Global| Mar 12 2021

Global| Mar 12 2021German HICP Runs Flat as Year-on-Year Gain Steadies at 1.6%

Summary

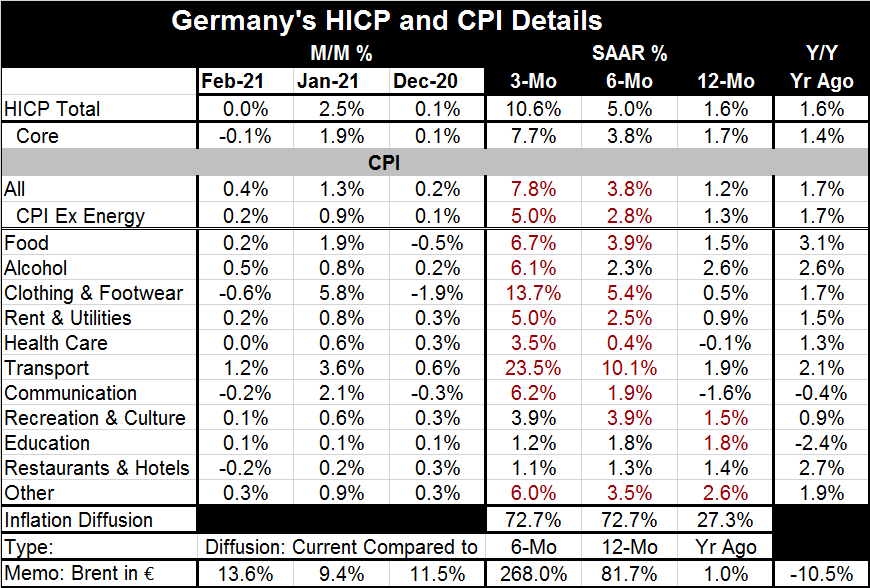

The German HICP was flat in February as the core fell by 0.1%. The German CPI went its own way rising by 0.4% in February with the core up by 0.2% month-to-month. The annual data show the HICP up by 1.6% with the core up by 1.7% while [...]

The German HICP was flat in February as the core fell by 0.1%. The German CPI went its own way rising by 0.4% in February with the core up by 0.2% month-to-month. The annual data show the HICP up by 1.6% with the core up by 1.7% while the CPI data show weaker gains on a headline rising 1.2% and the ex-energy CPI up a tick faster (just like with the HICP) at 1.3%.

The German HICP was flat in February as the core fell by 0.1%. The German CPI went its own way rising by 0.4% in February with the core up by 0.2% month-to-month. The annual data show the HICP up by 1.6% with the core up by 1.7% while the CPI data show weaker gains on a headline rising 1.2% and the ex-energy CPI up a tick faster (just like with the HICP) at 1.3%.

The trend in the price indexes looks the same for the CPI, the HICP, the HICP-core and the CPI excluding energy. In all cases, inflation rises 12-months to six-months then it rises again from six-months to three-months. These trends underline the fact that inflation is not rising just because of oil prices since the core and the ex-energy measures are showing the same trends as the respective headline measures. Sequential diffusion metrics show inflation is modest year-over-year with only 27.3% of the categories showing increases, but over six months and three months the diffusion measures rise to 72.7% in each case underlining the preponderance of inflation increases across categories in Germany since mid-year.

Nonetheless, energy prices are rising as oil (measured in euro-terms in the table) shows Brent prices are up 1% over 12 months, at an 81.7% annual rate over six months and by 268% annualized over three months. Oil prices are in fact contributing to price pressures along with other commodities and along with other factors.

Central banks want it all their way...

Christine Lagarde at the ECB has warned that sustained increases in interest rates could derail the European recovery. This in part was her explanation for why the ECB accelerated its asset purchases as its just-concluded meeting. However, with a mega-stimulus program enacted in the U.S. and inflation measures creeping up, it is hard to make the case against what global bond markets are doing. In the U.S., too, Chairman Jerome Powell has been cross-examined about why U.S. treasury yields are rising if the Fed is really so determined to show restraint until inflation runs hot and full employment is reached. Of course, in Japan, bond market bliss is obtained by a policy of yield curve control that has the central bank corralling the ten-year yield in a narrow band. Still, there is a global theme of rising inflation. Commodity prices are rising broadly and in reaction so are bond yields. Inflation is rising in Germany as the ECB is taking more aggressive stimulative action. At some point, such contrary trends will become a problem. The ECB cannot keep adding to stimulus if German inflation is rising.

Inflation in Germany is still modest, below even the gauge that the Bundesbank used to enforce when it made interest rate policy. However, the ECB sets rates in the EMU and it does look at EMU-wide inflation not just at German inflation. The pandemic puts a new spin on everything and it has interrupted business and lifestyles a lot in Germany so much so that there has been some civil unrest and protesting. Still, inflation has been restrained for a long time. And while service sectors globally remain impacted, the goods sector is more fully open for business and here supply chain issues are likely contributing to some price pressures.

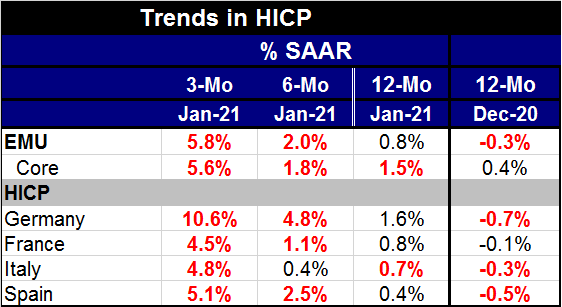

Through January, the EMU situation looks like this. Inflation is trending higher broadly, but annual inflation is still below 1% overall and in three of the four largest EMU economics. However, core or ex-energy inflation is above 1% over 12 months in the largest economies except Spain (not shown).

Policy conflicts...yet to come?

For now there are no real policy conflicts. But economic trends are not going to behave just because central bankers want them to. Markets are going to look ahead, assess and discount the action they see on the ground and in terms of price action. Policymakers are having a hard time mixing monetary stimulus with fiscal stimulus without creating a market hangover as markets worry about how that cocktail will go down. When the economies were in the grip of the pandemic and activity was plunging, markets were willing to exhibit a lot of forbearance. But as the fiscal stimulus continues to mix with monetary largesse and economic recovery, markets are beginning to see a new calculus and different risks ahead.

The period ahead

One issue here is that no one knows what lies ahead. There is no certainty about how well the vaccines will work, or if a virus variant will gain traction and undo some of the good work of the vaccinations. And then there are issues about how the vaccinations will progress. This is an issue at the moment as there is some controversy about the AstraZeneca vaccine. AstraZeneca says their product does not cause clotting. WHO supports this but several countries have halted use of the AstraZeneca product nonetheless. On top of that, there is simply uncertainty about how soon the service sectors will reopen. That is key for making sustainable growth and for reducing unemployment and under unemployment. Only so much can be accomplished trying to drive more growth through the goods sector. The future remains uncertain. Central banks are trying to conjure the best of all worlds: stimulus and growth but without a fear of inflation. It’s a high wire act without a net.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief