Global| Feb 13 2009

Global| Feb 13 2009GDP In EMU Falls Hard In 2008-Q4

Summary

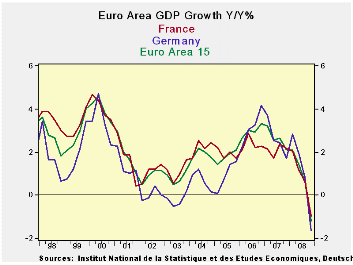

GDP is declining in the e-Zone at a very rapid rate. The fourth quarter GDP declines in the zone have been larger than had been expected. Declines in Europe are now generally worse than the declines in the US. Germany has just adopted [...]

GDP is declining in the e-Zone at a very rapid rate. The

fourth quarter GDP declines in the zone have been larger than had been

expected. Declines in Europe are now generally worse than the declines

in the US. Germany has just adopted a second stimulus package worth 50

billion euros over two years to buffer its sagging economy. Budgets in

EMU are beginning to strain or to shatter the EMU guidelines know as

the Maastricht Criteria. Italy and France have been warned by the

Chairman of e-Zone finance ministers, George Junker, about

protectionist policies. "The European Commission needs to examine very

intensively the details of the Italian and French stimulus programs,"

Juncker was quoted as saying in a pre-release of an interview with a

German newspaper. These are the sorts of things that happen in

recession. Survival is the first order of business and sometimes the

rules get trampled or slightly skirted along the road to survival.

As the G-7 finance ministers meet in Italy there is concern

about protectionism. The US too has been warned by Japan. The Japanese

are worried about the ‘buy American’ provisions in the US stimulus

package. No one wants a trade war. But everyone seems to being skating

close to the edge.

Economies are weak and the manufacturing and export-based

economies have been hit the hardest. Note that among this growth of

counties the US Q4 result is second best; Germany and Italy have been

hit hardest. . The US, of course, has a large service sector and it is

a net importing nation. The short fall in US demand has activated one

of the automatic stabilizers in GDP, imports. Imports are weakened so

US GDP has been buffered in its decline, since imports subtract from

GDP growth. Weaker imports mean stronger GDP. But that has transmitted

more weakness overseas to the countries that export to the US. Still

the domestic weakness in the US is severe and it is so severe that

Japan’s Toyota is planning layoffs in its US operations.

This decline in GDP puts everyone on notice for how bad things

are. GDP is one measure all can see and relate to, at least to some

extent. In the US, the labor market has been hit harder than in Europe

with the its broader social safety net and business practices that are

different and a little less quick on the lay-off trigger. There is

concern about how bad the second round effects will be in the US with

such severe labor market displacement. Mitigating that is the task of

the stimulus package. So far US GDP has not been hammered to the extent

expected. But if the US has a more severe second round you can expect

that it will get Europe’s attention too.

| E-Zone and main G-10 country GDP Results | |||||||

|---|---|---|---|---|---|---|---|

| Quarter over quarter-Saar | Year/Year | ||||||

| GDP | Q4-08 | Q3-08 | Q2-08 | Q4-08 | Q3-08 | Q2-08 | Q1-08 |

| EMU-15 | -6.1% | -0.7% | -0.7% | -1.2% | 0.6% | 1.4% | 2.1% |

| France | -4.6% | 0.4% | -1.2% | -1.0% | 0.6% | 1.2% | 2.1% |

| Germany | -8.2% | -2.1% | -2.0% | -1.7% | 0.8% | 2.0% | 2.8% |

| Italy | -7.1% | -2.2% | -2.5% | -2.6% | -1.1% | -0.4% | 0.3% |

| The Netherlands | -3.4% | -1.2% | -0.3% | -0.7% | 1.7% | 3.3% | 4.0% |

| UK | -5.9% | -2.5% | 0.0% | -1.8% | 0.3% | 1.7% | 2.6% |

| US | -3.8% | -0.5% | 2.8% | -0.2% | 0.7% | 2.1% | 2.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief