Global| May 03 2017

Global| May 03 2017GDP: Early Reporters Show Tepid Results

Summary

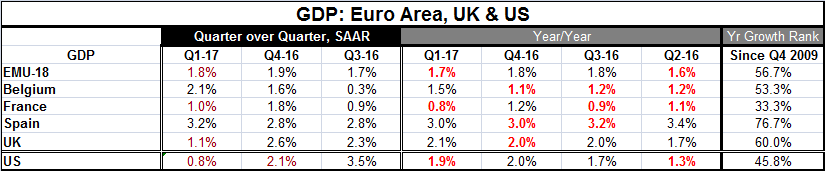

GDP reports for Q1 are starting to roll in. In the EMU, the year-on-year pace is 1.7% with Q1's annualized quarterly pace at 1.8%. EMU Q1 growth exceeds growth in the U.S., but the U.S. still has faster growth than Europe over four [...]

GDP reports for Q1 are starting to roll in. In the EMU, the year-on-year pace is 1.7% with Q1's annualized quarterly pace at 1.8%. EMU Q1 growth exceeds growth in the U.S., but the U.S. still has faster growth than Europe over four quarters.

GDP reports for Q1 are starting to roll in. In the EMU, the year-on-year pace is 1.7% with Q1's annualized quarterly pace at 1.8%. EMU Q1 growth exceeds growth in the U.S., but the U.S. still has faster growth than Europe over four quarters.

The chart shows that for the last year or so the U.S., EMU and the U.K. have logged remarkably similar and steady rates of growth.

This quarter, of the six countries in the table, growth rates for GDP decelerated in four: the EMU, France, the U.K., and the U.S.

Growth assessments

France is the laggard in growth with recent growth rate clusters around 1% and with its current year-on-year growth rate in the lower one third of its queue of growth rates since end-2009. The U.S. with growth at 1.9% (the third highest year-on-year rate in this table) also logs a relatively weak standing for growth at its 45th percentile. Growth in the U.S. is below its median, but that also leaves it where the Federal Reserve now thinks U.S. growth potential is located. Growth in Belgium at 1.5% is slightly above its median pace for this period with a queue standing at its 53rd percentile. The median for growth occurs at the 50th percentile for all these measures. The EMU is only slightly stronger than Belgium with a queue standing in its 56th percentile on year-over-year growth of 1.7%. Spain, having posted growth rates of 3% or more for each of the past four quarters, has year-on-year growth of 3%; that pace has a 76th percentile standing, the highest of any country in the table. The U.K. with the second strongest year-on-year growth in the table has a queue standing for its growth rate in tis 60th percentile.

These growth rates are moderate with the exception of Spain. In the case of Spain, despite a strong pace of GDP growth at 3.2% q/q SAAR in Q1, it has the second highest unemployment rate (18.2%) in the EMU, trailing only Greece.

Policies show some divergence without a clear rationale

While there have been some instances noted in soft-data or survey-data that has signaled a pickup in growth, the GDP reports are not showing any sort of a pickup in strength. The queue rankings of growth rates are another testament to moderate rates growth. The European Central Bank is still locked and loaded on a program of stimulus as is the Bank of Japan. The Bank of England is also running a stimulative policy but has had some thoughts about shifting. In the U.S., the Fed is in the middle of a program to normalize rates. Yet, looking at the U.S. quarterly growth rates and the ranking of its year-over-year rate, it shows no separation from the rest of reporting countries where full bore stimulus is still the order of the day.

PPI trends break

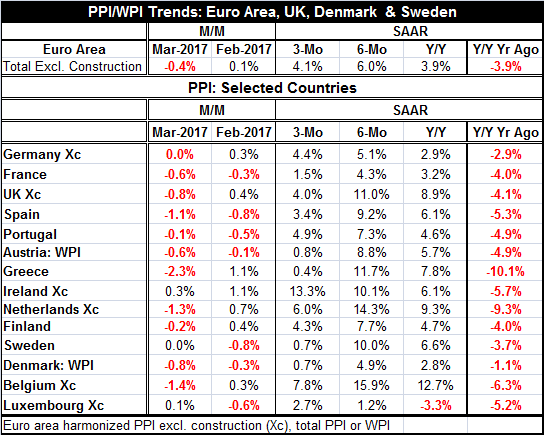

Meanwhile, on the inflation front, Europe's PPI inflation data just released show a marked deceleration with a fairly broad decline in prices of 14 European countries in March. Data show that the PPI fell in 10 of those countries and was unchanged in two with gains posted only in Ireland and Luxembourg month-to-month. In February, prices had fallen in in seven of these countries. For all of the EMU, the PPI rose by 0.1% in February and fell by 0.4% in March. The PPI growth rate is now barely advancing at a stronger pace over three months than it is over 12 months unlike the six-month pace that shows a substantial pick up compared to the 12-month pace. However, for most of these European nations, inflation is actually decelerating over three months compared to 12 months. In fact, it is decelerating in all but four of 14 countries: Germany Portugal, Ireland and Luxembourg. And because of the weight of Germany in the PPI, the EMU area PPI also shows acceleration over three months compared to 12 months.

Prospects

What we see in the PPI data is another case of inflation pressure being relieved when oil price pressures are relieved. We also see that growth is not really intensifying. Meanwhile, there is still a good deal of acrimony over not just what terms Brexit will produce but over the bargaining framework that will be used to address it. Right now the U.K. and the EU have no meeting of the minds about how to come to the bargaining table let alone what deal to strike. The once hopeful view that there would be stimulus in the U.S. has run afoul of politics and Democrats are being uncooperative and Republicans cannot agree on what they really want to do. Together those facts keep policy change on the sidelines. As a result, change still hangs in the balance. The Fed may be embarked on a tightening course, but it is far from clear to me that it will be able to stay that course. Meanwhile, Europe could remain in its current position with its pedal to the metal for some time to come.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief