Global| Apr 06 2005

Global| Apr 06 2005German Factory Orders Fall in January, February, But Big December Gain Still Promotes Forward Momentum

Summary

German factory orders declined in February, with domestic and foreign customers both pulling back. This was the second successive monthly decrease, although these followed a widespread jump in December. The Ministry of Economy and [...]

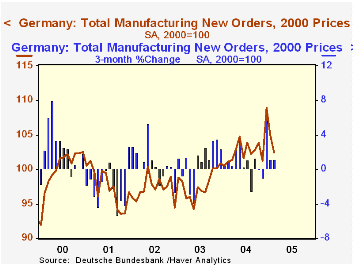

German factory orders declined in February, with domestic and foreign customers both pulling back. This was the second successive monthly decrease, although these followed a widespread jump in December. The Ministry of Economy and Labor reports that total orders were off 2.6% in February, following a 3.5% drop in January and a 7.6% surge in December.

Press reports of these data emphasize the two latest monthly declines, attributing them to higher energy costs and Germany's high level of unemployment. These factors may eventually drag down the German manufacturing sector. But for the time being, reductions in these last two months are probably better seen simply as reactions to the big gain in December. Foreign orders especially are still 4.1% above November's amount.

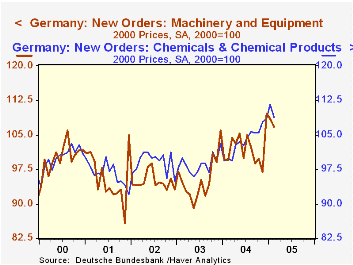

Further, among industries, the key machinery sector is holding that late 2004 level better than most others. Total orders for that group in February were 10.2% above November, with the domestic portion 1.9% higher and foreign 16.8% (simple point-to-point percent changes, not annualized). Foreign orders for machines were actually stronger in January than December so a modest setback in February was hardly noticeable. Some industries are weakening, to be sure, especially metals, nonmetallic minerals, rubber and leather. Flat trends are evident in wood products, electrical equipment orders from domestic customers and "other" manufacturing. Notably, though, chemicals, a sector that often reacts sharply to petroleum prices, has continued a dogged uptrend until a 2.5% decrease in February.

So a clear pattern is not apparent in German manufacturing. Some analysts argue that the persistent gains in the foreign sector will lift all of industry in coming months, actually helping eventually to lower unemployment; this is the opposite chain of events foreseen by others, who suggest that high unemployment will pull down all of the German economy. Stay tuned.

| Germany (% chg, SA) | Feb 2005 | Jan 2005 | Dec 2004 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| New Orders | -2.6 | -3.5 | 7.6 | 1.3 | 6.4 | 0.6 | -0.3 |

| Domestic | -2.8 | -6.3 | 8.0 | -2.9 | 4.3 | -0.1 | -3.4 |

| Foreign | -2.3 | -0.4 | 7.0 | 5.9 | 8.9 | 1.5 | 3.5 |

| Sales (includes Mining) | 0.1 | 2.8 | -2.1 | 1.2 | 4.8 | -0.5 | -1.7 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief