Global| Jun 26 2013

Global| Jun 26 2013German Consumer is on the Moon

Summary

Germans do live in a country of their own but is it also a world of their own? The forward-looking GFK consumer climate survey moved up to 6.8 in July from 6.5 in June. The 6.8 reading was last surpassed in September 2007. The German [...]

Is the Oxygen Running Out?

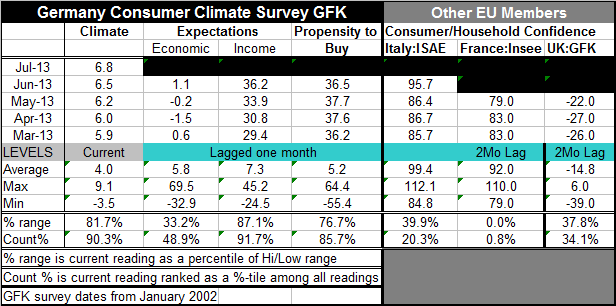

Germans do live in a country of their own but is it also a world of their own? The forward-looking GFK consumer climate survey moved up to 6.8 in July from 6.5 in June. The 6.8 reading was last surpassed in September 2007. The German index is being propelled by a strong move in the propensity to buy, and by increases in income, but assessments of the economy are actually lagging behind. Economic expectations have dropped compared of their value year ago. It's true that expectations are up from their deep dark values at the end of December as the economic reading was a -17.9 at that time, but the most recent economy reading is for June and its 1.1 reading reverses a string of negativism but it still is below its value of 3.0 for June 2012 and remains below a series of stronger numbers prior to that in 2012.

Germans do live in a country of their own but is it also a world of their own? The forward-looking GFK consumer climate survey moved up to 6.8 in July from 6.5 in June. The 6.8 reading was last surpassed in September 2007. The German index is being propelled by a strong move in the propensity to buy, and by increases in income, but assessments of the economy are actually lagging behind. Economic expectations have dropped compared of their value year ago. It's true that expectations are up from their deep dark values at the end of December as the economic reading was a -17.9 at that time, but the most recent economy reading is for June and its 1.1 reading reverses a string of negativism but it still is below its value of 3.0 for June 2012 and remains below a series of stronger numbers prior to that in 2012.

However, compared to the rest of Europe, Germany is in absolutely terrific shape. Germany's climate reading for July is above the 90th percentile of its historic queue or rank. It's components which lag by one month and are available for June show the economic reading in the 48th queue percentile, the income reading in the 91st queue percentile and the propensity to buy in the 85th percentile.

In contrast the index for Italy which is up-to-date three June stands at its 20th queue percentile denoting that it has been weaker only 20% of the time. The reading for France stands in the lower 0.8% of its queue; it's up-to-date through May. UK reading, also up to date through May stands in the 34th percentile of its queue.

Germany's climate reading continues to move up even as it economic reading has faltered and exhibited a great deal of instability. Germany is financially the most powerful firm in Europe. Its economy is still clearly the strongest in Europe. But, having said that, the German growth rate is not impressive. We are talking 'first gear' strength, not overdrive. And Germany is an economy that depends great deal of its ability to export. With its historically low inflation performance within EMU it has remained as the most competitive nation in the euro-Zone. However, the weakness within the Zone as well as global economic weakness is adversely affecting Germany's ability to export and thereby threatens growth in Germany itself.

Although the air of crisis may seem to have passed in the euro-Zone there continues to be serious questions about the euro-Zone, particularly about France and more questioning about what Germany's role in the union should be. It's not likely that the questions about Germany are going to be addressed let alone resolved until after the elections. At that point angle of Merkel will have a freer hand. But at the moment her hands tied by election politics.

And then there is France...ECB head, Mario Draghi, traveled to France where he gave a speech urging growth. I don't think anyone believes that you need to urge the French to pursue more growth. France has had a problem in dealing with its austerity since Holland took control. He has implemented tax hikes in order to not dismantle social welfare programs. Overall he has taken fewer steps to address its excesses than perhaps any other EMU member. While in general it may be a good time to try to urge countries to find a way to create more growth and to bend a little bit less to the whip of austerity, I can't think of a place that less needs that speech than France. All this leaves me a bit confused about what the real Draghi agenda might be.

The recent numbers from the US underscore the US growth is not doing well. The recent forecasts from the various Federal Reserve FOMC members seem already to be hopelessly out of date in addressing the economy's future. It's not just that the FOMC seems to be optimistic on growth but that from the outset its expectations for unemployment seem to be too optimistic based upon the growth scenario that had been laid out. Now, with weaker than expected Q1 GDP in the US, that 'assumption' or 'relationship' glares all the more. Everyone is aware that China is growing more slowly and nobody believes their official numbers (numb-ers?). And, to that mix, a slower US economy and a reduced outlook for the German economy from the IFO that was just released and we have still very challenging global economic circumstances ahead of us.

It will be interesting to see if the German consumer can keep getting his or her hopes up as has been happening amidst the global turmoil and backtracking.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief