Global| Nov 27 2013

Global| Nov 27 2013German Consumer Confidence Is a Juggernaut of Strength

Summary

From 2008 Germany's consumer climate has continued to rise with some fluctuations, but even the global recession and financial crisis failed to make much of a dent to that trend. After that brief interruption due to the financial [...]

From 2008 Germany's consumer climate has continued to rise with some fluctuations, but even the global recession and financial crisis failed to make much of a dent to that trend. After that brief interruption due to the financial crisis, growth in the index recovered strongly and has continued on its trend advance. It seems unstoppable.

From 2008 Germany's consumer climate has continued to rise with some fluctuations, but even the global recession and financial crisis failed to make much of a dent to that trend. After that brief interruption due to the financial crisis, growth in the index recovered strongly and has continued on its trend advance. It seems unstoppable.

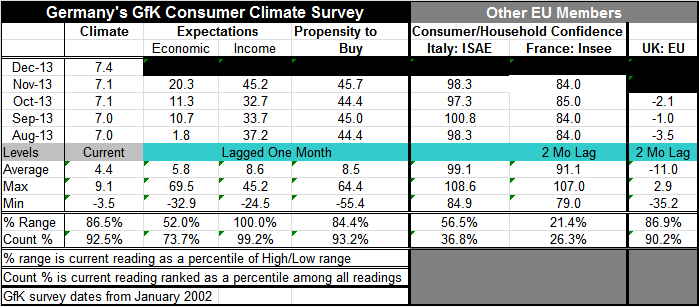

Expectations in Germany have been much more volatile than the actual climate. Before the financial crisis, expectations and climate moved more in tandem. After the crisis, expectations became much more volatile and were more disconnected from climate. The volatility in expectations increased by 40% after 2008 compared to the earlier period.

However, German expectations now are on a strong advance dating from early 2013 after stabilizing in the second half of 2012. German expectations peaked in mid-2007 then fell fast to a trough in late 2008. Thereafter expectations rebounded, reaching a level near to their old peak in early 2011 before falling and then stabilizing in 2012.

The lesson for Germany is that it is very sensitive to events in Europe. The second drop in its expectations index came in the recovery period from the global financial crisis when much of the world was in recovery, but when Europe was in disarray and to some seemed headed toward disintegration. Even though German Climate was not as affected -it was less affected in the recovery period when expectations took their second drop - the impact on expectations was severe.

Europe's financial crisis finally passed, but it did not pass because its ills were attended to. Crises are as much about actual issues as about fears of what those issues will mean for economic performance. Europe, in the end, took enough steps to assure the world that the financial crisis would not tear it apart with severe consequences for all. But the problems that led to Europe's crisis are still percolating. Some of them have been partially attended to. But for Europe many of the key issues remain. Banks are still an enigma. Inflation and competitiveness differences within the euro-zone persist and there is no plan to ameliorate the effects of these differences and no Europe-wide transfer system, the likes of which holds the US together with some of the same forces at work.

For now, Germany continues to expand. As the largest economy in the euro-zone, it will help to lift all the metrics of euro-zone health. But in the end the success of the euro-zone will not depend on Germany growing or on its consumer attitudes improving; it will rely on these same factors improving in the rest of the euro-zone. Germany is the most competitive economy in the euro-zone. Germany eats everyone else's lunch. The question is if there will be enough lunch to go around- not if Germany will eat. This is the problems that the euro-zone is currently trying to grapple with. Notice how confidence lags in fellow euro-zone member countries France and Italy. The euro-zone must find some way to spread the wealth instead of concentrating it. Germany is both the keystone and the albatross in this dilemma. An improving economy in Germany and rising consumer confidence do not hold the same promise for the euro-zone as they do for Germany. In fact if Germany is preparing at the expense of fellow euro-zone members, it is a bad event. The more that Germany prospers and the rest of Europe lags, the more it will look like Germany is the parasite of Europe instead of its savior.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief