Global| Mar 13 2015

Global| Mar 13 2015French Sales Volumes Recover in February

Summary

French sales volumes recovered in February, rising by 1.2% after two straight monthly declines in excess of 1%. In the last four months, French sales volumes have moved by more than 1% in each month: twice up and twice down. This is [...]

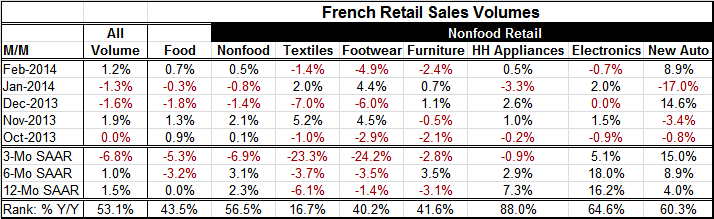

French sales volumes recovered in February, rising by 1.2% after two straight monthly declines in excess of 1%. In the last four months, French sales volumes have moved by more than 1% in each month: twice up and twice down. This is quite a period of volatility for sales. This Bank of France survey does not do much to clarify trends.

French sales volumes recovered in February, rising by 1.2% after two straight monthly declines in excess of 1%. In the last four months, French sales volumes have moved by more than 1% in each month: twice up and twice down. This is quite a period of volatility for sales. This Bank of France survey does not do much to clarify trends.

Growth rates show overall sales still declining over three months although up over six months and 12 months. Still, there is not much sign of recovering momentum with six-month growth weaker than 12-month growth. Food sales show progressive weakness with sales down at a 5.3% pace over three months and at a -3.2% pace over six months while flat over 12 months. Nonfood sales are falling at 6.9% annual rate over three months but show a pickup over six months compared to 12 months. That makes momentum uncertain.

The detailed nonfood categories show extreme sales weakness over three months for textiles and footwear and negative growth on all horizons for each. Electronics and auto sales show all positive growth rates with autos showing a clear progression to stronger growth. Furniture and household appliances show mixed growth rates but household appliances show a clear deteriorating trend.

On balance, the BoF survey is not very illuminating. French sales trend remain mixed. The building momentum in auto sales looks like good news since that big ticket item is an important barometer for consumers. But if the recovery is uneven, that sector could be kept active by the part of the population experiencing improved conditions. With bifurcated recoveries everywhere, there are few clear indications that growth taking hold. While the pick-up in auto sales is reassuring, the downshift in appliance sales is disconcerting.

Signals from the French economy and actual performance remain mixed. Hopes are high in France and in Europe in general that the ECB's QE program will help to turn the corner on growth. To me, QE still seems to be too late and is working within a too-flawed European financial structure to be a real hit. But time will tell. On the other hand, the weak euro is something that can help to transform growth in the euro area but at a cost to other economies.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief