Global| Dec 21 2017

Global| Dec 21 2017French Manufacturing Index Takes a Small Countertrend Step Back

Summary

France's INSEE index shows that the industry climate has backed off in December to a reading of 112.1 from 112.8 in November. Despite the drop, it is still a strong reading. In fact, it is stronger than every reading previous to [...]

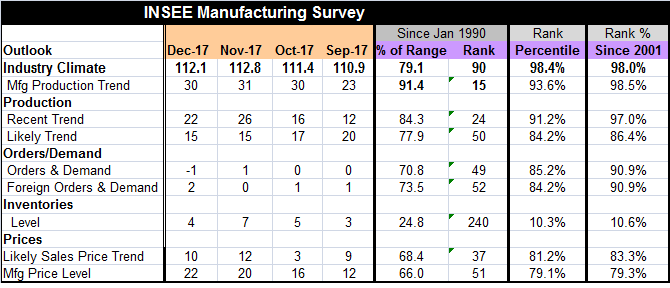

France's INSEE index shows that the industry climate has backed off in December to a reading of 112.1 from 112.8 in November. Despite the drop, it is still a strong reading. In fact, it is stronger than every reading previous to November back to December 2007 making this November reading the penultimate reading over the last decade.

France's INSEE index shows that the industry climate has backed off in December to a reading of 112.1 from 112.8 in November. Despite the drop, it is still a strong reading. In fact, it is stronger than every reading previous to November back to December 2007 making this November reading the penultimate reading over the last decade.

The chart shows production expectations for manufacturing and juxtaposes it to the service sector climate reading that has continued to make solid gains. Obviously, the step-back this month looks more like a pot-hole in the road of growth than like a fork in the road. Germany's IFO reading also took an unexpected small setback. Economic data simply do not normally expand monotonically. Every wiggle is not an indicator of a change direction. Certainly for France the trend still seems strongly in place.

The French industrial climate reading has been as high or higher only 2% of the time since 1991 and the production trend has been as good or better less than 1.5% of the time.

The recent trend in production has been as good or better only 3% of the time despite its four-point drop-off in December. November had seen a huge jump in that index to 26 from October's 16; the substantial four-point drop off to 22 this month still leaves the trend reading strong and with positive momentum.

The likely trend, however, is more circumspect. That reading has been simmering lower over a series of months and is, in fact, unchanged month-to-month in December. It has been higher rough 16% of the time since 2001.

Orders and demand show a slight slippage month-to-month and a net lower reading compared to the last three months but a much stronger reading compared to earlier months. Foreign orders and demand have moved higher this month and are similarly much stronger than earlier months. Both overall and foreign orders and demand have standings that lie in their respective top 10 percentiles back to 1991.

Price expectations are blossoming. The likely sales price trend fell in December but remains above levels for earlier months. The manufacturing price level continues to work higher. Both of these metrics have standings in either the high 70th percentile or lower 80th percentiles of their respective queues of values, roughly the same signal. Inflation and prices are being pressured up to some extent.

The service sector readings show similar sorts of strong readings with slightly less zest than for manufacturing. However, the outlook for services still represents a strong reading and one that has been higher only about 7% of the time. Plus in the service sector price expectations are slightly softer compared to manufacturing.

The sum up for France from these surveys is still quite upbeat. The drop off in the manufacturing headline does not seem to be a significant event. The expansion trend appears to be in place and we find sympathetic and reinforcing growth trends in the manufacturing as well as in the services sectors. French growth appears to be on solid footing and the expansion in price expectations at this point is not enough to excite or impress the ECB but they do seem to reinforce the notion of the French economy as 'heating up.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief