Global| Nov 14 2019

Global| Nov 14 2019GDP Finalizes for the Euro Area and It Is Disappointing

Summary

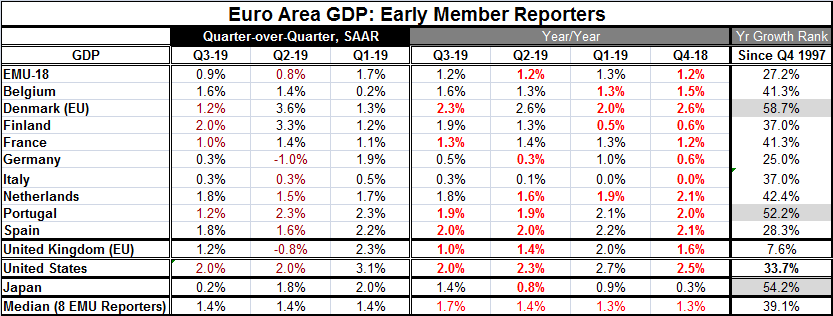

GDP in the euro area and for most members finalized for the third quarter. Three members out of eight saw weaker growth quarter-to-quarter. While four saw GDP’s year-on-year growth decelerate. Rounded to one decimal place, growth in [...]

GDP in the euro area and for most members finalized for the third quarter. Three members out of eight saw weaker growth quarter-to-quarter. While four saw GDP’s year-on-year growth decelerate. Rounded to one decimal place, growth in the EMU was unchanged year-over-year but carrying more digits there was a very small acceleration. The GDP data do not tell a story of Europe in distress, but it growth rates do tend to a description of ‘poor.’ EMU year-on-year growth for the last four quarters has averaged only 1.2%. Back to 1997, year-on-year growth has been stronger nearly 3/4ths of the time.

GDP in the euro area and for most members finalized for the third quarter. Three members out of eight saw weaker growth quarter-to-quarter. While four saw GDP’s year-on-year growth decelerate. Rounded to one decimal place, growth in the EMU was unchanged year-over-year but carrying more digits there was a very small acceleration. The GDP data do not tell a story of Europe in distress, but it growth rates do tend to a description of ‘poor.’ EMU year-on-year growth for the last four quarters has averaged only 1.2%. Back to 1997, year-on-year growth has been stronger nearly 3/4ths of the time.

The table shows growth for EMU overall, eight EMU nations, two EU-only members, the U.S. and Japan. Growth is ranked for each country for year-on-year growth rates back to 1997. All but three countries have rankings below 50% on the this basis which means growth has been below their median values for all but three countries in the table, only one of them, Portugal, is an EMU member. The other countries with above median growth are Japan and Denmark. Japan does this on the fifth weakest year-on-year country growth rate in the table (out of 12).

Growth Profiles

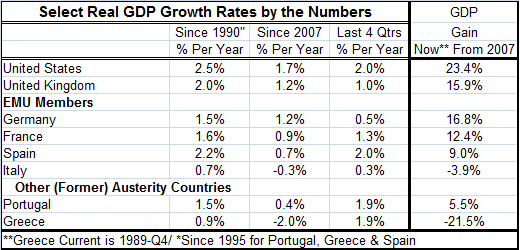

The table below shows total GDP growth and compounded growth rates for GDP for a select group of countries on various timelines. Over the past year, the U.S. and Spain are tied for growth leadership in this table with Portugal and Greece not far behind. Italy and Germany are the laggards on growth rates of less than 1%.

Since 2007, the U.S. has grown the fastest averaging 1.7% (that period includes the Not-So-Great-Recession). Next up is the U.K. at 1.2% and Germany at 1.2%. Italy and Greece have GDP declining on balance (yes, that means Italian and Greek GDPs both are lower in Q3 than they were in Q1 of 2007). Perhaps that injects some sympathy if not reality into Italy’s pleas for some forbearance on its debt issues. Italy is very compliant on EMU inflation performance. But getting inflation back into the tube was very painful for Italy; that process caused growth to back track reducing GDP in absolute terms – and it was much worse for Greece. France and Spain each average less than 1% growth over this period, a slow pace on balance.

On a much longer timeline back to 1990 (or 1995 for Portugal, Greece and Spain), U.S. growth leads at 2.5%. Spain is second at 2.2%. The U.K. is third at 2.0%. Next is France followed by a tie between Germany and Portugal. Of course, Italy and Greece are dinged on the long growth calculation by their underperformance since 2007; both average growth rates of less than 1%. It’s not like Greece and Italy had milked the system for huge growth rates that they had to pay for post 2007. Both have really been crippled by the austerity process. And while there is inflation progress to show for it and less debt creation, both economies are still struggling.

During this long period, Germany has not fared all that well for what is supposed to be Europe’s strongest economy. But Germany was still involved in absorbing East Germany and dealing with its reunification and all the attendant issues. Separate figures for West Germany alone would be so much more impressive. But those days are gone.

Perspectives in Growth

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief