in the case of Spain a smaller negative growth rate emerged. In addition Spain's unemployment rate fell in the second quarter but remains at an extremely elevated level. Consumer confidence in Italy improved rising to a two-year high. Producer confidence improved in the Netherlands and the rise beat expectations there. Sweden's economic sentiment improved substantially on a rise in its consumer component. However, industrial production in Austria saw a setback.

And while there have been other indications of improvements in the euro-Zone the financial data reported out today by the ECB shows that money growth slowed and that the growth and credit also slowed this despite a survey, released yesterday, that showed that lending conditions have begun to loosen for the first time since the financial crisis.

There are not going to be any quick and easy answers to what's going on in the euro-Zone area, perhaps not even to the German economy. The Bundesbank's outlook for continued but slow growth doesn't seem very controversial when we look at the details of the sectors in the IFO survey and as we peruse the data from other countries in the Monetary Union. Even where there is improvement it is mild or to a still-weak reading.

As we continue to point out, there remain good deals of risks in the euro-Zone and around the world. Markets continue to spin higher. Corporate profits continue to put in pretty good performance and the various key global economies continue to put one foot in front of the other despite the pitfalls as commodity prices erode..

Perhaps the correct outlook is the optimistic outlook that simply concludes that the age of austerity is over and that we will now have a period where debt to GDP ratios will be given an informal 'pass' as countries try to dig their way out of their respective economic morasses. Austerity has been given a pretty long time to work and while some may think that this is the right economic path, politically it's far too long, too hard and too much uphill without enough relief. Politically, even countries that have stayed the course- and have been as true as they could to the demands of austerity - have seen substantial backsliding and a rise in their debt to GDP ratios.

Germany is losing its grip on the Monetary Union. It's very possible that we are going to see a period ahead that will have more growth and possibly more inflation although probably not initially. Worldwide economic conditions are still very slack. China is laboring although trying some patchwork policies to fill in what are some very big gaps in its economy. If we keep our optimistic hats on, and assume or presume that political crisis is not going to strike, the optimism may seem well grounded - for a while.

However, to me it's a little bit like swimming at an unknown beach with unknown currents and unknown tides without a lifeguard. It's a good idea not to stray too far from shore. The kinds of risks that lurk in the backgrounds of most of the world's major economies are of the sort that could do substantial damage -and quickly- if they were to emerge. Right now there is no doubt that investors need to set those fears aside if they're going to make money in these markets. However, the day may come when they will wish that they had been more vigilant.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief