Global| Jun 06 2014

Global| Jun 06 2014German Exports Surge ahead and Balloon Trade Surplus

Summary

German exports surged by 3% in April as imports edged ahead by just 0.1%. This combination sent the German trade surplus to ?17.7 billion in April, up from ?14.99 billion in March. Over 12 months. German exports and imports are [...]

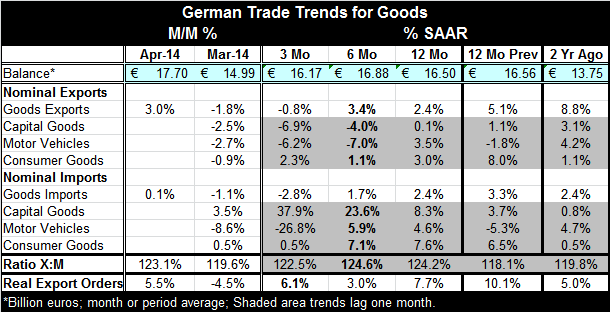

German exports surged by 3% in April as imports edged ahead by just 0.1%. This combination sent the German trade surplus to ?17.7 billion in April, up from ?14.99 billion in March.

German exports surged by 3% in April as imports edged ahead by just 0.1%. This combination sent the German trade surplus to ?17.7 billion in April, up from ?14.99 billion in March.

Over 12 months. German exports and imports are roughly balanced with each having a 2.4% growth rate. However, because the German trade position is in surplus equal growth rates for exports and imports make the year-over-year surplus bigger.

Export growth shifts from a 2.4% annual growth rate over 12 months to a 3.4% growth rate over six months to a -0.8% growth rate over three months.

Import growth rates shift from a 2.4% annual growth rate over 12 months to a 1.7% growth rate over six months to a -2.8% growth rate over three months.

A steady deceleration with import growth rates, just mentioned above, is not what we have been looking for from the German economy. As it has been strong, we had expected German domestic demand to grow and provide some stimulus for its trade partners, particularly for its fellow partners in the European Monetary Union. However, this transition has still not occurred.

German exports also show deterioration, but the pattern is not so clear. The export growth rate rose over six months and then declined over three months; the three-month growth rate is below the 12-month growth rate. Still, there's no constancy to export trends. We can't be sure where German exports are headed. The sharp rebound in April makes us less inclined to think that German exports are really decelerating. In the bottom of the table, it shows that real export orders have jumped back to a 6.1% growth rate over three months from a 3% growth rate over six months. However, the real orders growth rate for three months is slightly below the growth rate for 12 months.

The detailed statistics on exports and imports lag by month; to create three-month, six-month, and 12-month growth rates for the components, we use one-month lagged data. As you can see in the table, we have sector detail only through March although we have aggregate figures that are topical through April.

The detail on exports shows pronounced weakness in capital goods which tends to be a strong sector for the German economy. We have also seen sharp declines in real sector sales of capital goods for Germany. Motor vehicle exports have been slowing. Although consumer goods exports have stabilized to some extent at a 2.3% growth rate over three months, that rate is bracketed by a weaker six-month growth rate and a stronger 12-month growth rate.

For imports we see a great deal of strength in capital goods with imports of capital goods growing progressively stronger from 12 months, to six months, to three months. Motor vehicle imports are up slightly year-over-year, but down sharply over three months. Consumer goods imports have slowed sharply over the recent three months but still show a relatively strong year-over-year gain at 7.6%.

The rebounding exports and the ongoing strength in German export orders suggest the German exports are going to stay on the expansion path. However, for imports, weak tends are in play.

The German economy shows some odd things happening with the German capital goods sector. Real sector capital goods sales are week. German capital goods exports are weak. German capital goods imports are strong. This is a puzzle for the German economy. Although the capital goods sector is often much stronger in the earlier parts of the economic cycle, the kind of weakness we are seeing in this sector in terms of sales and exports now is surprising and seems uncharacteristic of the German economy where capital goods is normally the leading sector.

Germany continues to grow. But like other European economies, its performance has been somewhat uneven. The Bundesbank has increased its outlook for growth this year slightly and has reduced its outlook for inflation, in line with the European Central Bank's outlook for inflation in the EMU as a whole. This month, France has also reported out statistics with weak imports that have had the impact of shrinking its trade deficit. We continue to see these sorts of problems in the euro area. Trade deficits are reduced due to weak domestic demand more than due to export strength. The EMU countries that have been struggling continue to struggle. It's not exactly that the rich are getting richer and the poor are getting poorer, but the poor are not making the progress we would expect and want them to make.

Beyond Germany

At his press conference this week, ECB President Mario Draghi noted that austerity had been imposed in a number of countries because they had price level differences with the rest of the euro area. He also remarked that fixing the price level difference is a one-time affair. He did not say that the price level differences within the euro area had been resolved, and we know that they have not been fixed. But he did urge the countries that are emerging from austerity to stay on the right path, noting that going back is not a solution.

With the ECB trying to offer additional support, there may be some cause to be more optimistic on the outlook for the EMU as a whole. However, at his press conference, Draghi noted that the bank's outlook for this year had been reduced and that the outlook for growth in 2015 had been increased. Like the inflation profile at the Fed, Draghi does not see inflation in the euro area getting back to normal for a number of years.

While the ECB is putting a lot of change on the table and keeping its options open, it's not clear that the monetary steps being taken are going to be sufficient. With ongoing fiscal restraint in Europe and lingering banking sector issues, there may still be insufficient loan demand. The ECB may be trying to provide financing tied it to banks making the "right" kinds of loans, but supply does not automatically create its own demand. The ECB is trying to get loans to private nonfinancial corporations in gear; it's not trying to stimulate loans to governments.

The success or failure of the ECB will have a lot to do with how growth progresses in the EMU. While Europe's banks are still in some difficulty, the extra funds may help them to conduct business. I would be skeptical that there's going to be any pickup in credit growth in the EMU just because of the new actions by the central bank. Its rate moves were small and its credit moves may not be that effective. What we see in the United States, in the wake of quantitative easing, is a tremendous allotment of excess reserves in the banking system. These are reserves in excess of what banks have to hold. This situation demonstrates that the extra liquidity provided by the Federal Reserve has fallen far short of stimulating loan demand for it. It's likely that the ECB will encounter the same sort of difficulty. You can lead a bank to liquidity, but you can't make it lend.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief