Global| Oct 07 2014

Global| Oct 07 2014German Capital Goods Output Takes a Hit

Summary

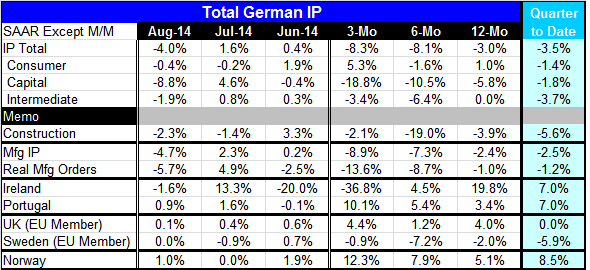

German industrial production fell sharply in August, falling by 4% after rising by 1.6% in July. The sequential growth rates for output show widening declines from 12 months to six months to three months. Output is declining at all [...]

German industrial production fell sharply in August, falling by 4% after rising by 1.6% in July. The sequential growth rates for output show widening declines from 12 months to six months to three months. Output is declining at all those horizons. Nonetheless, German officials argue that the current data have been exaggerated by German holidays.

German industrial production fell sharply in August, falling by 4% after rising by 1.6% in July. The sequential growth rates for output show widening declines from 12 months to six months to three months. Output is declining at all those horizons. Nonetheless, German officials argue that the current data have been exaggerated by German holidays.

Consumer goods output fell by 0.4% in August after a 0.2% decline in July. Nonetheless, consumer goods output is showing a 5.3% gain over three months after falling at a 1.6% rate over six months. Over 12 months, consumer goods output is still positive, up by 1%. Capital goods is the category that has turned the most sharply. Capital goods output fell by 8.8% in August after rising by 4.6% in July and falling by 0.4% in June. Capital goods output is falling at an 18.8% annual rate over three months, falling at a 10.5% annual rate over six months, and falling at a 5.8% annual rate over 12 months. The capital goods sector is extremely weak, but all these calculations are importantly affected by the 8.8% drop in August. Intermediate goods output fell by 1.9% in August and it's down at a 3.4% annual rate over three months, down at a 6.4% annual rate over six months, and flat over 12 months.

Consumer goods and intermediate goods do not show a consistent pattern of continually weaker output trends over shorter horizons. Intermediate goods output is declining over three and six months but it's flat over 12 months; for consumer goods, there's a reasonably sharp increase over three months. The deteriorating sequential growth rates for overall industrial production are really dominated by weakness in capital goods.

Construction output fell by 2.3% in August and by 1.4% in July. It's down at a 2.1% annual rate over three months, down at a 19% annual rate over six months, and down 3.9% year-over-year. The construction sector is chronically weak but does not show a progressive trend toward greater weakness.

Manufacturing industrial production fell by 4.7% in August after a 2.3% increase in July. It's falling at progressively faster rates over closer time periods: 8.9% over three months, 7.3% over six months, and 2.4% over 12 months.

We can compare these trends to real manufacturing orders. We see the same progressively weaker growth and orders down 13.6% at an annual rate over three months, down 8.7% at an annual rate over six months, and down by 1% at an annual rate of 12 months.

Industrial output has widespread weakness. The weakness in output is reflected in weakness in orders as well and that looks ahead. Weakness is present in the construction sector as well as in the manufacturing sector.

Several European countries have reported industrial output as early as has Germany. Early reports for August show Ireland with a 1.6% drop, Portugal with a 0.9% rise, the U.K. with a 0.1% rise, Sweden flat, and Norway with a 1% rise.

In these countries, only Ireland showed a decline month-to-month. Over three months, Sweden and Ireland show declines. Over six months and 12 months, only Sweden shows declines. Sweden has declines on all horizons, while the other four countries show increases over six months and 12 months at least.

Portugal shows progressive of strength in output with growth of 10.1% over three months, 5.4% over six months and 3.4% over 12 months. Norway also shows progressive of strength with output up 12.3% over three months, 7.9% over six months and 5.1% over 12 months.

Only Ireland shows progressive weakness with growth going from a strong 19.8% rate over 12 months and 4.5% over six months to falling at a 36.8% annual rate over three months. For the most part, outside of Germany, output in these other countries is still tending to expand.

In the quarter to date, all the German metrics are showing declines while among the other countries, only Sweden has a decline in the quarter to date; even Ireland is growing at a 7% annual rate in the quarter to date in face of its steeply negative three-month growth rate.

The German figures shook European markets and affected premarket stock trading in the U.S. this morning. Output was weaker than expected and came as a surprise even in the wake of what had been weaker-than-expected German industrial orders that were just reported. German officials do not take this figure at face value and argue that there are holiday affects that are amplifying the decline. But markets seem to be in no mood to believe arguments of moderation.

Overnight we also have more information on the weakness in Russia with the weakness in the ruble. Russia has been spending money hand over fist in the foreign-exchange markets to try to break the decline of the ruble, and operation seems to have largely failed. Russia's central bank is reported to have spent at least $1.68 billion to prop up the ruble over the last two trading days, its biggest intervention since President Vladimir Putin's incursion into Ukraine in March.

While Russia continues to try to argue that its economy is pressing ahead in the face of Western sanctions, and is largely unaffected, it seems that the sanctions actually are having a huge effect on the Russian economy. As that fact becomes harder to cover up, the Russians will have less to lose by taking more aggressive foreign policy actions. As this situation drags on and as Russia fails to capitulate and if it continues to support rebels in Ukraine, we can expect the risks to magnify. The less Russia has to lose, the less the threat of more sanctions will deter it from its desired actions. So far Russia has only been playing games with European fuel deliveries but that could change.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief