Global| Mar 24 2016

Global| Mar 24 2016German Confidence Ticks Off Its Highs Ever So Slightly; Most of the Rest of EMU Tags Along Behind

Summary

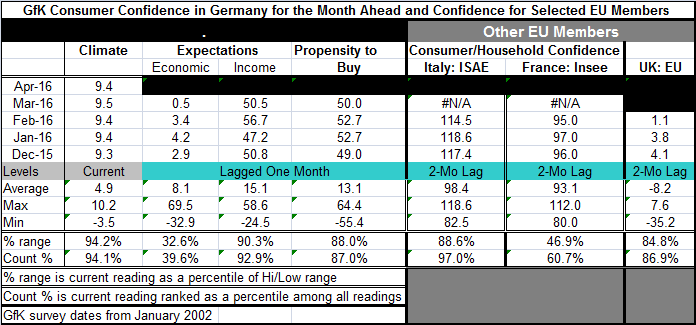

The estimate for German confidence in April is lower than in March by just 0.1 point, its smallest unit of measurement. The index has a 94 queue or count percentile standing which means it has been higher only above 6% of the time, an [...]

The estimate for German confidence in April is lower than in March by just 0.1 point, its smallest unit of measurement. The index has a 94 queue or count percentile standing which means it has been higher only above 6% of the time, an impressively strong reading. However, all is not terrific in Germany. The reading for economic expectations, which lags by one month, fell to 0.5 in March from 3.4 in February and sits in the bottom 40% of its historic queue. Income expectations fell to 50.5 from 56.7 and now reside in the 92nd percentile of their historic queue. Clearly income generation is still in train and German respondents see it and are comforted by it. But there is concern about the economy which has not yet manifested any labor market, or apparently, income-generation concerns. The economy is a vague sort of concept not directly attached to welfare considerations or so it seems here. Still, the propensity to buy reading slipped to 50 from 52.7 and resides in its 87th percentile and is stronger only about 13% of the time. That also is a strong and solid reading.

The estimate for German confidence in April is lower than in March by just 0.1 point, its smallest unit of measurement. The index has a 94 queue or count percentile standing which means it has been higher only above 6% of the time, an impressively strong reading. However, all is not terrific in Germany. The reading for economic expectations, which lags by one month, fell to 0.5 in March from 3.4 in February and sits in the bottom 40% of its historic queue. Income expectations fell to 50.5 from 56.7 and now reside in the 92nd percentile of their historic queue. Clearly income generation is still in train and German respondents see it and are comforted by it. But there is concern about the economy which has not yet manifested any labor market, or apparently, income-generation concerns. The economy is a vague sort of concept not directly attached to welfare considerations or so it seems here. Still, the propensity to buy reading slipped to 50 from 52.7 and resides in its 87th percentile and is stronger only about 13% of the time. That also is a strong and solid reading.

Germans feeling good and running the show

Germans continue to feel good and to be confident. The GfK reading has been at 9.3 or above since February 2015. This is a collection of unprecedentedly high confidence readings since January 2002 when this survey began. The Germans seem to understand that they have the EMU situation at their beck and call. Despite the monthly ups and downs, German values are running the show.

Problems percolate, then are walled off

Still there are problems percolating in Germany and in Europe. Angela Merkel's party lost support in the last regional elections largely because of disagreement over her policy of taking in migrants. The recent terror attack in Belgium may shake that foundation further. However, the shutting of the border by Macedonia has made the issue of migrant sheltering moot for Germany since migrants no longer can travel there. The way is shut. This shutdown is described by some as an action by peripheral countries, but it certainly does shelter the core of the euro area from incursions by migrants and it has bottled up the problem in Greece, a country with diminished resources that has been left to deal with this expensive growing piled-up of humanity. That may have been solved by a recent agreement by the EU to ship migrants off to Turkey and to pay Turkey some six billion euros for their trouble and by an additional EU agreement to help Greece with its costs as well.

To each his own; from each his own?

Separately, Greece has been vetted for its next tranche of funds under its ongoing austerity program and the German viewpoint was that the Greece should be given no slack or special consideration for the monies it had to expend in housing and caring for migrants. That was big of them, wasn't it? I have mentioned here before that the Danish people were, in a very recent survey, deemed the happiest people in the world, but to be a migrant there, to join the `happiness' and accept aid, you will have your worldly goods confiscated by the government. When we evaluate consumer confidence, we must account for local preferences and the kinds of things that do and do not weigh on a consumer's conscience. Angela Merkel seems to worry a bit more about Europe than does the average German consumer or Dane. Italians seem to worry about next to nothing.

Europe's confidence game

Elsewhere in Europe, the consumer confidence measures are lagging the early release by GfK. French, Italian and U.K. confidence measures all are up to date only through February and none stand so strongly relative to their own respective histories- except Italy. February finds each of these measures on a down tick with Italy's reading still strong in the top 3% of its historic queue, the U.K. in its top 13% and France with a less ebullient standing only in the 60th percentile of its historic queue of data. When it comes to confidence, Germany is generally doing better than anyone. The strong reading in Italy is a bit hard to understand since Italy's economic performance is surely not up to supporting that sort of reading. Confidence in Italy is a statement about happiness disconnected from economic wellbeing.

Europe's challenges the German policy `Caliphate'

But Europe faces all sorts of challenges. Countries like Spain are still bottled up in austerity programs that are very unpopular. France has simply asserted its right to take more time to get its budget under control. Italy and Portugal have budget issues. Greece is an ongoing and well-known problem; yet, Germany just yesterday adopted fiscal spending goals and set a budget path consistent with budget balance through 2020. Germany is in the fiscal cat-bird's seat. With its finances in order, Germany is in a position to add fiscal stimulus to an area in great need of it but instead has chosen to dictate to others. Still, the German policy `caliphate' (also known as EMU) has not performed well. German unemployment is low (scary-record low!), but unemployment is higher everywhere else in the EMU. Austerity has put fiscal policy off limits. The ECB's just under 2% price target has not been able to be met and extensive monetary stretching has been unable to get inflation back on track or anywhere close to on track. Despite inflation being below target since February 2013 and despite the ECB having a single policy mandate (inflation!), the Germans have persistently opposed any action to boost it back to target always more worried that the sanctity of the ECB's rules was being violated. Instead it is the ECB's performance that has been constantly violating its mandate and now its credibility is shattered too.

Everywhere in Europe is like living in Germany! Well, in terms of the policy agenda

But these circumstances have favored Germany. The impact of weak growth and inflation in the EMU have pushed the euro exchange rate lower and boosted further German competitiveness -adding to the air of well-being in Germany. This has given German firms time to retool and deal with the ongoing industrial technology revolution. Germany also has an economy geared to run on low inflation and has an economic structure already streamlined and optimized for it. The rest of Europe was caught out of equilibrium and getting back to an equilibrium (a German equilibrium) supported by the Germans has proved (not surprisingly) painful. Some have never been there before since the EMU region has only one exchange rate and there are no more country level freelance depreciations. EMU nations are all locked together and have had very different national inflation performances as their respective legacies. That means that vis-a-vis Germany they have lost ground compared to the starting position in the EMU. Each of the original EMU member countries has lost competitiveness with Germany since the euro was launched. Only Germany and France have averaged a price level rise less than the (weighted) aggregate for the EMU as a whole since EMU was begun- and France still trails Germany in that regard. Since the EMU was formed, inflation differentials vs. Germany have ranged from 2.5% (vs. France) to 18.9% (vs. Luxembourg). These differentials represent losses in competiveness vs. Germany. Germany has gained 16.9% vs. Spain, 13.8% vs. Ireland, 13.1% vs. Portugal, and 10.9% vs. Italy. Currently countries wishing to make gains in competiveness vs. Germany need to run national inflation rates below the -0.2% pace Germany currently is running. That's right; right now it takes a policy of outright deflation to gain on German competitiveness judging from the German HICP.

Play EMU...the German game

So this is the game Germany plays in Europe. Germany is off to a huge lead by having kept inflation so much lower. France has been smart to tag along and does not trail by much despite its ongoing budget issues. France has kept budgetary excess from whacking its price level too badly. But the rest of Europe is in a German pickle, or maybe vat of sauerkraut. The fixed exchange rate keeps everyone tied to the German game with the Germans in the lead. There is no escape for Europe. They have no choice but to play along or to leave. Despite stresses, no one really wants to leave. But to stay will continue to be painful since Germany is still playing for keeps: balancing its budget and with a falling price level. Catching Germany will not be painless. It looks harder than catching Secretariat at the Belmont stakes. The Italians are not exactly prospering, but judging from their confidence reading, they have learned to live with the pain much more than they have acceded to adjust their economic policies. I wonder how long that can last? And if it does not last, then what?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief