Global| Oct 16 2008

Global| Oct 16 2008German Firms Cut Back Their Assessment and Expectations

Summary

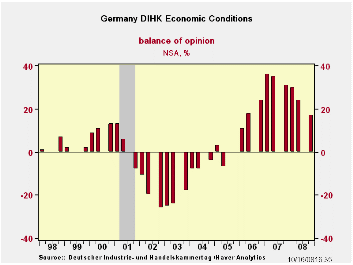

The German Chamber of Industry and Commerce survey (DIHK) shows a steady if not rapid deterioration in the current assessment and in the expectations for the period ahead. Economic conditions slipped from a reading of +24 in Q2 to +17 [...]

The German Chamber of Industry and Commerce survey (DIHK) shows a steady if not rapid deterioration in the current assessment and in the expectations for the period ahead. Economic conditions slipped from a reading of +24 in Q2 to +17 in Q4 dropping their standing to the 69th percentile from the 80th percentile previously. Business expectations dropped from +6 to -9 as the percentile standing fell to the 41st percentile from the 76th percentile, a sharp drop off and a move away from a nice position above the range midpoint to substantially below it.

Investment intentions have also crossed into negative territory, dropping from +6 to -2. But in terms of the percentile standing, the drop off is not as severe as the percentile fall from the 78th to the 60th percentile still leaves a firm reading in place not one that is below average. A modest negative number is still above the mid-point response for German firms’ capital spending intentions. Hiring intentions also fell to a negative reading from +6 in Q2 2008 to -3 in Q4 2008. Similarly the percentile ranking fell from the 86th to the 66th percentile for hiring plans.

The survey was conducted in late September and early October so some of the worst of the recent financial markets events were probably not taken into consideration in the survey. However in mid and late September the stock market was extremely choppy and volatile. It is unclear how much of this affected respondent expectations and assessments.

In the survey German firms also expressed more concerns about foreign growth and with that diminished expectations for German exports.

| DIHK-Balance of Economic Opinion | ||||||||

|---|---|---|---|---|---|---|---|---|

| Net Balance Readings | Change | Range Q4'91 | Percentile | |||||

| Q4-08 | Q2-08 | Q1-08 | Yr Ago | 2-Yr | 3-Yr | Q4-08 | Q2-08 | |

| Economic Conditions | 17 | 24 | 30 | -14 | -7 | 17 | 69.4 | 80.6 |

| Business Expectations | -9 | 6 | 10 | -24 | -18 | -12 | 41.1 | 67.9 |

| Export Expectations | 14 | 26 | 36 | -25 | -21 | -18 | 54.8 | 74.2 |

| Investment Intentions | -2 | 6 | 9 | -15 | -9 | 4 | 60.9 | 78.3 |

| Hiring Intentions | -3 | 6 | 7 | -12 | -3 | 11 | 66.7 | 86.7 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief