Global| Apr 28 2008

Global| Apr 28 2008French Service Sector Outlook and Climate Gauges Slip

Summary

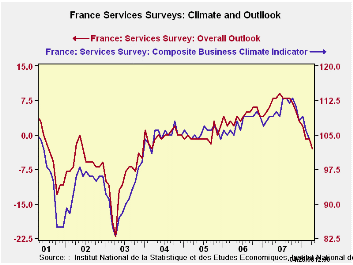

The French service sector climate indicator is down sharply in the current month form 104 to 102 after being as high as 109 in January to start the year. Service sector sentiment has been steadily eroding. The climate indicator is in [...]

The French service sector climate indicator is down sharply in

the current month form 104 to 102 after being as high as 109 in January

to start the year. Service sector sentiment has been steadily eroding.

The climate indicator is in the 63 percentile of its range. The gauge

of employment expected in the next three months is lower in the 58th

percentile of its range.

The slip in the service sector is both steady and widespread.

France is coming off a period when the service climate has been in the

top 94th percentile of its range. But conditions in France have been

deteriorating rapidly. Morale and activity gauges from other large EMU

economies have been off peak. France itself is succumbing to these

adverse pressures. French Finance Minister Christine Lagarde said

Sunday that the Federal Reserve has a policy of very low interest rates

and the ECB has kept interest rates elevated and that the differential

in rates between the two is a little too big at the moment. This

continues a policy of being obliquely critical of the tight ECB

interest rate policy.

| France INSEE Services Survey Jan 2000-date | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Apr-08 | Mar-08 | Feb-08 | Jan-08 | %tile | Rank | Max | Min | Range | Mean | |

| Climate Indicator | 102 | 104 | 106 | 109 | 63.3 | 51 | 113 | 83 | 30 | 102 |

| Climate: 3-Mos MAV | 104 | 106 | 108 | 109 | 68.7 | 48 | 113 | 85 | 28 | 102 |

| Climate: 12-Mos MAV | 109 | 110 | 110 | 110 | 94.1 | 10 | 110 | 91 | 20 | 102 |

| Outlook | -3 | -1 | -1 | 2 | 61.3 | 55 | 9 | -22 | 31 | -1 |

| Sales | ||||||||||

| Observed 3-Mos | 9 | 17 | 13 | 13 | 69.0 | 28 | 18 | -11 | 29 | 6 |

| Expected 3-Mos | 9 | 5 | 10 | 14 | 70.4 | 36 | 17 | -10 | 27 | 7 |

| Sales Price | ||||||||||

| Observed over 3-Mos | 5 | 1 | 1 | 1 | 75.0 | 2 | 8 | -4 | 12 | 0 |

| Expected over 3-Mos | 2 | 1 | 0 | 0 | 70.0 | 10 | 5 | -5 | 10 | 0 |

| Employment | ||||||||||

| Observed over 3-Mos | 11 | 17 | 17 | 7 | 78.6 | 9 | 17 | -11 | 28 | 4 |

| Expected over 3-Mos | 9 | 12 | 19 | 14 | 58.3 | 17 | 19 | -5 | 24 | 5 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief