Global| Oct 22 2020

Global| Oct 22 2020French Manufacturing Steps Back After Five Months of Gains

Summary

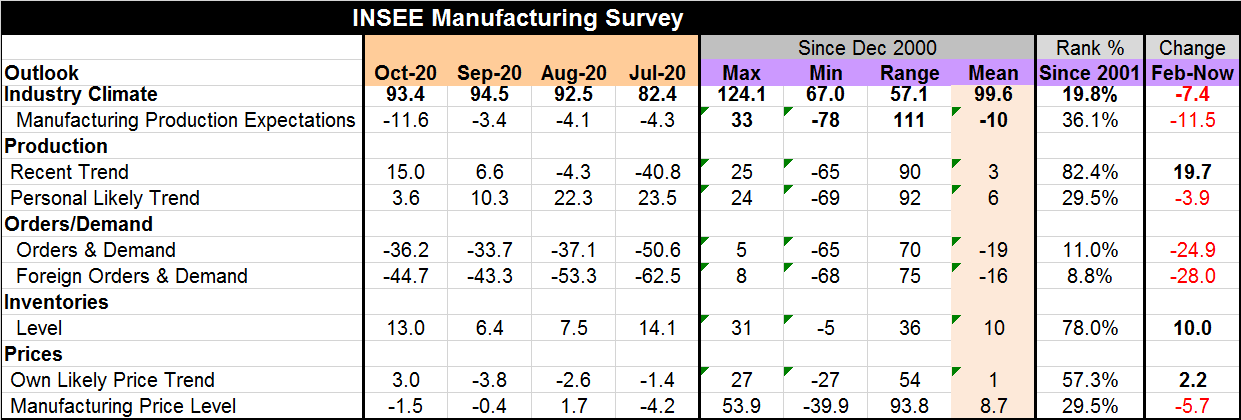

The French INSEE survey shows a reduction in the industry climate gauge in October as that gauge drops to 93.4 from 94.5 in September marking the first decline after five straight months of expansion. This basic table, which I use [...]

The French INSEE survey shows a reduction in the industry climate gauge in October as that gauge drops to 93.4 from 94.5 in September marking the first decline after five straight months of expansion. This basic table, which I use frequently to vet this report, has been amended with the appending of the far right column, a measure of the change to date from the February value for each component. What we find is that after five straight monthly increases and now a small monthly set back (a drop of 1.1 points month-to-month), the October index is some 7.4 points below its February value. February was chosen because it was the last month before the virus impact hit hard. But the industry climate gauge made its local peak in January; the short fall from the January level would be slightly larger.

The French INSEE survey shows a reduction in the industry climate gauge in October as that gauge drops to 93.4 from 94.5 in September marking the first decline after five straight months of expansion. This basic table, which I use frequently to vet this report, has been amended with the appending of the far right column, a measure of the change to date from the February value for each component. What we find is that after five straight monthly increases and now a small monthly set back (a drop of 1.1 points month-to-month), the October index is some 7.4 points below its February value. February was chosen because it was the last month before the virus impact hit hard. But the industry climate gauge made its local peak in January; the short fall from the January level would be slightly larger.

Three components improve from their February levels

Interestingly, that final column shows only three survey items higher in October than their levels in February. These three components are (1) recent trend, (2) inventory level, and (3) own likely price trend. None of these are surprising. As we note above, the recent trend has been higher in each of the previous five months as the climate index has improved. The 'industrial trend expected' rose in four of the five previous months, but it also has fallen this month as well as last month. The statement about what that trend has been is not necessarily denial that the worm for trend may have turned. Also, while output has been picking up apparently, demand has not outstripped it; as a result, inventory levels are higher now than in February. That is not a positive development. The own likely price trend just shifted from a string of negative readings to a positive one in October leaving it above is positive February level. That was not the case in previous months so this movement is encouraging and is a new development in the survey. However, survey participants had this response at the same time their estimate for the overall manufacturing price level was for more weakness month-to-month as well a reveling a weaker reading in October than in February. So this 'own-price' assessment may be somewhat selective and a result of wishful thinking. Why do 'most survey participants' think their own price can rise when prices in general will soften? That is a red flag.

Most components are still below their February levels

As I noted above, industry climate gauge was among the items that stepped back in October after five months of improving. Manufacturing production expectations also stepped back in a sharp monthly deterioration, dropping to -11.6 from -3.4 in September. Also while the recent trend was assessed as higher, the personal (own firm) likely trend is not assessed as better; in fact, it makes a sizeable step back to 3.6 in October from 10.3 in September and shows deterioration from February. Firms are not wearing rose-colored glasses when it comes to assessing their own output trend. Orders & demand as well as foreign orders & demand both step back in month-to-month drops either 2.5 or 1.4 points, significant but small decrements; however, both of them compared to February levels are lower by an outsized 25 to 28 points-- weaker readings by far. Indeed the percentile queue standings (second to last column in the table) show these two components as having the weakest standings among all the components in the survey. As already noted, the overall macro price trend for manufacturing is weaker than its February level and it has now weakened for two months in a row.

About the survey

This is a 'supply side survey,' a survey of industrial and manufacturing, a survey of output and output expectations, and related data. It is notable that the weakest part of the survey on this sector is the respondents' perceptions of the orders and demand that either could, will or won't keep the sector operating – a factor beyond their control.

The survey's apparent message is grim

The highest percentile rank (or queue) standing in the table are for the recent trend of production and for inventories – both of them are around the 80th percentile region. Having high inventories is either a danger sign of inventory excess or a sign of optimism about the future. The strength in the recent trend (also an 80th percentile reading) may feed the notion of high inventories as optimism. And firms do make judgements from past trends (how else?). But the personal likely trend reading is off sharply for two months running and it has only a weak 29.5 percentile standing for its October reading. And since orders and demand are so weak, it seems more likely that the past buoyant trend is and will remain a thing of the past. The future is grimmer. Inventories are becoming bloated relative to need and the optimism about 'own-price' trends is misplaced.

The virus is the reason yet again

This is a harsh view of the survey which itself is not crystal clear and is subject to differing interpretations. But one reason for the creeping pessimism in the survey may also be the explosive nature of the ongoing French virus infection rate (here). At first, France had a relatively low infection peak at 7,578 cases per day on the last day of March. Since then the infection rate receded and remained controlled until it began to rise mildly at the end of July and early August. By September 5, French infections had shot up to 8,975 per day, a new peak. By October 17, infections had exploded to 34,427 per day and have since been volatile in a higher and rising range of bad outcomes. Measures of mobility show that mobility in French has been reduced and is being further enforced and more lockdown procedures are being put in place.

New virus findings

The FT reports (here) that this time around (second wave) the virus has been less lethal for several reasons: (1) there is more testing (uncovering more cases that previously might have gone unnoticed and therefore uncounted), (2) the people getting infected this time are younger and healthier, and (3) that even among those admitted to hospitals the proportion of admissions that die within 28 days is down to 27% from 39% previously.

France, the economy and the virus

All in all, France, like most other countries, is taking steps to stop the spread and to reduce infection rates to something much lower. Even though infection per se is not as lethal as it once was, it is also clear that while health officials know certain things about vulnerable populations and the like there are also unknown factors such as why some people get sick and stay sick for long periods. There is some speculation that blood types may matter. Clearly a person's physical shape and healthiness is an issue as well – data bear this out time and time again. As countries take steps to mitigate infection, they try to use what they know about these risk factors to improve results. But in the end, whether it is NYC or Paris, France, the approach involved is a lockdown of some sort. But the lockdowns are becoming more localized, more focused. In the end, that may be the best news for the economy as localized lockdowns are less likely to have as pronounced macroeconomic effects. But none of that changes the discussion about France that is in the middle or a real outbreak and is taking some substantial growth-impeding steps to stop the spread.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief