Global| Sep 28 2016

Global| Sep 28 2016German Consumer Confidence from GfK Edges Lower But Remains Lofty

Summary

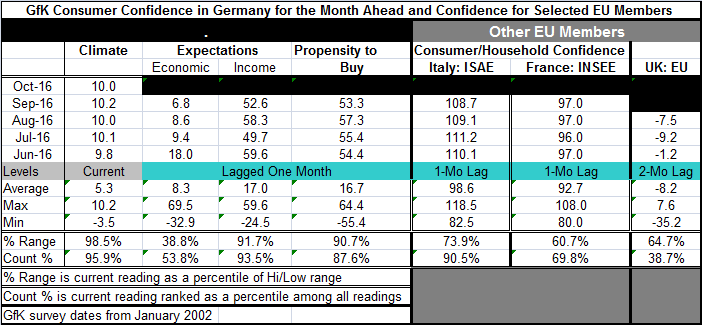

Germany's look-ahead consumer confidence indicator from GfK sees a drop in confidence in October. The setback is small, taking the monthly reading to 10.0, from September's 10.2, which has been the cycle as well as the all-time high. [...]

Germany's look-ahead consumer confidence indicator from GfK sees a drop in confidence in October. The setback is small, taking the monthly reading to 10.0, from September's 10.2, which has been the cycle as well as the all-time high. This is the second time in this cycle that German confidence has reached a peak of 10.2 and backed off; the other occasion was in June 2015.

Germany's look-ahead consumer confidence indicator from GfK sees a drop in confidence in October. The setback is small, taking the monthly reading to 10.0, from September's 10.2, which has been the cycle as well as the all-time high. This is the second time in this cycle that German confidence has reached a peak of 10.2 and backed off; the other occasion was in June 2015.

While the confidence reading is just off its high, economic expectations are much weaker. That sub-index as well as other GfK components lag the headline by one month.

Economic expectations

Germany's economic expectations peaked at a reading of 69.5 in May 2007 before the financial crisis struck. Since then, the reading has fallen then cycled higher to make lower peaks at 58.8 in January 2011, 46.2 in June 2014, and 38.3 in May 2015. But now, with the overall consumer reading just dropping off peak, the economic index is only back to a reading of 6.8 in September, a standing in the 53rd percentile of its historic queue of data. Economic expectations are barely above their historic median in September despite the record high for consumer climate in that same month.

Income expectations

Income expectations are strong, but they slipped back to 52.6 in September from 58.3 in August. The August reading was near the measure's all-time high reading of 59.6 that was registered in June 2016. The readings for income expectations have had an inexorable rise as they have attained levels in 2014-2016 simply not seen in any earlier period when this survey existed (since January 2002).

Buying climate

The propensity to buy index also is strong although it fell back in September to 53.3 from 57.3 in August. Its all-time high is at a reading of 64.4; that high was established in October 2006. The buying climate whose September standing is in the 93rd percentile of its historic queue of data has had readings of 50 or better for 9 months in a row. There are only four episodes with clusters of readings at or above 50 in the history of this index. The buying propensity is only at or above 50 about 15% of this time. German consumers are experiencing a buying climate that has only been rivalled historically from January 2015 to December 2015.

Selected other EU members

Despite sluggish growth in the rest of the EU and EMU, consumer confidence readings have been surprisingly strong elsewhere. Italy, a nation with some real troubles stalking its banks and with substantial political discord, still has its consumer confidence reading in September in the top 10% of its historic queue of readings. France cannot match that with its confidence standing only in its 69th percentile. In the U.K. where the consumer index lags Germany's by two months, the standing for consumer confidence is only in its 38th percentile as it has fallen sharply in the wake of the Brexit vote.

Summary

The global economic scene remains challenging as the WTO just cut its outlook for world trade growth and now projects that global income will grow faster than trade for the first time in 15 years. Still, Germany, which has a very export-oriented economy, finds its main economic institutions prepared to raise their forecasts for German growth in 2016 to 1.9% from 1.6%. The official forecast release date is set for September 29. This lifting of the forecast is an exception to what has been the rule since virtually all economic forecasts for any country or area of size and of any economic importance has been reduced and reduced repeatedly in recent years. But Germany's 2016 upgrade is also accompanied by a downgrade for 2017. The 2017 projection will be for growth of 1.4% instead of 1.5%; a downshifting in the growth rate as well as a downgrade from the previous outlook. If the German institutes are correct about 2016, growth will beat its 1.7% mark for 2015. The German economy has been doing well; its trade performance has generated a huge current account surplus for it, despite what have been challenging times in the EMU and for global growth. Consumer attitudes reflect this optimism even though several of Germany's largest firms face challenges: Volkswagen in the wake of its emissions scandal and Deutsche Bank whose shares have been under extreme selling pressure recently.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief