Global| May 12 2014

Global| May 12 2014French Outlook Is Trimmed

Summary

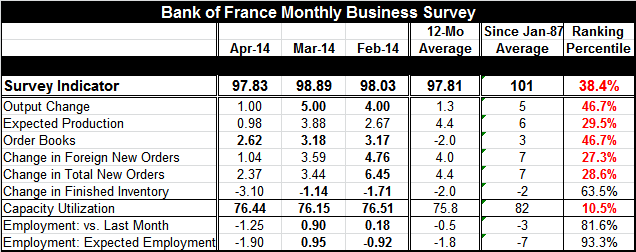

The Bank of France survey backtracked in April, falling to a value of 97.83 from March's 98.89. The index has a percentile standing in its historic range of 38.4%; it is weaker than its April standing only about 38% of the time. The [...]

The Bank of France survey backtracked in April, falling to a value of 97.83 from March's 98.89. The index has a percentile standing in its historic range of 38.4%; it is weaker than its April standing only about 38% of the time.

The Bank of France survey backtracked in April, falling to a value of 97.83 from March's 98.89. The index has a percentile standing in its historic range of 38.4%; it is weaker than its April standing only about 38% of the time.

The Bank of France has cut its outlook for growth. Its previous estimate of Q1 growth of 0.7% for "mid-2014" has now been reduced to 0.2% for the second quarter, the same as the estimate for the first quarter. The French economy continues to flounder.

None of the key indicators from the French survey are remotely strong. Capacity utilization is so weak that it is only weaker 10% of the time.

The relatively strongest components of the survey are for expected employment and employment last month. Employment last month, while at a -1.25 raw reading, compared to a mean response of -3 and stands in the 81st percentile of its historic queue. Expected employment is even stronger with a reading in the 93rd percentile (stronger only 7% of the time). But these readings are way out of whack with the rest of the survey.

Among the activity components of the rest of the survey, output change and the order book metrics are the relatively strongest readings in the latest survey. These two indicators stand below the 50% level which marks their respective medians.

It seems that the employment responses in the survey embody unrealistic optimism compared with the rest of the report. Either that or employment expectations and assessments have been reset to a much lower range. Inventories are high, standing in the 63rd percentile of their historic queue. With inventories relatively high and capacity use so low, the outlook for employment should not be so strong. Orders are very modest as is the output change. Why should the outlook for employment be so robust? Employment traditionally is a lagging variable.

On balance, the French survey is disappointing. As it was released, the Bank of France announced its reduced expectations for growth. France continues to struggles as Hollande looks for ways to stimulate growth without much success and while the country continues carrying a large debt burden.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief