Global| Feb 23 2017

Global| Feb 23 2017German GfK Confidence Will Step Back in March

Summary

Despite a coming setback to German confidence in March, the GfK look-ahead confidence reading remains strong and is barely off that index's best of all-time levels. There have been three episodes in which the GfK reading has attained [...]

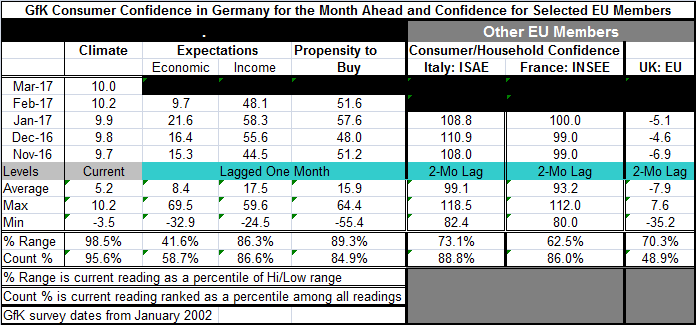

Despite a coming setback to German confidence in March, the GfK look-ahead confidence reading remains strong and is barely off that index's best of all-time levels. There have been three episodes in which the GfK reading has attained a level as high as 10. The index is expected to fall to 10 in March from 10.2 in February. September of last year was the middle month of series of readings that topped 10. And June 2015 was the middle month of another series of readings that topped 10. These are the only such occasions of such an elevated reading on headline data back to January 2002. Levels with readings as high as 10 or more have occurred only 6% of the time (and that has happened on only the three occasions enumerated above).

Despite a coming setback to German confidence in March, the GfK look-ahead confidence reading remains strong and is barely off that index's best of all-time levels. There have been three episodes in which the GfK reading has attained a level as high as 10. The index is expected to fall to 10 in March from 10.2 in February. September of last year was the middle month of series of readings that topped 10. And June 2015 was the middle month of another series of readings that topped 10. These are the only such occasions of such an elevated reading on headline data back to January 2002. Levels with readings as high as 10 or more have occurred only 6% of the time (and that has happened on only the three occasions enumerated above).

GfK releases its estimate for confidence the month ahead but does not provide any topical information on the components. The component readings are up-to-date only through February.

Economic expectations drop off sharply

In February, German economic expectations dropped sharply. In the previous four months, expectations had held values ranging from 13 to 21.6. In February the level for economic expectations fell sharply to 9.7 from January's 21.6. At its current standing, economic expectations have a queue standing that is only in the 58th percentile of its historic queue of data; that is quite a step back and quite a bit more limited than the headline which has a top-five percentile standing.

Other GfK component readings

Although the GfK headline reading rose in February before tailing in March, February saw declines in the readings for economic expectations, income expectations and the assessment of consumers' propensity to buy. However, income expectations and the propensity to buy queue standings both are relatively strong, each with mid-80th percentile standings in February.

France, Italy and the U.K.

The overall confidence standings (which are up-to-date through January) for Italy and France each show the same sort of mid to upper 80th percentile queue standings in January that the GfK components exhibit in February. The U.K. with its reading up-to-date as of January has a below median 48th percentile standing as its raw diffusion reading fell into negative territory in May of last year, eroding to a low in July. Since then, it has made some slow and uneven recovery.

Broader perspective

German GDP figures show that the German economy and private consumer spending are chugging along at a 2% rate of growth. There is really no sign of either acceleration or deceleration. Nevertheless, there is some good news as both German exports and imports are showing a bit more life. In France, the industry survey from INSEE has seen its overall barometer rise to its highest reading since mid-2011, but still only to a top 25th percentile standing on that index. Yet, France is showing a cluster of observations in the 107 to 106 index level band over the last three months that make the revival look like it is the real deal and not just a short-term recovery. Italy's 108.8 standing represents a drop from December and generally depicts a state of ongoing erosion for confidence.

Summing up

Italy is still struggling. The U.K. has outperformed expectations in the wake of Brexit vote but only because of strong BOE action and a plummeting pound sterling. In the U.K., there is accumulating evidence that the rise in import prices might finally be taking a toll on consumers. France is in the midst of a clear revival. Germany is hovering around some of its best readings ever but with hints from its components' drop off that there may be some erosion in store.

Policy

While all eyes are on the Fed since it seems poised to hike rates and the release of its meeting minutes speak to the growing likelihood of another move in the coming months, that is commanding the attention of markets. But the ECB is on hold with headline inflation surging and in defiance of Germans urging some policy shift there. So far, core inflation remains surprisingly unaffected by surging energy prices. But if the activity data for EMU begin to behave and to fall into line on the side of growth, the ECB too may begin to consider rolling up some of its extraordinary stimulus. The case for an ECB policy shift is far from clear, but apart from month-to-month oscillations there is a more general feeling that Europe is on the mend. The data simply are not consistent enough to reflect that clearly yet and meanwhile core inflation provides no motivation or sense of urgency for the ECB to move. But where there is smoke, there is likely to be fire. And headline inflation is burning up and economic activity seems to be generating some heat. It is clear which way Europe is leaning. But will that lean continue and will it become more pronounced? That's what policy is waiting for. Is it waiting for good times or Godot?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief