Global| Aug 28 2019

Global| Aug 28 2019German Consumer Climate Stabilizes: GfK

Summary

The GfK consumer climate reading went dead flat in September at 9.7, stopping three straight months of decline and yet keeping intact a legacy of steady weakening from February 2019. There is even a broader though less steady state of [...]

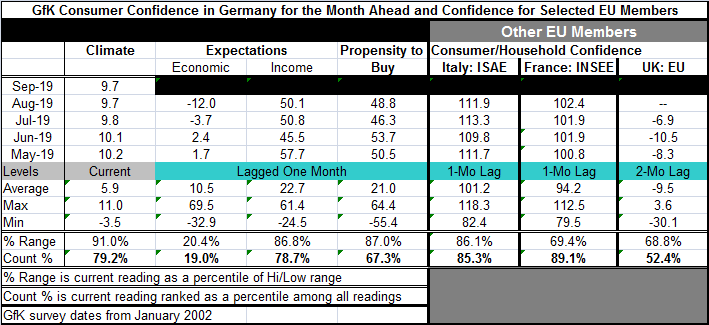

The GfK consumer climate reading went dead flat in September at 9.7, stopping three straight months of decline and yet keeping intact a legacy of steady weakening from February 2019. There is even a broader though less steady state of decline in place back to February 2018. That one embodies some erosion mixed with some minor temporary advances.

The GfK consumer climate reading went dead flat in September at 9.7, stopping three straight months of decline and yet keeping intact a legacy of steady weakening from February 2019. There is even a broader though less steady state of decline in place back to February 2018. That one embodies some erosion mixed with some minor temporary advances.

The German climate gauge for September has a 79.2 rank percentile standing. That still leaves a strong reading in place with the index higher only about 21% of the time.

The components of the GfK index lag the main index by one month. Two of three of them have much weaker standings than the headline. The component ‘income expectation' is an exception with nearly the same ranking at 78.7% in August as the IFO headline for September (and August).

The change in the economic reading month-to-month shows an 8.3 point drop month-to-month in August (current value of -12.0), which is a monthly change that has been larger only about 15% of the time. The last month with a larger one-month deterioration was June 2018 when the economic index fell by 14.2 points month-to-month. The rank standing of the economic expectations index is at its 19th percentile, quite weak.

The propensity to buy index rose month-to-month in August. However, except for last month, this is the weakest propensity to buy index since December 2016. The August reading has a rank standing at its 67th percentile.

The GfK index fell by one tenth of one point month-to-month in August when two of three components fell. The economic index fell very sharply by 8.3 points but the GfK climate index slipped by only one tenth of a point in the month.

Italy and France have confidence readings that are up to date as of August. Italy's confidence level fell month-to-month while the French index rose. Italy's confidence index has an 85.3 percentile standing while France has an 89.1 percentile standing.

The U.K. confidence index at -6.9 actually improved in July from June. It has a 52.4 percentile standing, just above its historic median.

Recent trends in confidence

The German index has been in a state of decline since February 2018. The French index is in the midst of a sharp rebound after it hit a spike low in December 2018. The French index reached its cyclical recovery peak at 107.9 in mid-2017; it fell to a subsequent low at 86.8 in late-December. The current French reading is back up and has come 15.6 points from its recent low to a level only 5.5 points from its cyclical high--quite a rebound. The Italian index has been fluctuating in a range from about 106 to 118 since early-2015. The current Italian reading is right in the middle of this high-low range. The U.K. index is cycling higher now, but it is oscillating in a downtrend since early-2015.

Compared to the sharp weakness in recent manufacturing indexes, the consumer confidence readings are reassuring. Confidence is still ‘positive' if I can define that as above its median value in each of these countries including the U.K. with all of its Brexit worries. Amid other weak readings in Italy and despite some real political upheaval, the consumer reading remains surprisingly firm and with a nascent uptrend. Germany has a still high reading, but it also displays a much clearer and ongoing downtrend. While the European consumer appears to be a positive force for growth, there is not much here that looks all that reliable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief