Global| Aug 23 2007

Global| Aug 23 2007German GDP Rebound Still Not Supported by the Consumer

Summary

Germany is a much more export oriented economy than is the United States. With the formation of the EMU, Germany was helped by having a large proportion of its trade no longer subject to foreign exchange fluctuations. Goods sold [...]

Germany is a much more export oriented economy than is the United States. With the formation of the EMU, Germany was helped by having a large proportion of its trade no longer subject to foreign exchange fluctuations. Goods sold outside Germany are still exports, but if they are sold to EMU members the currency of the transaction does not change.

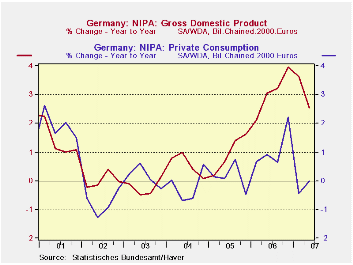

German private consumption is only 55% of German GDP. Compared to the US where personal consumption is over 70% of GDP.Also German exports are 49% of GDP whereas in the US exports of goods and service are only about 11% of GDP. The German economy has a structure very different from the US. Still at 55% of GDP the German economy needs to get the consumer involved to have its expansion last. Germany’s economy is being carried by its export strength compared to weaker imports and strong business capital formation. But it will need more for the expansion to endure. Germany like many other EMU countries continues to show that order demand outside the country is much stronger than within. Overall orders remain strong for Germany and France. For the time being the expansion still seems to be in place. But it must broaden. The risk cited recently in the Zew survey is that confidence may have been hurt by financial turmoil. This remains something to be on the look-out for in Germany as well as throughout the Euro area.

| GDP | Private Consumption | Public Consumption | Total Capital Formation | Housing | Exports | Imports | Domestic Demand | |

| % change Q/Q; X-M is Q/Q change in billions of chained 2000 euros | ||||||||

| Q2-07 | 1.0% | 2.5% | -0.7% | 10.3% | -18.0% | 3.6% | -3.5% | -2.2% |

| Q1-07 | 2.2% | -7.0% | 6.9% | 15.7% | 5.8% | -1.2% | 8.7% | 6.8% |

| Q4-06 | 4.0% | 3.4% | 0.0% | 10.8% | 6.2% | 23.0% | 5.4% | -3.6% |

| Q3-06 | 3.0% | 1.4% | 2.1% | -2.4% | 8.0% | 13.9% | 14.9% | 2.7% |

| % change Yr/Yr; X-M is Yr/Yr change in Gap in billions of chained 2000 euros | ||||||||

| Q2-07 | 2.5% | 0.0% | 2.0% | 8.4% | -0.1% | 9.4% | 6.2% | 0.8% |

| Q1-07 | 3.6% | -0.5% | 2.1% | 11.7% | 12.7% | 10.4% | 7.9% | 2.3% |

| Q4-06 | 3.9% | 2.2% | 0.9% | 7.1% | 6.6% | 16.1% | 9.7% | 0.8% |

| Q3-06 | 3.2% | 0.6% | 0.8% | 9.4% | 7.2% | 11.6% | 11.0% | 2.6% |

| 5-Yrs | 1.3% | 0.2% | 0.4% | 5.8% | -0.7% | 7.8% | 6.9% | 0.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief