Global| Aug 29 2018

Global| Aug 29 2018German Confidence Will Continue to Bump Along the Ceiling

Summary

The GfK economic index, that looks ahead to preview September for Germany, shows a slight downtick in its consumer gauge. The recent history shows that German confidence has been bumping along its rent ceiling sketching out a [...]

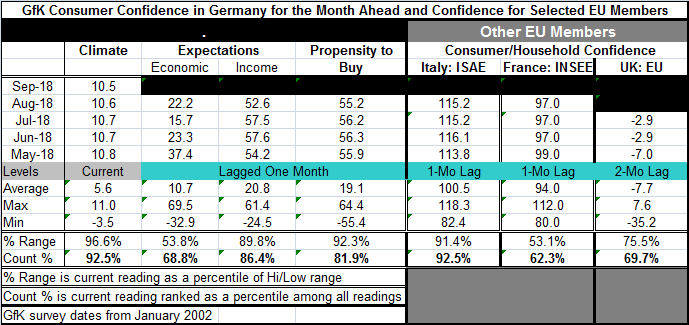

The GfK economic index, that looks ahead to preview September for Germany, shows a slight downtick in its consumer gauge. The recent history shows that German confidence has been bumping along its rent ceiling sketching out a declining trend that has moved ever so slightly lower since late-2017 (see Chart).

The GfK economic index, that looks ahead to preview September for Germany, shows a slight downtick in its consumer gauge. The recent history shows that German confidence has been bumping along its rent ceiling sketching out a declining trend that has moved ever so slightly lower since late-2017 (see Chart).

While the GfK reading remains strong, its economic component has been weakening having hit its peak in January 2018. The economic index had reached even higher levels in 2011, but January is peak level in the phase of the expansion. It has fallen from a level of 54.4 in January to 22.2 in August. In fact, August represents a bounce since that gauge is up from its 15.7 low point of 2018 reached just one month ago.

The economic gauge has the lowest queue percentile standing of any of the GfK components. The economic expectations reading is meaningfully above its median at a queue standing in its 68.8 percentile. But it is not strong. The income expectations reading with an 86.4 percentile standing and the buying climate reading with an 81.9 percentile standing are on much stronger ground. However, income expectations have been eroding while the buying climate gauge has remained somewhat firmer with a much more gradual loss of value.

The overall climate index has a 92.5 percentile standing. It also stands at the 96th percentile of its high-low range. The percentile standing is lower than the percent of range standing only because the index has spent so much time clustered up near the top of its range in this cycle. Still, the component parts of this index show lesser standings in their respective ranges with the economic gauge not in support of such a higher overall reading for consumer confidence.

The German GfK index standing contrasts with a 92nd percentile standing in Italy, and a 62nd percentile standing in France and a 69th percentile standing for the United Kingdom. The surprise here is that Italian confidence stands up so well after even a decade of lost growth and with a good dose of political turmoil in train to boot. France had a strong recovery run last year that is now unwinding to some extent. The U.K. pattern is mostly the result of the Brexit vote and its timing.

We know that Europe has a number of issues festering some of them just below the surface. Europe has not been able/willing to sort out what relationship it will have with the U.K. post-Brexit. The Italian situation is potentially destabilizing to the EU and EMU. And beyond that, the treatment of migrants and the way EU rules treat countries who must deal with migrants has not rising to challenge of what is going on and this has left Greece and Italy to bear the brunt of the migrant problem, its distress dislocation, and financial burden.

Italy and France show much the same pattern for confidence trends as confidence gauges have been running out of gas but have been moving sideways more than moving lower. Italy displays a bit more of a topping pattern while France displays more of a decline on data back to 2017. The U.K. is on a different beat since its confidence tanked in the wake of the Brexit vote and has since caught on and has been achieving a slight upward gradient from 2016 onward.

As a background to all of this, there is also the trade conflict that lurks. The U.S. and Europe are for now quietly negotiating in the background. The U.S. that has been the trade policy aggressor has just cut a deal with Mexico and is negotiating with Canada. The U.S. and China are trading tariffs and threats. In a report released today, the OECD noted that OECD trade contracts had fallen in Q2. Nonetheless, central banks remain on the warpath to reduce their legacy policies of stimulus. There is a lot going on in the mixture of growth trends, policy and geopolitics. A lot of things are changing in the global economy. So far, consumer attitudes have responded in a mostly favorable way by not reacting to the bad news on trade or the heightened risks in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief