Global| May 07 2014

Global| May 07 2014German Foreign Orders Drop Unexpectedly

Summary

German orders fell by 2.8% in March, an unexpected drop. The decline comes after a 0.9% gain in February and a small 0.1% increase in January. On balance, the weakness is severe enough to drive the three-month annualized growth rate [...]

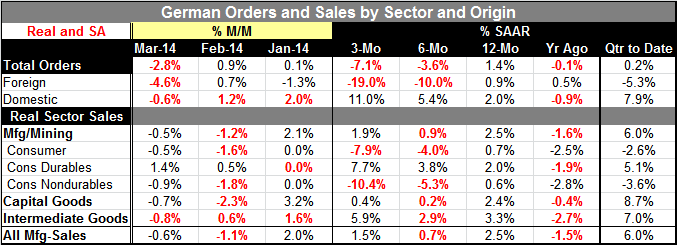

German orders fell by 2.8% in March, an unexpected drop. The decline comes after a 0.9% gain in February and a small 0.1% increase in January. On balance, the weakness is severe enough to drive the three-month annualized growth rate of orders to -7.1%. The six-month annualized growth rate is -3.6%; the 12 month growth rate is a 1.4%. These are starkly different trends than what we were looking at just one month ago.

German orders fell by 2.8% in March, an unexpected drop. The decline comes after a 0.9% gain in February and a small 0.1% increase in January. On balance, the weakness is severe enough to drive the three-month annualized growth rate of orders to -7.1%. The six-month annualized growth rate is -3.6%; the 12 month growth rate is a 1.4%. These are starkly different trends than what we were looking at just one month ago.

Is it a one-off drop or is it `Russia'?: These new growth metrics show a persistent slowdown in the growth of German orders that was not there before. The main source of the weakness is foreign orders which fell by 4.6% in March. The decline was mostly in big-ticket items, but there are concerns that the slowdown may have been related in some fashion to the geopolitical events in Ukraine. Certainly some expect a bounce back in April because big-ticket items tend to be volatile. When there's an outsized drop in one month, there frequently is a gain in the next one. But if this drop is related to orders and activities in Russia and Ukraine or if in related markets orders have been canceled or slowed because of concerns about geopolitical developments, we may find that the bounce back in April is less than expected. For now this outsized drop in foreign orders has created a three-month decline of 19% at an annual rate, a six-month decline at a 10% annual rate and it trims the year-over-year gain to just 0.9%.

At the same time, domestic orders seem to be largely unaffected. They declined by 0.6% in March but after a 1.2% gain in February and a 2% gain in January. Orders domestically are growing and accelerating. The three-month growth rate is 11% at an annual rate compared to 5.4% over six months and 2% over 12 months. This is a nice steady revival and so far seems unaffected by the crankiness and downturn in foreign orders.

Real sector sales show a slowdown and a drop of 0.5% in March on the heels of a larger drop in February. Still, three-month real sector sales in mining and manufacturing are growing at a 1.9% rate, up from a 0.9% pace over six months but below its 2.5% pace over 12 months. Nonetheless, these growth rates are relatively stable and positive. The weakness in real sector sales comes from overall consumer goods, led by weakness in consumer nondurables sales that have declined for two consecutive months, driving the three-month growth rate for nondurables to a -10.4% annual rate drop. The six-month rate is a -5.3% annual rate drop. Over 12 months, there is a small increase of 0.6%. For the most part, real sector sales are still expanding. Capital goods and intermediate goods sales fell in March, but for each the three-month growth rate is still positive; both sectors are showing relatively steady growth although unspectacular growth in the case of capital goods.

German orders are somewhat unsettling for Europe because Germany has been a juggernaut of growth if not of strength. The German economy doesn't always post the strongest numbers; however, in an environment where most of the rest of the economies have had more severe declines in industrial production and still weak domestic demand, Germany has continued to power ahead even if only in first or second gear. Everyone will have their eyes glued to German orders in April. At that time we'll find out if the decline in March was one of those declines brought on by the lumpiness of big-ticket items or whether there is something perhaps more severe in train related to geopolitical events in the region. German businessmen have been lobbying the government for no further sanctions on Russia. Perhaps where there is smoke, there is fire?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief