Global| Feb 11 2015

Global| Feb 11 2015French Trade Trends Show Progress

Summary

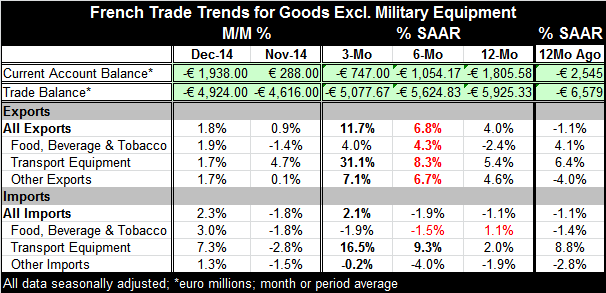

French trade and current account trends are showing progress despite the step back into deficit for France's current account in December. The December current account deficit is still 1.9 billion euros, smaller than it was one year [...]

French trade and current account trends are showing progress despite the step back into deficit for France's current account in December. The December current account deficit is still 1.9 billion euros, smaller than it was one year ago. The 12-month change in the current account deficit is sketching a trend of clear improvement. It looks as though the weaker euro is helping France even if it is working at a slow pace.

French trade and current account trends are showing progress despite the step back into deficit for France's current account in December. The December current account deficit is still 1.9 billion euros, smaller than it was one year ago. The 12-month change in the current account deficit is sketching a trend of clear improvement. It looks as though the weaker euro is helping France even if it is working at a slow pace.

We can see that French exports are gaining pace, up at an 11.7% annual rate over three-months and show steady acceleration from six-months with six-month growth ahead of 12-month growth. While steady progression in these intra yearly metrics is no guarantee, it will continue. It is a hopeful signal and one that is also underpinned by improving year-over-year growth for exports.

While weak imports help France to improve its trade and current account deficit trends, dropping imports are not a sign of a healthy economy. Over time domestic income and demand grow, and imports will tend to expand as well. In modern advanced economies, imports tend to expand faster than GDP. One reason that is not occurring now is because of weak oil prices which reduce the value of nominal oil imports. Weak oil prices should put more money into the pockets of consumers and into the cash registers of businesses paving the way for them to spend more and for imports to reengage with growth. But since early 2013, French import growth year-over-year has been mostly negative. Declining French imports has been more than just a story about weak oil prices for some time.

Still, progress on the export side of the ledger seems quite clear and could be the catalyst for better domestic growth and eventually stronger imports. The weakening euro is already breathing new life into the German economy where forecasts by different agencies (today by DIHK) are being steadily lifted. The Bank of France has lifted its outlook for French growth already.

But the G20 Summit reminds us that competitive devaluations are a risky game and should not be played. We have seen clearly that an ultra-accommodative monetary policy has the result of weakening a region's currency. The impact of the ECB's QE plan on the euro exchange rate wouldn't shock anyone. For now it seems that the needs of Europe are going to be allowed to be met through QE and through the exchange rate effect which may be the most viable channel through which QE will work. But the G20 statement was also a warning not to let such a phenomenon become entrenched. Exchange rates, while having the needed stimulative impact on Europe, are exacerbating trade imbalances. Germany's largest ever trade surplus is getting bigger. The perpetual U.S. trade deficit is again getting larger. The U.S. cannot provide domestic demand to suckle the world back to health although the strong dollar makes it easier for foreign exports to tap into that channel.

We are running policies of expediency and of unsustainability. The late Herb Stein used to say that he did not worry about unsustainable policies because if they were unsustainable they would not be sustained! Oh, that Herb. I think the point of such `worry' is over how policies will cease to be sustainable and that warning is to keep nations from becoming deeply committed to a course of action that will produce distortions and adverse repercussions before those excesses arise and create a backlash. In that context, the embarkation on policies that are unsustainable although immediately helpful chart a risky course of action for the global economy. Whenever a policy helps one country's situation at the expense of another's, something dangerous has been introduced. Trade is about being mutually beneficial. When it is not, it is not the result of free trade and distortions are being spread. Sometimes it takes a while for the ill effects to percolate and mature. Hopefully EMU policy will have exited this policy tack before that happens.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.