Global| Jun 24 2016

Global| Jun 24 2016German IFO Echoes ZEW Optimism But What About Post-Brexit?

Summary

The IFO joins the ZEW index with a rise in June. But these increases came in the wake of the `polls' that were saying that Brexit would be defeated. In the event, Brexit was not defeated and the U.K. is on its way out of the EU. Much [...]

The IFO joins the ZEW index with a rise in June. But these increases came in the wake of the `polls' that were saying that Brexit would be defeated. In the event, Brexit was not defeated and the U.K. is on its way out of the EU. Much of the morning commentary from European and other sources is about how bad this will be, even from the chief of Germany's foreign trade association Anton Boerner who said "That is a catastrophic result for Britain and also for Europe and Germany, especially the German economy." "It is disturbing that the oldest democracy in the world turns its back on us" (source: Reuters).

The IFO joins the ZEW index with a rise in June. But these increases came in the wake of the `polls' that were saying that Brexit would be defeated. In the event, Brexit was not defeated and the U.K. is on its way out of the EU. Much of the morning commentary from European and other sources is about how bad this will be, even from the chief of Germany's foreign trade association Anton Boerner who said "That is a catastrophic result for Britain and also for Europe and Germany, especially the German economy." "It is disturbing that the oldest democracy in the world turns its back on us" (source: Reuters).

We can assume with some safety that the U.K. result was not discounted and is not really reflected in this survey. So the July survey could change quite a lot, depending on the weight placed on the U.K. and on the U.K. exit as a potential bellwether for other potential leavers.

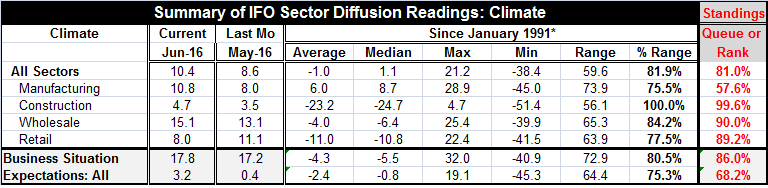

However, today's IFO survey was upbeat. The all sector index rose to 10.4 in June from 8.6 in May. The manufacturing index rose to 10.8 from 8.0. The construction sector rose to a new all-time high, rising to a diffusion index of 4.7 from 3.5. The wholesale sector also advanced to an index reading of 15.1 from 13.1. Retailing was the lone sector that backtracked, falling to 8.0 in June from 11.1 in May.

The sector rankings are high nearly across the board. The IFO all-sector index stands in its 81st percentile (higher only 19% of the time) and would be much stronger except for the very moderate standing in its 57th queue percentile for the important manufacturing index. Construction is on at an all-time high standing (this high or higher only 0.4% of the time). Wholesaling is at its 90th percentile queue standings. Retailing is at its 89th queue percentile despite its month's step back.

The overall business situation improves slightly to 17.8 in June from 17.2 in May. It has an 86th percentile standing. Expectations made a sharp rise in June to 3.2 from 0.4 in May as the standing rose only to its 68th percentile standing.

In the wake of Brexit, the U.K. and the EU will have to renegotiate their trade deals. One thing to bear in mind is that although the EU may not want to cut the U.K. cushy deal because it does not want to send the wrong signal to others who might want to leave, EU Commission does not want to kill growth in the EU and EU members also come from various EU nations. And there may be other nations considering leaving. Spain and Italy have been two members with substantial opposition talking about opting out of the EMU. And Spain's stock market took the largest drop on the day. Spain's Podemos party is a big risk and Spain faces elections this weekend.

Clearly leaving the EMU is a bigger problem than leaving the EU. Leaving the EMU would entail more of the sort of problem experienced in the Lehman shutdown as there would be many things to negotiate and to untangle that no one had really planned to untangle.

For now Brexit has hit banks hard because it has hit interest rates, foreign exchange and the financial markets hard. While it has been lost on the day's news, U.S. banks just passed their stress test yesterday with flying colors - all 33 of them. But in Europe banks have not been recapitalized. They are still largely dependent on central bank banks' backstops if there is something that goes wrong. Also bank business is being disrupted the most clearly by Brexit. All international banks have operations in London and now that is in limbo. No one knows how the EU will treat the U.K. or U.K. banking when the U.K. opts out of the EU. So that uncertainty has hit bank shares hard.

We can assume that Germany will for the most part power through this period. I still would expect some backtracking in the IFO and ZEW indices next month. And more broadly there may be more questioning of Germany's outsized influence on operations in the EU/EMU. Germany has simply created a situation where it is calling the tune. The euro area is being turned into the deutschemark area. The U.K. move to Brexit gives other countries some means to believe that they do not have to stay with that situation. That is where the risk lies for Europe but some remain in denial about this potential.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief