Global| Feb 24 2014

Global| Feb 24 2014German Economic Climate Improves as Expectations Sag

Summary

Economic climate continued to improve in Germany through February. However, the survey by the Ifo shows some cracks in the solidity of German growth. The climate index increased to 14.9 in February from 13.7 in January. Improvement [...]

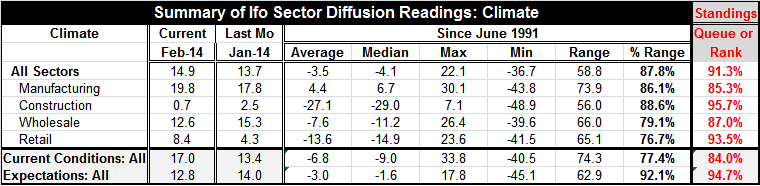

Economic climate continued to improve in Germany through February. However, the survey by the Ifo shows some cracks in the solidity of German growth. The climate index increased to 14.9 in February from 13.7 in January. Improvement was led by a sharp increase in retailing. The retail index climbed to 8.4 in February from 4.3 in January; the retailing is now the second strongest sector for Germany, falling in just behind construction.

Economic climate continued to improve in Germany through February. However, the survey by the Ifo shows some cracks in the solidity of German growth. The climate index increased to 14.9 in February from 13.7 in January. Improvement was led by a sharp increase in retailing. The retail index climbed to 8.4 in February from 4.3 in January; the retailing is now the second strongest sector for Germany, falling in just behind construction.

The rankings at the far right of the table present each sector's topical diffusion index as a percentage standing in its individual historic queue. The other statistics in the table show that there are great differences among the various sectors in terms of their variability, the range of their highs and lows, and their average and median levels. The queue ranking is the best way to compare the performance across sectors. The raw value of an index does not always tell the story. For example, in February the raw reading for retailing is at 8.4 and the raw reading in construction is 0.7. Manufacturing has a raw reading stronger than both of those; it is showing a much higher diffusion readings in February at 19.8! Yet, in a historic context, construction and retailing are the relatively strongest sectors. And this is not a messy, esoteric, calculation. You can see in the table that the construction sector has averaged a reading of -27. In some sense, the ranking index is saying that when you get a 0.7 point indicator on an index that averages -27, that reading is extremely strong. Similarly, retailing has averaged -13.6. Its raw reading at 8.4 is extremely strong in that context. While manufacturing has a higher 19.8 current reading, it has averaged 4.4. In comparison, that is not quite as strong in relative terms as the readings for construction and retailing. The actual ranking calculations use true ranked positions of the indicators, but the story of how they work is well-enough told in relation to the various sector averages.

However, only climate in manufacturing and retailing advanced in February. Climate in construction fell back, as it also did in wholesaling.

As a result of these readings current conditions for all sectors improved to a value of 17 in February from 13.4 previously. Expectations were at the 12.8 in February from 14 the previous month. On a queue standing basis, the expectations index is still the relatively stronger standing at the 94th percentile of its historic queue compared the 84th percentile for current conditions.

The headline from the Ifo surprised the market with its strength, but the report still contains evidence of some weakening. Only two of the four sectors advanced in the month by showing improved climate. The all-important expectations index has begun to drop from its peak.

The German economy is still performing well. Manufacturing is showing strong positive results even though they are not blockbusters by historic standards. The recent issues and the rest of the euro area continue to fester. But for now German economy remains on the expansion path as does the rest of Europe. On closer inspection, the Ifo is not as puzzling- nor strong -as its headline is made out to be in February.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief