Global| Feb 26 2019

Global| Feb 26 2019German Confidence Is Steady Despite Slowdown, Italy and France Show Stability or Better as Well

Summary

In Germany economic expectations have fallen off rather sharply but the German consumer confidence reading continues to hover very close to its all-time high on this gauge. The GFK index is a look-ahead index that is updated through [...]

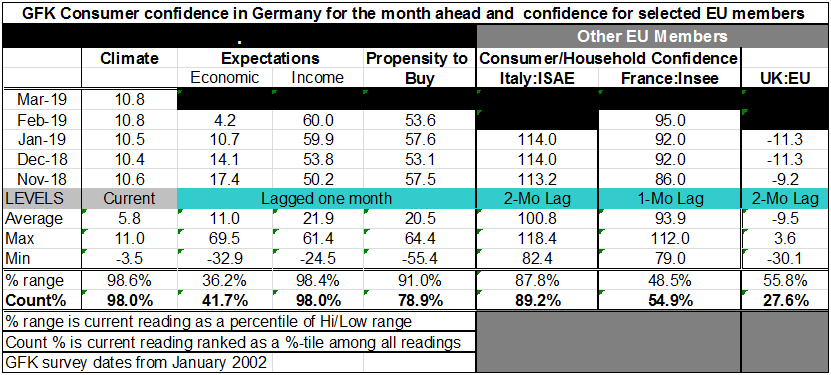

In Germany economic expectations have fallen off rather sharply but the German consumer confidence reading continues to hover very close to its all-time high on this gauge. The GFK index is a look-ahead index that is updated through March while its components are up-to-date only through February. German income expectations are still extremely strong but other components are much more challenged.

In Germany economic expectations have fallen off rather sharply but the German consumer confidence reading continues to hover very close to its all-time high on this gauge. The GFK index is a look-ahead index that is updated through March while its components are up-to-date only through February. German income expectations are still extremely strong but other components are much more challenged.

Economic expectations fell in February to 4.2 from 10.7 in January and stand only in their 41 percentile of its historic rank or queue standing. This compares to an overall consumer climate standing in its 98th percentile. Income expectations also are in their 98th percentile with the ‘propensity to buy’ index getting softer again; that index clings to its 78th percentile standing.

Several other country level confidence measures show mixed performance. Italy, France and the UK all have local confidence readings that are steady over at least the last two months. But more broadly there is a lot more difference than similarly in the standings of those metrics. Confidence, of course, tops up with the Germany’s 98 percentile rank standing. Italy logs a strong 89th percentile standing. France drops all the way back to a 54th percentile standing with the UK still suffering Brexit woes has a 27 percentile standing, leaving the UK as the only country in this group with a standing below its historic median (which occurs at a standing at the 50th percentile); the UK has a standing just above its lower 25th percentile.

The UK continues - even through today - to have Brexit arguments in play. It has had a hard time deciding what the EU will let it do that it also wants to do, and this uncertainty is dogging consumer confidence in the UK. In France confidence has risen in February as the ‘yellow vest’ movement is falling out of favor. Italy, despite the worst economic performance of any EMU member country (save Greece) since the great recession, continues to log extremely high consumer confidence. In Italy there has been some erosion in local elections of the five star movement’s coalition.

Europe is slowing. On some metrics the slowing borders on dramatic. In perspective, the slowing, while considerable, and, in some ways sudden, still has not taken weakness to a troubling low. We can see from the consumer confidence readings that consumers have not had their expectations and assessment for conditions to degrade by much recently. That is encouraging. At the same time there is a huge difference in how various consumer populations in Europe feel. For the time being the UK is a special and afflicted case.

Globally inflation remains low and central banks in monetary center countries are undershooting their inflation targets if they have them. This situation allows central banks to have flexibility in dealing with the weakness when it emerges, as it has. While most central banks around the world have been stuck on stimulus, in the US the Federal Reserve has been raising rates and that process has come to a sudden halt as financial conditions and growth began to turn somewhat dodgy at the end of 2018. In response to that policy shift there is some evidence that economic conditions are stabilizing after a period of encroaching weakness. Of course, consumers, governments and central banks are watching the US-China trade negotiations closely. Trade policy is important to economic performance and ultimately to consumer attitudes. As trade and Brexit negotiations churn on, the news on European confidence this month is encouraging, but just as clearly, challenges to growth remain.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief