Global| Sep 08 2015

Global| Sep 08 2015German Exports Spurt in July

Summary

German exports surged by 2.4% in July, more than offsetting the 1.1% drop in June. The euro exchange rate continues weak, bolstering German exports. Exports are outpacing imports handily over three months and six months. But year- [...]

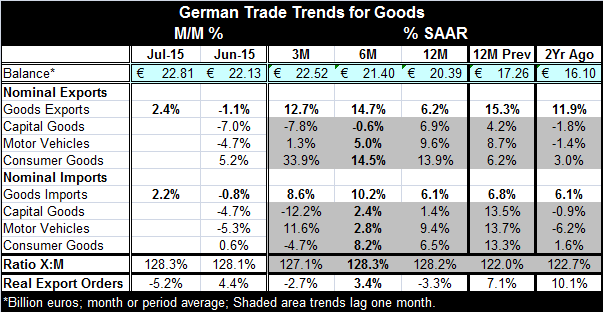

German exports surged by 2.4% in July, more than offsetting the 1.1% drop in June. The euro exchange rate continues weak, bolstering German exports. Exports are outpacing imports handily over three months and six months. But year-over-year exports are faster than imports by the tiniest of margins; exports are up by 6.2% and imports are up by 6.1%. Exports and imports have built momentum although not as a steady pattern of acceleration. But export and import three- and six-month rates of growth are well above their respective 12-month rates of growth.

German exports surged by 2.4% in July, more than offsetting the 1.1% drop in June. The euro exchange rate continues weak, bolstering German exports. Exports are outpacing imports handily over three months and six months. But year-over-year exports are faster than imports by the tiniest of margins; exports are up by 6.2% and imports are up by 6.1%. Exports and imports have built momentum although not as a steady pattern of acceleration. But export and import three- and six-month rates of growth are well above their respective 12-month rates of growth.

Germany continues to have export-led growth and the largest trade surplus relative to GDP among large economies. The ratio of German exports to imports is at 128.3% in July, up from 12 months ago, 24 months ago, and 36 months ago. Germany's trade surplus is at 22.8 billion euros in July, compared to 20.4 billion euros 12 months ago, 17.3 billion euros 24 months ago, and 16.1 billion euros 36 months ago. The growth in the surplus has slowed over the past year.

The fly in the ointment for Germany is that real export orders do not show the strength that we see in exports themselves. Real export orders are lower by 5.2% in July and down by 2.7% at an annual rate over three months. Real orders are up over six months but down by 3.3% year-over-year. Export orders, especially year-over-year orders, tend to track actual export growth well.

The problem is that while German export growth is solid, export orders imply that the strength is fleeting. We know that Germany is the most competitive economy in the euro area and that a dropping euro exchange rate has further enhanced German competitiveness abroad. But Germany has also been one of the countries that has focused on trade with China and has benefited from China's rapid growth. Now China is slowing; that slowdown could hit German exports hard. Also since German exporters have targeted the high end of the Chinese market, the new emphasis on corralling corruption could make highly visible high-end goods less attractive to own. Moreover, exporting is not just about competiveness; there must also be demand. German exports are trying to make headway against gale force global winds. The export order series tells us that German progress is about to slow despite German competitiveness and exports' own trend.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief