Global| Apr 26 2007

Global| Apr 26 2007German Export and Import Prices Show Relief

Summary

Germany has long been a bastion of inflation fighting. Ever since the post war hyperinflation raged, sapping German spending power, Germans have been alert and vigilant against the rise of inflation. The Bundesbank long was charged [...]

Germany has long been a bastion of inflation fighting. Ever since the post war hyperinflation raged, sapping German spending power, Germans have been alert and vigilant against the rise of inflation. The Bundesbank long was charged with that job. But when the monetary union was formed in Europe a central bank of central banks was to take control and the question was raised as to who would run it...and how.

Early conflict on the issue was decided by the two largest Euro members. The Germans, wanting to root the ECB and the euro in the same stability as the Bundesbank and the Deutschemark, pushed for an ECB located in Frankfurt with a research head drawn from the staff of the Bundesbank. France wanted the honor of having the first central bank head. But France’s pick, Jean-Claude Trichet, was embroiled in a controversy stemming from his tenure as head of the Bank of France and was still under investigation at the time the ECB was formed. Europeans were adamant that someone under a cloud like that could not head the ECB. So it fell to a Dutchman, Wim Duisenberg, to head the first European Central bank. Eventually Trichet was cleared and he took his place as the ECB’s second head.

It is important to bear in mind the nationalistic themes that underlay everything in Europe. It is not a united states of Europe. It is a federation of independent nations with a common currency and some common trade rules amid some varied domestic regulations that conflict with the confederation rules from time to time. While the EU makes some political decisions, each nation runs its own foreign policy. The rules in Europe, at least to this American, seem sometimes to be a smorgasbord where they pick and choose which will apply and when.

So it is against this back ground that we wonder about European inflation trends.

Germany is typically is not the country with a burgeoning inflation problem inside the e-zone. The table below identifies those that are persistent violators of the supposed 2% cap imposed by the ECB on inflation. Note that the cap is a zone-wide cap – not country by country- but it still is interesting to see where inflation is stubborn- even in a common currency area.

| Core HICP | Mar-07 | Feb-07 | Jan-07 | Dec-06 | Nov-06 | Oct-06 | Sep-06 |

| Austria | 1.8% | 1.7% | 1.6% | 1.5% | 1.5% | 1.5% | 1.3% |

| Belgium | 2.0% | 1.7% | 1.6% | 1.6% | 1.5% | 1.6% | 1.9% |

| Finland | 1.4% | 1.3% | 1.2% | 1.0% | 1.0% | 1.2% | 0.9% |

| France | 1.3% | 1.4% | 1.4% | 1.5% | 1.4% | 1.3% | 1.2% |

| Germany | 1.7% | 1.8% | 1.7% | 1.0% | 1.1% | 0.9% | 0.8% |

| Greece | 3.5% | 4.0% | 3.6% | 3.4% | 3.3% | 3.3% | 3.0% |

| Ireland | 3.0% | 2.9% | 2.5% | 2.8% | 2.4% | 2.5% | 2.3% |

| Italy | 2.0% | 2.1% | 1.7% | 1.9% | 1.8% | 2.0% | 2.0% |

| Luxembourg | 2.4% | 2.4% | 2.4% | 2.3% | 2.2% | 2.2% | 2.3% |

| The Netherlands | 1.6% | 1.0% | 1.0% | 1.1% | 1.0% | 1.0% | 1.1% |

| Portugal | 2.0% | 2.0% | 2.0% | 2.1% | 2.2% | 2.7% | 2.7% |

| Spain | 2.5% | 2.8% | 2.8% | 2.5% | 2.7% | 2.8% | 3.0% |

| Core HICP/CPI | |||||||

| UK (HICP) | #N/A | 1.9% | 1.8% | 1.9% | 1.7% | 1.6% | 1.6% |

| US | 2.5% | 2.7% | 2.7% | 2.6% | 2.6% | 2.8% | 2.9% |

| Japan | #N/A | -0.3% | -0.2% | -0.3% | -0.2% | -0.4% | -0.5% |

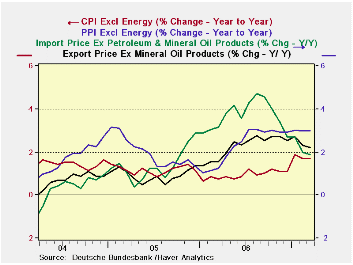

· With energy prices having jumped and with Germany doing a good deal of trade with these high inflation countries inside the E-zone it is useful to look at German export and import prices to see if Germany is importing any of this inflation . · German trends typically are an example of the best of the best…But are they good enough? German domestic price and export and import trends · Trends in German inflation show that Ex petrol and mineral imports, prices surged last year around September, as knock-on effects from high energy prices were passed on. Non Petroleum and non-mineral export prices also were elevated at that time and have since receded but by less than import prices. Producer non-energy prices went up in Germany around midyear and have continued to hover at a 3% pace Yr/Yr. The German CPI excluding energy has also ratcheted up but on a minor scale. The index hit its local low below 1% early in 2006 and has steadily risen moving ‘sharply higher’ in early 2007 to a Yr/yr pace that peaked at 1.9%. Since then it has deflated slightly, moving lower with a current pace of 1.7%. · While Germany is not a problem inflation country, it is one of those countries that tends to have a low rate of inflation and provides a counter-weight to e-zone high inflation countries. So the concern going ahead is that with EIGHT of TWLEVE (excluding Slovenia for this discussion) E-zone members having inflation at or above 2% are there enough countries or enough LARGE countries with inflation low enough below 2% to keep EMU inflation in check? More broadly, there is the question of whether the trend rise we see in German ex-petroleum inflation is still in force, if inflation has played out its bubble already, or if the push in prices has more to come. This next time will it come from wage inflation and tight domestic labor markets? · The perusal of Germany’s trends and those from the E-zone members give us reason to be wary. Not only have recent European data particularly from Germany and France looked firm-to-strong but we do have this inflation effect percolating in the background. With eight EMU countries on inflation levels that are too strong or with borderline trends there are still the low but rising inflation countries to worry about… and that includes about everyone else. · For the ECB, 2% inflation is a ceiling rate, not a target rate. The ECB surely wants to stop inflation short of that mark. The trend from exported inflation, based on German data, is going in the ‘right direction.’ But the pace of even German export and import price inflation while ‘locked’ in a downtrend (excl petrol) is still near to or over the ECB’s preferred pace for overall inflation. It will take some time – and only if that down-trend continues -- before export and import prices will be of some help to fighting inflation. In these circumstances it would be a surprise to see the ECB hold off on a rate hike, although the strength in the Euro is one thing that could make it somewhat gun shy when it comes to pulling the policy tightening trigger. All we can say so far is that if the high euro is an adverse issue for Euro-growth it has not made its mark yet on activity trends nor has it made its mark on restraining export and import prices in Germany. · European growth is not so strong nor is inflation so wrong that ECB action is called for at this very moment. But this, we know, is how inflation often starts. · There can be little doubt that if these trends stemmed from Germany alone and were the Bundesbank making policy what it would do. Will the ECB find its backbone or will it play the same waiting game that the Fed seems to have lost with inflation? · I am reminded of a old Three Stooges comedy routine in which one of the ‘Stooges’ dares a bully to step over this line, then he draws another and dares him to step over the next and the next…before he turns tail to run. Better to act than to draw meaningless lines in the sand. The ECB has drawn a line. The Fed has created a zone of discomfort. The Fed has decided to reside in its discomfort zone instead of taking steps to exit it. Only time can tell what is next. But waiting doesn’t always make it better. What choice will the ECB make? Will it take the policy course of discomfort or like the Fed tolerate inflation discomfort? |

|---|

| % m/m | % SAAR | ||||||

| SA | Mar-07 | Feb-07 | Jan-07 | 3-Mo | 6-Mo | 12-Mo | Yr-Ago |

| Export Products | 0.0% | 0.1% | 0.2% | 1.1% | 1.9% | 2.1% | 1.9% |

| Import Products | -0.1% | 0.4% | -0.9% | -2.6% | -1.1% | 0.8% | 5.4% |

| NSA | |||||||

| Exports excl Petroleum | 0.1% | 0.1% | 0.4% | 2.3% | 1.9% | 2.2% | 1.6% |

| Imports excl Petroleum | 0.1% | 0.0% | 0.3% | 1.6% | 0.4% | 1.9% | 3.2% |

| Memo: SA | |||||||

| CPI | 0.3% | 0.1% | 0.5% | 3.3% | 2.0% | 1.9% | 1.8% |

| CPI excl Energy | 0.1% | 0.0% | 0.4% | 1.9% | 1.7% | 1.7% | 0.8% |

| PPI | 0.2% | 0.2% | 0.1% | 1.7% | 1.4% | 2.5% | 5.9% |

| PPI excl Energy | 0.1% | 0.2% | 0.2% | 1.8% | 2.2% | 3.0% | 1.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief