Global| Jul 06 2007

Global| Jul 06 2007French Trade Deteriorates While German Foreign Orders Soar

Summary

French exports have relatively long lived and broad based declining trends across industries. This is very different from the German results also reported today that showed such strong orders from overseas. While Germany may have [...]

French exports have relatively long lived and broad based declining trends across industries. This is very different from the German results also reported today that showed such strong orders from overseas. While Germany may have special business ties and niches of strength that help to insulate it from the strong euro, France does not seem to be so lucky. While Mr Sarkozy is out there trying to balance one budget (or to postpone putting it in balance) it looks like he has another deficit reading that is ready to split at the seams, this one for trade.

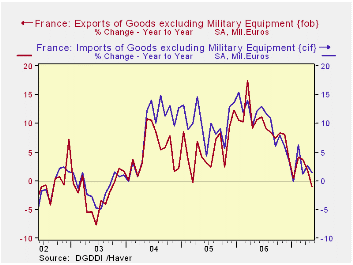

French trends show that despite their proximity and shared currency France and Germany are as different as night and day in some respects. While German order trends for capital goods are very strong, for France actual exports are dropping by 12.3% at an annual rate in the three months ended in May and are lower by 6.3% Yr/Yr. This compares to German foreign order rise of double digits on both those horizons for capital goods. Clearly France is facing a very different situation than Germany. And after also sharing the same business cycle and fiscal issues for a time these two economies are now going their separate ways. Germany has its fiscal situation under control and its MFG sector riding high; and France is trying to postpone its promised adjustment – with the Germans as some of its biggest critics – and its industrial competitiveness seems to be slipping.

It is not as simply as saying there is a capital spending boom in Europe and Germany. If that were so, wouldn’t fellow Euro-zone member France get its share? France is not taking part. Rather Germany, as the most competitive Euro-zone member, is the country that will be the last to feel the effects of the strong euro. German will enjoy a competitive advantage for a while after others have lost it. Is that where we are today? Is that why Germany is still doing well while others are not?

Italy and Spain already are showing some signs of weakness. For Spain it is a clear loss of momentum in industrial output that drops the hint. For Italy weakness is a little more broad-based. The OECD leading indicators still have France on an upswing, but that may be more domestic in nature. France’s external sector seems to be lacking, judging from export trends. Clearly this is a good time to look at the various Euro-zone countries as distinct entities and see which of them – if any - is hurting from the strong Euro. This will be a theme in the coming months.

| m/m% | % SAAR | ||||

| May-07 | Apr-07 | 3M | 6M | 12M | |

| Balance* | -€€ 3,015.00 | -€€ 2,493.00 | -€€ 2,364.33 | -€€ 2,402.33 | -€€ 2,310.42 |

| Exports | |||||

| All Export | -1.0% | -1.4% | -5.5% | -4.0% | -1.0% |

| Capital Goods | -6.5% | 0.6% | -12.3% | -9.6% | -6.3% |

| Motor Vehicles | -2.4% | -1.4% | -13.1% | -6.4% | -5.2% |

| Consumer Goods | -0.2% | -0.6% | -0.4% | -3.7% | 0.4% |

| IMPORTS | |||||

| All Import | -0.6% | 2.0% | -2.4% | 0.5% | 1.4% |

| Capital Goods | 0.6% | -0.1% | -16.7% | 1.0% | -2.6% |

| Motor Vehicles | -0.1% | -1.4% | -4.2% | 9.1% | 3.7% |

| Consumer Goods | -0.2% | -0.2% | -3.2% | -4.1% | 2.6% |

| *Eur Blns; mo or period average | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief