Global| Jan 27 2016

Global| Jan 27 2016German and European Confidences Hold the Line or Advance in Uncertain Times

Summary

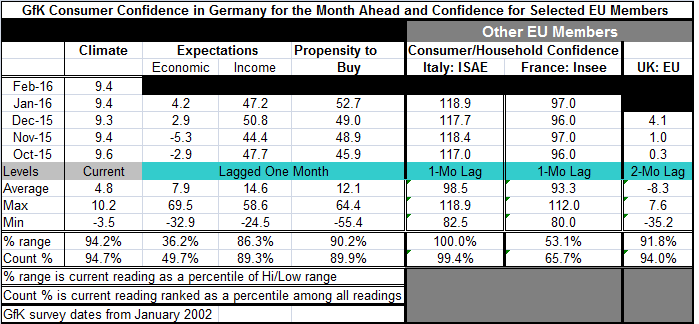

Germany's GfK consumer confidence index, a forward-looking measure, predicts a flattening of confidence for Germany in February. The GfK measure has slowed markedly in recent months but has continued to make some hard-fought gains. As [...]

Germany's GfK consumer confidence index, a forward-looking measure, predicts a flattening of confidence for Germany in February. The GfK measure has slowed markedly in recent months but has continued to make some hard-fought gains.

Germany's GfK consumer confidence index, a forward-looking measure, predicts a flattening of confidence for Germany in February. The GfK measure has slowed markedly in recent months but has continued to make some hard-fought gains.

As for its components which lag by one month, the economic index is expanding again; after two consecutive months of negative readings, it now boasts two consecutive months of positive and advancing readings. The income metric has backtracked in January and sits below its October level as of January. The propensity to buy index is up above 50 for the first time in four months and has its highest reading since July 2015.

The GfK climate reading in February sits in the 94.7 percentile of its historic queue of ranked data, an exceptionally high standing. The economic index is decidedly middling with a 49.7 percentile standing, below its historic median. Despite the backtracking for income in January, the income standing is at its 89.3 percentile. Similarly, the propensity to buy has a strong 89.9 percentile standing in its historic queue of data.

These metrics show strength up and down the line for the readings on Germany consumer confidence. Income and the propensity to buy have exceptionally strong readings to support the overall climate index. The economy index, however, lags. Despite its renewed growth, the economy assessment has several points of slipping, peaking in June 2014 then recovering and peaking more recently at a lower level in May 2015, then slipping again. The economy index has been by far the most volatile component reading since 2010. Over that period, the economy index has been above twice as volatile as income and as the propensity to buy. Prior to that, the propensity to buy had been the most volatile index with income expectations still relatively tranquil over the previous period. Nevertheless, in the more recent period, German consumers have developed a more volatile angst toward economic performance beginning around 2010. And since then, the economy has not only been more volatile, its assessment has become decidedly weaker than the other components.

Other Europe

The table encourages comparisons with some other relatively large EMU member economies: France, Italy and the U.K. Each of these metrics lags the GfK reading by one or two months (two in the case of the U.K.). While economic performance (growth, the unemployment rate, etc.) elsewhere in Europe has generally lagged performance in Germany, one interesting and surprising finding is the extent to which consumer confidence has performed well outside Germany. In Italy, the consumer sentiment reading is on its peak for this period back to January 2002. In France, the index stands in its 65th percentile of its historic queue of data. The U.K. metric stands in the 94th percentile of its historic data queue. Despite the ongoing slow growth and budget battles, France has a nearly top one-third standing in confidence, which is a relatively good result given its economic performance. Italy's standing is astonishing given its performance and the challenges that still lie ahead. The U.K. has continued to perform relatively well; still, its consumer attitudes are generally one of the best metrics of its economy.

Consumers can help to support growth by their confidence or impede by their lack of confidence. And the services sector, which is less volatile and less reported upon has continue to churn out growth in all these countries (with less of a propensity in France) and generally has outperformed the more widely-reported manufacturing sector. The services sector is the sector of job growth. Job and income growth are the backbone of consumer confidence. For the most part, there has been continued expansion of some degree in those variables. Low inflation and dropping prices in a modern economy generally boost real wages at least to some degree and that supports confidence.

2016 surprises

Still, Europe is growing slowly. One of the surprises about these January confidence measures is the extent to which consumers are simply not reacting to the stock market selloff that has begun the New Year. In Europe, there is the additional problem of migrants which is being dealt with poorly and by different methods in different countries. For example, recently, Greece has been threatened with the removal of Schengen privileges because it has been unable to staunch the inflow of migrants. Europe continues to have slow-growth economic issues. It is threatened, as is the global economy, by the extremely weak stock prices and ongoing drop in stock prices. But consumers, at least those in net energy consuming countries, will see some help from weaker energy prices. In the U.S., the reaction to all this is more mixed because the U.S. has been a producer and in recent years has ramped up its production abilities using new technologies. Low oil prices will hurt investment in the U.S. Europe does not take such a hit to industry in general (however, there are Royal Dutch Shell, Total and BP, to name three European energy companies that will have to deal with the oil shock).

Summing up

In general, Europe is an energy importer and it has some of the highest energy and gasoline prices in the world. Still, the weakness in stocks will project a chilling effect on wealth and there could yet be negative knock-on effects to spending as a result. We may wish to revisit these consumer measures in one month and see if stocks have recovered and if consumers remain so dismissive of their impact. For now all is well on the consumer side of the ledger and cheap oil helps.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief