Global| Mar 26 2008

Global| Mar 26 2008French Production Trend is Lower but Optimism is Intact

Summary

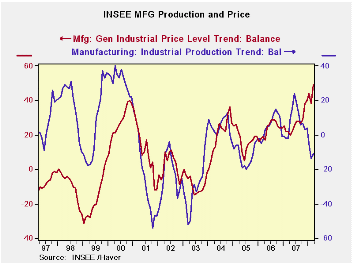

The chart on the left shows that price trends continue to press higher in France but the production trend is sharply lower. For total industry we find similar results to those in manufacturing. The recent trend of production at -11 is [...]

The chart on the left shows that price trends continue to press higher in France but the production trend is sharply lower.

For total industry we find similar results to those in manufacturing. The recent trend of production at -11 is below its mid-point, standing at the 46th percentile of its range. But the likely trend reading at 51 is in the 87th percentile of its range, a strong reading. Despite the current slowing and despite high energy and commodity prices and despite financial turmoil and despite a super strong and a still-rising euro, French industrialists have maintained their optimism. Orders are in the 74th percentile of their range with foreign orders relatively weaker in the 69th percentile of their range. This is unusual since in other large EMU countries foreign orders have been relatively stronger than domestic orders.

France is an interesting case in several respects. Its budget

is now expected to overshoot its target as growth in revenues slow. The

Finance Ministry is scaling back its forecast for growth. It is an odd

time for businesses to be looking for the future trend in output to

deviate so much and to become so much stronger than the current trend

in output. Nonetheless, that is what the survey says.

| INSEE Industry Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| Feb 08 | Jan 08 | Dec 07 | Nov 07 | Percentile | Rank | Max | Min | Range | Mean | |

| Climate | 107 | 108 | 109 | 110 | 68.0 | 64 | 123 | 73 | 50 | 101 |

| Production | ||||||||||

| Recent Trend | -14 | -6 | 4 | 3 | 43.1 | 134 | 44 | -58 | 102 | -5 |

| Likely trend | 43 | 47 | 44 | 43 | 79.2 | 8 | 63 | -33 | 96 | 8 |

| Orders/Demand | ||||||||||

| Orders & Demand | -1 | -1 | 1 | 4 | 70.1 | 46 | 25 | -62 | 87 | -14 |

| Foreign Order s& Demand | 1 | 0 | 6 | 4 | 66.3 | 67 | 31 | -58 | 89 | -10 |

| Prices | ||||||||||

| Likely Sales Prices Trend | 17 | 12 | 12 | 10 | 85.1 | 12 | 24 | -23 | 47 | 1 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief