Global| Dec 11 2020

Global| Dec 11 2020German HICP Continues Negative Year-on-Year

Summary

No major central bank is experiencing any trouble with accelerating inflation at the moment. The virus has recirculated and that is slowing things down again keeping slack conditions present globally although also creating some [...]

No major central bank is experiencing any trouble with accelerating inflation at the moment. The virus has recirculated and that is slowing things down again keeping slack conditions present globally although also creating some sporadic price pressures for scare protective equipment. The worst days of those shortage problems, however, are past.

No major central bank is experiencing any trouble with accelerating inflation at the moment. The virus has recirculated and that is slowing things down again keeping slack conditions present globally although also creating some sporadic price pressures for scare protective equipment. The worst days of those shortage problems, however, are past.

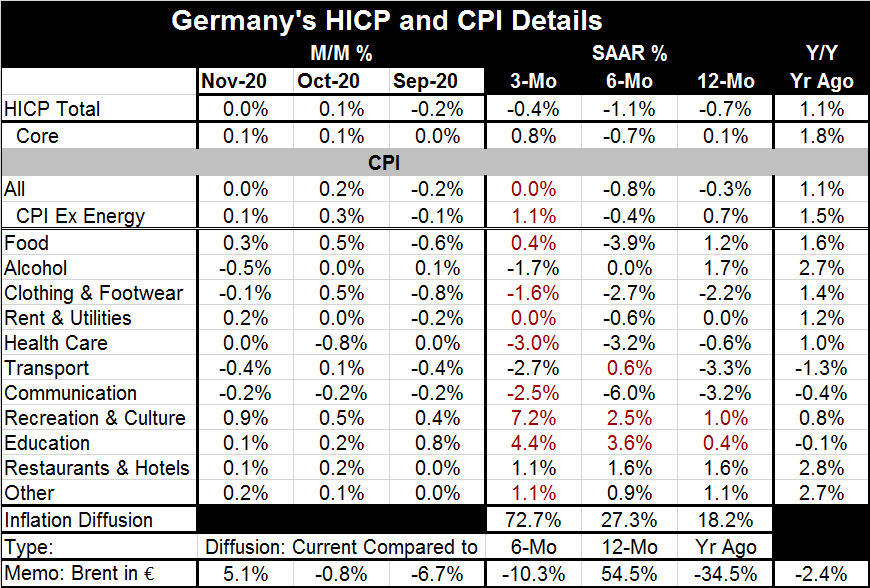

Germany's inflation data show weaker price momentum for the HICP than for the CPI. The HICP shows prices are falling over three months, six months and 12 months. The CPI shows price drops on all those horizons except over three months where prices are flat. The HICP reveals year-on-year core inflation at just 0.1% nearly negative while the German CPI excluding energy is up by 0.7% over 12 months. Any way you slice it, inflation in Germany is low, it is broadly low, and there are no clear signs of that changing. However, there are historic lingering fears.

In November of the 11 categories in the domestic CPI, only four showed price drops month-to-month. That compares to two in October and to five in September. Deflation does not seem a risk despite the year-on-year overall price drop. That has a lot to do with the ratchet lower in growth, the economic displacement by the virus, and the drop in oil and commodity prices. Oil has fallen by 34.5% over 12 months.

And we can assess inflation diffusion. By this, we look at the pace of price changes over various horizons by commodity group and ask if pressures are getting broadly stronger or weaker. The CPI shows that comparing three-month to six-month trends reveals prices rising faster over three months than over six months with 73% of categories experiencing upward inflation pressures. This is not too surprising since overall CPI prices fell by 0.8% over six months then were much less weak at 'flat' over three months.

However, over six months, we see the opposite trend. There, price trends are weakening over six months more than accelerating when compared with their 12-month trend. Inflation diffusion is only 27%. Inflation is broadly weaker of over 6-months than over 12-months Once again this is not surprising since over 12 months inflation fell by only 0.3% but fell by 0.8% over six months. And the CPI excluding energy reinforces these circumstances.

Comparing inflation over 12 months to 12-months ago also shows low inflation acceleration with diffusion at 18% (only about 18% of categories show year-on-year inflation is accelerating). Of course, over 12 months headline CPI inflation is at -0.3% while 12-months ago inflation was at 1.1%, a large step-down in its pace.

The diffusion calculations are a check on where inflation is really 'trending.' It basically checks to see whether just a few large-weighted components are driving the index or if most categories are on the same sort of trend. What we see in the German case is that inflation remains substantially and broadly decelerating. The three-month exception is not surprising- or telling- since the three-month calculation is never robust.

The last three months of data also produced inflation by month that has hugged close to zero on both major indexes. Low inflation is a broad, consistent finding whether we use more sophisticated methods or extremely simple methods to assess it.

It is fair to say that there is not much evidence of inflation in Germany – and no hint whatsoever of excessive inflation. Excess pressure simply has not existed; it does not seem to be building any momentum. Globally economic conditions remain weak; economic slack is not likely to produce global inflation pressures. This slack will help keep a lid on oil prices too; they are always a risk to drive price pressures. And the greater global sensitivity to 'green' issues could work keep oil prices on the sidelines for longer.

Eventually growth will resume as the vaccines are distributed and we will be back to a world where economic forces behave more traditionally. But we are not there now and we are not likely to be there in any reasonably policy-making horizon. As a result, inflation is off the table as a practical issue except that such a thing never happens in Germany. Of course, for real monetary policymaking, it is the ECB and EMU-wide inflation that matter. But EMU-wide inflation overall is facing the same hurdles as it is in Germany. The real problem has been maintaining growth, not suppressing inflation. And policy options to maintain growth are becoming more and more scare. Everyone everywhere really needs the vaccine to work and to start working soon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief