Global| Oct 23 2013

Global| Oct 23 2013French Manufacturing Is Doing Better...But Not Much Better

Summary

The chart that maps the survey responses on the outlook for French manufacturing industrial production and prices shows that IP expectations are moving upward rapidly while the prices expectations index, after some very moderate [...]

The chart that maps the survey responses on the outlook for French manufacturing industrial production and prices shows that IP expectations are moving upward rapidly while the prices expectations index, after some very moderate increases, has backtracked a tad in October. We are getting separation between expected activity and expected inflation.

The chart that maps the survey responses on the outlook for French manufacturing industrial production and prices shows that IP expectations are moving upward rapidly while the prices expectations index, after some very moderate increases, has backtracked a tad in October. We are getting separation between expected activity and expected inflation.

Gaps between the survey values for IP and prices have been observed in the past and have been as large or larger than the one we see now. But what is unusual this time is the height of the IP assessment vs. the low level (still quite near zero) assessment for expected prices. In the past with an expected IP level this high, expected prices would be advancing strongly with an accelerating trend. Unless that phenomenon appears in the next few months, this will mark a strong exception with the past.

Spain has just announced a small but positive GDP figure; its emergence from recession is being applauded. Yes, but only if it lasts. Spain does not have much momentum and neither does the rest of Europe. Is France hoping that the rest of Europe will carry it higher?

France's strong expectations in this INSEE report are encouraging. However, US export and import data just released for September still show trends too weak for there to be much of a pick-up in the rest of the world. French optimism does not have that much to support it- but there it is.

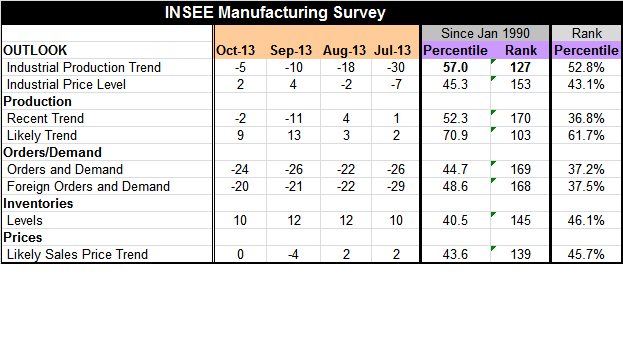

Still the INSEE results show that the outlook for the Mfg production trend at -5 is up from -10 in September, -18 in August, and -30 in July. The upward progress is extremely rapid. The five-month ascent of the outlook for the IP index is the ninth largest five month gain in the history of this index making this ascent a top 3% event. Along with this, the outlook for the industrial price index has risen from -8 to +2, a still low value. The expected IP trend sits in the 52.8 percentile of its historic queue compared to expected prices that are in the 43.1% of their historic queue.

Current production has not advanced as much as its expected or `outlook' counterpart. The recent trend for IP is evaluated at -2, up from -11 in September, but on a net basis higher by only 2 points over the last five months. Expectations for IP are clearly outstripping IP itself. IP (recent trend) still sits at a low, 36.8 percentile of its historic range.

Orders and demand are still very weak at a reading of -24. They are up fractionally in recent months and sit in the 37.2 percentile of their historic range. Orders are in a similar spot to the recent production trend. Foreign orders are at a -20 reading and have improved a bit more in recent months (than overall orders). Still this reading is only in the 37.5 percentile of its historic queue.

The service sector survey is not much better as its overall climate indicator stands only in the 29th percentile of its historic range. The observed and expected sales performance readings are in the bottom 25% of their respective historic ranges. Observed employment trends in services are in the 30th percentile of their historic queue; but expected employment is stronger in the 42.7 percentile of its historic queue. There is that optimism again.

On balance, French manufacturers are upbeat about the future even though we cannot see any reason for it from the components of their business on which they provide judgment in the survey. Orders are weak. Current production is weak and it is not improving rapidly. Expectations for the future, however, are on a real tear. In services all the recent readings are weak but expectations for employment (still weak) are better.

One must wonder if there is something fanciful to these expectations. The world around France may be doing somewhat better, but improvements in France's orders from abroad do not reflect any transmission of that improvement. For the moment, we must take these assessments on the French economy to heart in that they are weak assessments.

Nevertheless, the French are optimistic about the future- even on these weak conditions! We don't know why from everything they have told us, there is no reason for optimism. But maybe they know something we don't, something that these surveys do not capture. Or.maybe not. Optimism may simply be a way to cope with such bad economic times. Hope springs eternal. But `hope' should not be an input in a forecasting process.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief