Global| Mar 10 2016

Global| Mar 10 2016German Exports Fade Again

Summary

Despite the overwhelming competitiveness of the German economy inside the euro area and despite the very weak euro, itself which makes all of the euro area countries very competitive in their trade outside the zone, German exports [...]

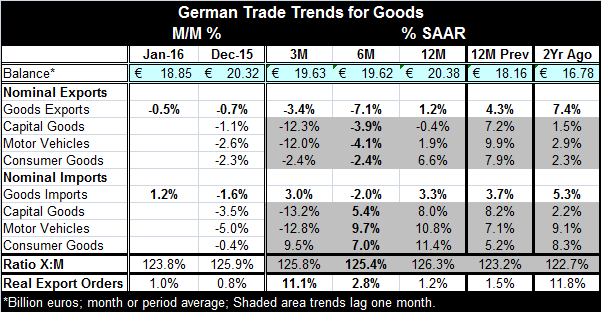

Despite the overwhelming competitiveness of the German economy inside the euro area and despite the very weak euro, itself which makes all of the euro area countries very competitive in their trade outside the zone, German exports dropped in January on surprisingly broad fronts. The huge German trade surplus fell to 18.85 billion euros in January from ?20.32 billion euros in February. What we are seeing in this report is how activity (weak activity) trumps competiveness. Being extremely competitive in a time of very weak growth does not pay much in the way of dividends. As a result and without intent, Germany is becoming a true `locomotive for growth' importing faster than it is exporting over 12 months, six months and three months

Despite the overwhelming competitiveness of the German economy inside the euro area and despite the very weak euro, itself which makes all of the euro area countries very competitive in their trade outside the zone, German exports dropped in January on surprisingly broad fronts. The huge German trade surplus fell to 18.85 billion euros in January from ?20.32 billion euros in February. What we are seeing in this report is how activity (weak activity) trumps competiveness. Being extremely competitive in a time of very weak growth does not pay much in the way of dividends. As a result and without intent, Germany is becoming a true `locomotive for growth' importing faster than it is exporting over 12 months, six months and three months

German demand and imports are steadier in this environment with nominal growth rates hovering around 3%. But German exports are falling on balance over three months and six months and post an increase of just 1.2% over 12 months.

Germany's ratio of exports to imports is slipping as imports gradually gain on exports.

Geographical patterns in German trade

The German statistical agency tells us this about intra EU and EMU trade flows for goods in January. I have added some description to their web site data. Compared with January 2015, exports to the EU countries increased by 1.0%, and imports from those countries by 3.0%. So the trade balance for intra EU trade worsened. Goods to the value of 34.3 billion euros (-0.1%) were dispatched to the euro area countries in January 2016, while the value of the goods received from those countries was 33.3 billion euros (+2.7%). The trade balance within the EMU also worsened. In January 2016, goods to the value of 20.4 billion euros (+2.9%) were dispatched to EU countries not belonging to the euro area, while the value of the goods which arrived from those countries was 15.1 billion euros (+3.8%). With those flows, the trade balance with EU countries not in the EMU also worsened. Germany saw trade deterioration on all those balance accounts: for all of the EU, for the EMU, and for EU countries not in the EMU.

Trade results outside of Europe is worsening

Germany has also seen balance deterioration on trade flows outside of the EU area. Exports of goods to countries outside the European Union (third countries) amounted to 34.0 billion euros in January 2016, while imports from those countries totaled 26.7 billion euros. Compared with January 2015, exports to third countries decreased by 5.0% and imports from those countries fell by 1.1%. There is still a surplus on this account, as there is on all the other regional breakdowns, but it is eroding.

We see deteriorating exports to third country markets (outside the EU area) and declining imports from them. This evidence of some extreme weakness (as well as of weak oil prices) as foreign markets are exporting and importing less in their trade with Germany - both sets of flows are being impacted. This underscores the weakness in the global economy.

The commodity composition of trade

The commodity composition of trade figures lag by one month, but they still echo the weakness of the more topical headlines. Note that since components lag the headline by one month, that component periods (three-month, six-month and 12-month) are slightly mismatched with the headlines). Component export flows are weak on broad front over the last three months and six months. Import components show mixed weakness over the last three months and then show more resilience over six months and 12 months (remember on a different time line from the headline).

Signals about the future remain mixed

Still, German real export orders show not just resilience, but also strength as they are up by nearly 1% in each of the last two months and grow at an annualized pace of 11.1% over three months. Thus, data on the future remains mixed in its signaling.

Judging EU health from manufacturing production data

Base on fragmentary EU-wide data, manufacturing in the EU is mixed. German IP was strong in January (3.2%), but that was cited as a weather effect. There are as of right now seven early reporters of EMU manufacturing and three of them show significant declines in January (Finland, Spain and Malta). On the upside, Ireland shows an off the charts gain; Germany shows a strong (distorted?) gain; and France and Portugal show solid months gains at 0.8% month-on-month. Two of three EU-only members show gains; one shows a sizeable IP drop. Still, in December, 14 EU countries report and show output declines in manufacturing for six nations with output flat in two more (8 of 14 disappoint). Momentum is not particularly good. Over three months, these EU reporters show five declines and two instance of flatness out of 10 reporters. Four of 10 still show year-over-year manufacturing output declines. These trends do not reassure.

The current state of Europe as the ECB acts

While we have to admit to a mixed picture here, it is also mixed with a great deal of weakness. There are too many instances of output falling to be reassuring. The ECB today cut its repo rate by 10 basis points and upped its monthly `QE' allotment to 80 billion euros from 60 billion euros. But experience with QE at low rate levels is not very extensive. While the ECB seems reluctant (given warnings by the BIS) to dig deposit rates into too deep of a negative hole, QE acts to do just that at these rate levels with a broader array of securities. As interest rates eventually rise, the ECB will lose money on these operations; that seems clear. It is clearly operating in very muddy, shallow and troubled waters.

Germans are in opposition to everything! Just let bad things happen!

Germany has opposed most of these moves and used delaying tactics. Germany will probably howl and say "I told you so" when the chickens come home to roost and the ECB has to take a loss on these operations. However, it is the delays forced on this policy by the Germans themselves that have made the programs ineffective.

It is also the German insistence on enforcing Maastricht debt and deficit rules that have put fiscal policy off limits and out of reach and put the monkey on the back of the ECB. The ECB is a bank which still shows no sign of reaching its inflation objective after all these moves. Germans should be concerned about this. But their `view' of the inflation objective is that it is not just a bit less than 2%, but that the `target' is `less than 2% or less than that.' The Germans are not unhappy with the ECBs results. They can cope. But this performance still sticks in the craw of nearly every other EMU member and the poor target-hitting erodes ECB credibility. It's long past time for the Germans to take their foot off everyone's throat and allow some fiscal stimulus. Germany's obstreperousness reached a peak of irrationality this last week as it insisted that Greece should be evaluated on its budget hitting or missing with no allowance for the expenditures on the migrants that have flooded the country. That is not just closed minded; it is mean-spirited. And it rather sums up the policy attitude in Europe today. Europe is house divided. The U.K. is deciding whether to divide it up further.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief