Global| Jul 13 2018

Global| Jul 13 2018French Retail Sales Rebound In June But Do Not Convince

Summary

French retail sales rebounded in June after falling for two consecutive months. Gains earlier in the year in the February and March were quite strong, but April brought a deep decline; May sales were lower- but essentially flat- and [...]

French retail sales rebounded in June after falling for two consecutive months. Gains earlier in the year in the February and March were quite strong, but April brought a deep decline; May sales were lower- but essentially flat- and now volume is back up solidly in June. But French trends are not reassuring. Clearly, this is a volatile series. But it also shows signs of losing momentum.

French retail sales rebounded in June after falling for two consecutive months. Gains earlier in the year in the February and March were quite strong, but April brought a deep decline; May sales were lower- but essentially flat- and now volume is back up solidly in June. But French trends are not reassuring. Clearly, this is a volatile series. But it also shows signs of losing momentum.

Even the year-to-year gains are volatile, but they clearly are also moving lower (see Chart).

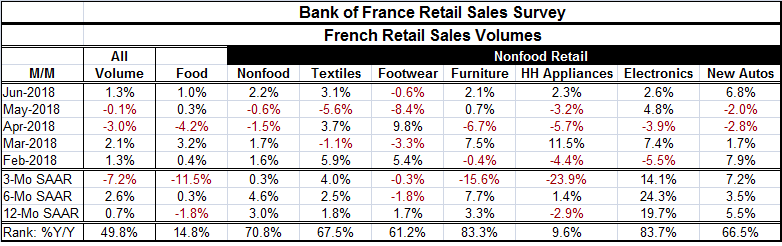

To help evaluate the relative strength of retail sales, I calculate the rank position of overall volume as well as for all retail components in addition to momentum metrics (sequential growth rates from 12-month to six-month to three-month).

Assessment of current retail strength

Retail sales volume growth over 12 months in June has a queue or rank standing at 49.8 %, nearly on top of its historic median (which occurs at a rank standing of 50%). Still, only two spending components are below their respective medians; they are foods and household appliances. Nonfoods as a whole have a 70th percentile standing. Within nonfoods, textiles, footwear and new auto sales have standings for their 12-month growth rates around their respective two thirds mark. Appliance-spending, as noted already, is very weak. But spending on furniture and on electronics stands in the top 17th percentile among historic growth rates for each of these categories. French spending seems to have a lot of irregularities associated with it.

The sequential growth rates offer us no clear view of French sales momentum for total sales volumes or for any category-save one. Spending on textiles grows from a 1.8% pace over 12 months to 2.5% over six months and steps up to a 4% pace over three months. Spending on nonfoods generally is positive on all horizons as is spending on electronics and new autos. But none of these categories show any accelerating or decelerating trend. Still, new auto spending is consistently solid and spending on electronics is consistently strong, well into double digits on all horizons.

Growth in the EMU generally has stepped back and just yesterday the EU Commission cut its outlook for growth for the euro area for the year as a whole. For France, its June PMI gauges for services and manufacturing have slipped below their six-month and 12-month averages. The French PMIs have que percentile standings over the past five years that place them in about the top one third of their range which is a common standing for consumer spending categories in the table and close to what is posted for nonfoods as well. French trends are not poised on the razor’s edge of decline, but neither are they very solid or reliable.

On balance, the ranking for French retail overall being at its median is not reassuring. And spending on appliances has been on the weak side for nearly two years- it is nothing new. Overall sales growth is under 1% over 12 months and the overall annual growth rate has been playing hide and seek with the zero line since October of last year. Over those eight months, annual retail sale growth rates are below zero on five occasions and that is not a reassuring trend.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief