Global| Aug 29 2017

Global| Aug 29 2017German Confidence Leads a Happy Europe

Summary

Good times in the euro area The GfK survey somehow magically surveys (projects) German confidence for the month ahead. The reading for September has ticked up from its August level to reach a new high in the series (it dates from [...]

Good times in the euro area

Good times in the euro area

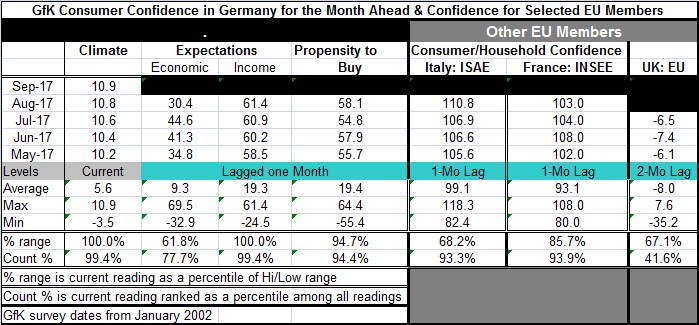

The GfK survey somehow magically surveys (projects) German confidence for the month ahead. The reading for September has ticked up from its August level to reach a new high in the series (it dates from January 2002). However, we also log the most recent observations on confidence for Italy, France and the United Kingdom. If we rank each of them on a common timeline, German confidence is at a new all-time high as its rank measure shows confidence is this high, or higher, only 0.6% of the time. In Italy, confidence is as high, or higher, than its August level less than 7% of the time. In France, confidence is as high, or higher, than its August level only about 6% of the time. But in the U.K. where the dark clouds of Brexit fears have gathered and settled confidence is below its median and is lower only about 41% of the time. Yes, Brexit fears make a big difference. Still, for the largest economies of EMU, the consumer tilt on confidence is a definite strong positive reading. European consumers are by and large in a very positive frame of mind. The EMU wide index for July from the EU Commission for example stands at its 94th percentile and is higher less than 6% of the time for the EMU as a whole.

Some inconsistencies

However, gauging the consumer's mood is tricky stuff. And not all gauges produce the same results. On data through July, the EU gauges put German consumer confidence in the top 6th percentile, not much of a different signal from the GfK signal for September. France is at a top 6% level too, quite similar to its own (INSEE) confidence gauge. But Italy is placed at its 57th percentile by the EU framework, a great difference from its 93rd percentile in the ISAE framework. Spain also has a strong standing in the EU framework with a top five percentile reading. Portugal, a former troubled economy, has a very strong top one percentile reading. But Greece, for example, lags with a 41st percentile standing. Still, confidence will always be hard to measure and inconsistencies are an inevitable part of the process. Also Europe is a large area with many different national jurisdictions and some differences in confidence levels will be normal feature of the area. On balance, most of these are very strong readings - certainly that is true for the largest economies of the EMU. To see such strong readings for Portugal and Spain as well is particularly heartening.

German detail

The German GfK survey has three components that are available with a one month lag. They show that confidence is being boosted in Germany mostly by income expectations which are on an all-time high reading. The propensity to buy has a strong 94.4 percentile standing, which is also very strong. But the economic gauge is a relative laggard with its 77.7 percentile standing. While income and the buying index each have strong rank standings and even higher standings in their all-time ranges (high-low ranges), the economic index is weaker and has an even lower standing in its all-time high-low range of values than for its queue or rank standing. Despite the ebullient readings for Germany, the economic expectations gauge for Germany slipped to 30.4 in August from 44.6 in July. Germany also has issues it is not all good times. But the beer gardens are full.

Geopolitics

With all the new geopolitical chaos in the wake of North Korea's ill-conceived decision to shoot a missile over the island of Japan as part of a 'test,' it is important to broaden our discussion of confidence. Geopolitical events can undercut an economy and confidence in it quickly. I am not making that a projection, but it is important to see that the current context for confidence is a somewhat unstable environment politically. Not only are the UK-EU Brexit talks another potential source of instability, but there are ongoing geopolitical tensions in the Baltics and surrounding the Ukraine as well as new allegations by Israel that Iran is doing research on more precise missiles. The U.S. has challenged Iran by a requesting an inspection and has been denied. President Trump has bad-mouthed the Iran nuclear deal from day one. There are a number of places where tensions of various sorts could flare as well as there are ongoing negotiations about the various U.S. challenges related to its charges that trade has not been fair. Also a number of nations continue to claim the right of clear passage and challenge China's claim to the South China Sea where the U.S. navy has suffered several maritime accidents this year. In a world where consumers claim to feel so good, there are a lot of events in the wings that could change that in a hurry. Don't worry...but be wary.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief