Global| Oct 24 2014

Global| Oct 24 2014German Economic Climate Makes a Small Rebound for November

Summary

Germany's consumer climate for November, measured by the survey group GfK, rose for the first time in two months. German consumer climate had been at a level of 8.9 on this gauge in July and August. In September, it fell to 8.6; in [...]

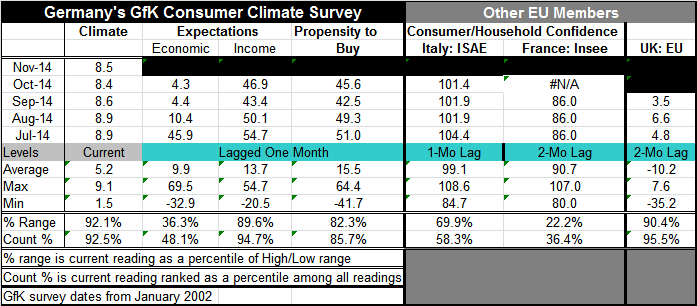

Germany's consumer climate for November, measured by the survey group GfK, rose for the first time in two months. German consumer climate had been at a level of 8.9 on this gauge in July and August. In September, it fell to 8.6; in October, it fell to 8.4. For November, it has rebounded to 8.5. Apparently, the slippage in Germany's consumer climate is over.

Germany's consumer climate for November, measured by the survey group GfK, rose for the first time in two months. German consumer climate had been at a level of 8.9 on this gauge in July and August. In September, it fell to 8.6; in October, it fell to 8.4. For November, it has rebounded to 8.5. Apparently, the slippage in Germany's consumer climate is over.

If that statement is true, it would be quite surprising. The German economy by all economic measures is still struggling in both its manufacturing and services sector. The euro area is still under great deal of pressure. And yet we see there is very short episode for the decline in consumer climate and a shallow decline at that, with the period of decline lasting just two months.

When we look at other survey components, we see more severe evidence of disruption in attitudes about the economy, income expectations and the buying climate. Germany's economic expectations peaked in this cycle at 46.2 in June. By July, they had fallen to 45.9; then in August, the reading took an extraordinary drop down to 10.4. In September, that index fell to 4.4; in October, it slipped further to 4.3. That is now the most up-to-date reading. Economic expectations sit at the 48th percentile of their historic queue; that's below their historic midpoint.

Income expectations peaked in the cycle at a level of 54.7 in July, having fallen to 50.1 in August and to 43.4 in September. This component has already rebounded to 46.9 in October. Income expectations continue to be very high in Germany where the reading sits in the 94th percentile of its historic queue, marking it as higher less than 6% of the time.

The propensity to buy index also rebounded in October, rising to 45.6 from September's 42.5. This component had peaked at a level of 53.5 in June in the cycle. The propensity to buy stands in the 85th percentile of its historic queue of data.

Despite ongoing economic problems, German consumers appear to be rather resilient. Notice that the economic and income expectations and the propensity to buy readings all lag by one month. So we have not yet seen the readings for November when the overall climate index has advanced. Economic expectations have taken the biggest drop. But income expectations have not been damaged much at all; the propensity to buy continues to be relatively strong.

We can compare the German results to some other European countries' results. Italy's consumer confidence stands in the 58th percentile of its historic queue. In France, Insee's confidence measure stands in its 36th percentile while in U.K. consumer confidence is still raging-strong in its 95th percentile. Compared to July, the confidence measure in France has not changed; it is updated through September. Since July, Italy's measure has fallen from 104.4 to 101.4 as of October. In the U.K., confidence has fallen from 4.8 in July to 3.5 as of September.

We see that consumer confidence across the euro area has not been greatly affected since July despite continuing and deepening economic problems. The strong readings have not gotten much weaker and the weak readings have not eroded by much either.

The EU Commission is still fighting with France and Italy about budgets that the European Commission thinks are too generous and take too long to get fiscal deficits back to the targets that EU members have agreed to.

This weekend we will get the results of the European Central Bank's bank stress tests. The two earlier rounds of the stress tests were not rigorous and some banks that had been given the green light under the previous procedures subsequently failed. The ECB is therefore put in the delicate position of trying to run a more stringent stress test, but hopefully one that will not show that a large block of the European banking system is in danger.

Against this background, we can see that there are components of consumer attitudes that have been knocked back sharply. However, consumer confidence per se does not appear to have greatly harmed in Europe by recent events: things are as they have been. Yet we know that there are anxieties. Europe is watching and wondering what is happening and what the plans are to provide energy this winter for Ukraine through its pipeline with Russia. Certainly European countries have to wonder about the energy delivery shortfalls that are currently occurring across Europe, also from the Russian pipeline.

It was reported yesterday that a Russian jet was intercepted over the Baltic Sea; that can't make consumers in Europe happy. Similarly, a report from NATO today asserts that Russian troops are still in Ukraine -- far from reassuring.

In trying to assess all of this, I am not sure if European consumers are resilient or in denial. Europe's economy is not doing well. The only countries with fiscal flexibility are refusing to use it. Austerity is still being preached for EMU nations. Money supply and loan growth are weak. Interest rates have been cut to the bone. The ECB has limited options and fiscal policy is handcuffed. Geopolitical issues linger and threaten. It's hard to understand the nature of European consumers' stoicism in the face of all these challenges.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief