Global| Sep 25 2018

Global| Sep 25 2018French Manufacturing Takes a Sizable Step Back

Summary

France's INSEE manufacturing survey fell sharply as the headline climate index shed the better part of three points dropping to 107.0 in September from 109.7 in August. The index has fallen more sharply than this less than 20% of the [...]

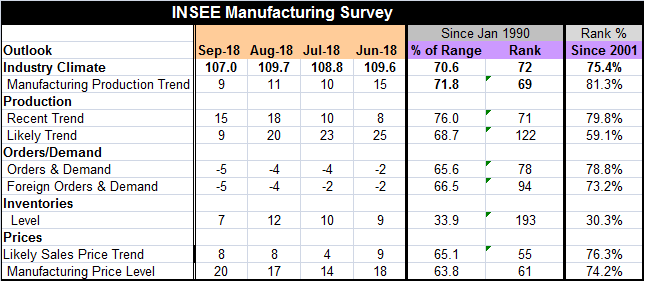

France's INSEE manufacturing survey fell sharply as the headline climate index shed the better part of three points dropping to 107.0 in September from 109.7 in August. The index has fallen more sharply than this less than 20% of the time since 2012. The new standing for the climate index is in the 75th percentile of its historic queue of data, leaving it right at the border of the top 25th percentile of its historic queue of observations.

France's INSEE manufacturing survey fell sharply as the headline climate index shed the better part of three points dropping to 107.0 in September from 109.7 in August. The index has fallen more sharply than this less than 20% of the time since 2012. The new standing for the climate index is in the 75th percentile of its historic queue of data, leaving it right at the border of the top 25th percentile of its historic queue of observations.

Manufacturing has been showing slippage in the EMU since about the turn of the year. France had been the fastest improving economy in the EMU around the turn off the year; now its manufacturing sector is slipping at a noticeable pace.

Still, the assessment of the manufacturing production trend dropped by only two points this month and stands in the 81st percentile of is historic queue of data. The recent trend reading shed three points and maintains a 79th- nearly an 80th - percentile standing. But the likely trend fell by 11 points from a reading of 20 in August to reading of 9 in September. That dropped its standing to the 59th percentile of its historic queue of data and tells volumes about where industry thinks it is headed. A reading at the 59th percentile is still a 'firm' reading but it does not leave much wiggle room for above-median growth since the 50th percentile is the median level and typically the statistical distribution of values tightly cluster around the medians so that a value that stands at its 59th percentile would not be far above its historic median. Still, the 'likely trend' reading has been sporadically much weaker than the recent trend since late-2016, a time during which the recent trend continued to rise. However, in 2018 the recent trend seems to be flattening out as the likely trend has dived to a lower standing.

Expectations aside for now, orders and demand, including foreign orders and demand, each slipped by only one point month-to-month. And despite their negative value, those survey values have a 73rd to 78th percentile standing in their respective historic queues of data. Orders are still on the solid side showing above median growth even though the raw reading signals 'contraction.' Inventories are at a low 30th percentile standing.

Price readings, which include the likely price trend and the manufacturing price level, demonstrate mid-70th percentile standings. The likely trend was steady this month, but the manufacturing price level notched three points higher.

French services

There are also service sector readings available from INSEE for September. These readings are uniformly more moderate with the climate gauge having a 61st percentile standing. The overall outlook has a 68 percentile standing. Observed sales have a 52 percentile standing (barely above its median). Expected sales have a 67th percentile standing. Observed employment has a 48th percentile standing with expected sales at a 64th percentile standing. These standings are clustered around their respective two-third marks in terms of their historic queue or rank standings. That is a sort of netherworld of readings. It is above median, not strong and not threatening growth sustainability either. Some might think of it as a set of goldilocks readings, but the corresponding growth rates may not be good enough for that. To flesh this out, look at raw diffusion scores. Four of the components, observed sales, observed sales prices, the expected sales price, and the observed employment trend have raw diffusion scores that are only one point above their period means. Expected sales and expected employment are each four points about their respective means. The overall expectation is seven points above its expected mean. Why with such weak underlying data is the outlook seemingly stronger?

These details tell us that the 'good news' in the services sector (above-median readings) is on thin ice. Readings that are pinned to actual current trends in this survey are uniformly low while several 'expected values' are higher, indicating that future trends are about to pick up or that optimism is still in gear from the past strong trend despite the fact that that strength has eroded. Denial, like hope, springs eternal.

France - all things considered - seems to be in a slowing mode. And despite its clear policy success in 2017, it seems to be running out of gas in 2018. Policymakers in the EU and ECB are still upbeat. EU officials are still taking a tough line on Brexit as if how they treat the U.K. does not matter to them. Italy is in a swirl of change. Mario Draghi is taking a page out of the Fed's book and trying to project higher inflation to justify a policy switch to a firmer stance on the horizon. But do any of these policy shifts make allowances for the fact that the EU and EMU are not the U.S.? This optimism in EMU growth and fear/forecast of higher inflation has no basis in current euro-reality. France is just the first to go through this impending baptism of slower growth and the angst it will bring. It is in its early stages so continued denial seems likely.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief