Global| Apr 21 2017

Global| Apr 21 2017Fresh Six-Year PMI Highs for Euro Area; Moon Shot, High Orbit Or Decaying Orbit?; Time to Play: 'Guess That Trajectory!'

Summary

You have to admit, it's getting better, it's getting better, All the time (it can't get no worse) Lennon and McCartney Well, of course, things can always get worse. But the euro area is getting better, and my reference to the famous [...]

You have to admit,

You have to admit,

it's getting better,

it's getting better,

All the time (it can't get no worse)

Lennon and McCartney

Well, of course, things can always get worse. But the euro area is getting better, and my reference to the famous Beatles' lyric is to underscore that while things are getting better they are still hardly tip-top. The 'fresh six-year high' is a pleasant surprise that continues, but it is hardly a high hurdle or certainly a bar you could easily go over like a hurdle but no impediment to a high-jumper or a pole-vaulter. We are not in that sort of world by any stretch. It's a world of some progress and of success compared to our recent past. But this is still slug-it-out slow progress made one step at a time.

The very ubiquity of improvement

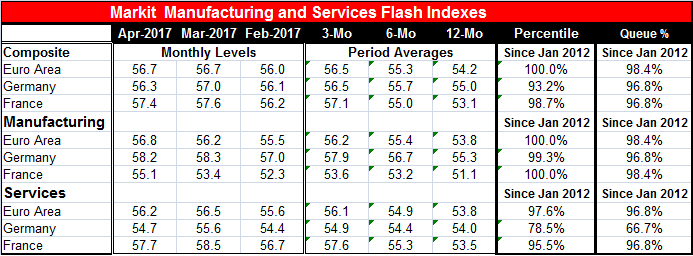

The PMI data are still encouraging. The sequential PMI averages from 12-month to six-month to three-month show that, over ever shorter horizons, the PMIs are stronger and stronger for the EMU, Germany and France - without exception. And this is for a period with some disruption including Brexit, ongoing jitters about the French elections and the Italian political situation as well as a very messy geopolitical background which includes a good deal of uncertainty about what have seemed to be shifting U.S. intentions. There have been ongoing internal quarrels as well between the hard money EMU crowd and others over whether the ECB's policy of stimulus has outlived its usefulness or not. And yet, economic conditions continue to improve...inch by inch...step by step.

PMI perspective

It is important to put these improvements in perspective. PMI gauges are time-sensitive things. They are more like applying percentage change operators to data over time that are NOMINAL data rather than volume data. Not all historic comparisons are going to be valid across such a time series of data. Obviously, in a time of rampant inflation, nominal series will show greater gains than in periods with low inflation and stronger gains may not signal better economic times. However, over any short period with 'roughly similar inflation', the ordinal comparisons/assessments may be valid. Similarly, the PMI gauges are INDICATORS of breadth, not of of strength. And with the economy having been weak for so long, the comparisons in this period are easy comparisons. Improving breadth may not translate into that much more strength. And this is one of the confusions we are working though as indicators (globally) continue to 'indicate' more lift than accounting type data that add things up and produce a true quantitative assessment of events.

The breadth of my breadth is breath-taking

Still, the recovery in EMU is impressive at least for its relentlessness as well as for the breadth of its breadth! The breadth of the improving rebound in is gear for manufacturing and services as well as for the EMU, Germany and France. There is no shoving all that aside. The diffusion gauges tell us that recovery is spreading. Relatively more data-reporters are seeing conditions improve rather than deteriorate and this is good news.

But we should also be careful in assessing this progress and vary cautious about comparing today's PMI levels with periods of similar past PMI gauges. Caveat Emptor (or Caveat PMI'er).

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief