Global| Aug 11 2008

Global| Aug 11 2008French IP is Losing MomentumAcross Sectors

Summary

In June French IP fell by 0.4%, unexpected weakness. It has now dropped in two of the past three months and is falling sharply in the current quarter, at a -5.3% annual rate. Italy, like France, has had a very weak May but managed [...]

In June French IP fell by 0.4%, unexpected weakness. It has

now dropped in two of the past three months and is falling sharply in

the current quarter, at a -5.3% annual rate. Italy, like France, has

had a very weak May but managed some output increases in June. Still,

Italy’s IP is dropping in Q2 as well.

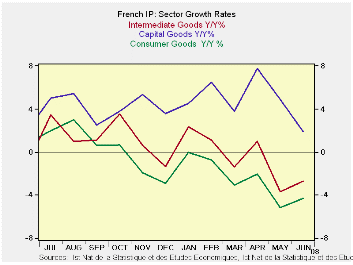

The sequential growth rates in France shows a clear ongoing

deterioration. This is what the OECD trend-adjusted leading indicators

pointed to last week. France has more severe downward momentum that

most other EMU nations.

Italy’s path lower is more jagged with a rise in output over

six months and an actual ongoing acceleration in the output of consumer

goods, 12mo to 6mo to 3mo. This is very odd since the export markets

seem to be declining for other EMU countries (like Germany) and Italy’s

own domestic demand for consumer goods is quite weak. Still it may be

that Italy’s consumer goods output is more volatile than it is strong.

The recent monthly results have been extremely choppy.

| French IP excluding construction | |||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | Jun-08 | May-08 | Apr-08 | 3-mo | 6-mo | 12-mo | Quarter-to-date |

| IP total | -0.4% | -2.9% | 1.3% | -7.8% | -4.9% | -1.6% | -5.3% |

| Consumer | 0.5% | -1.5% | 0.0% | -3.9% | -1.8% | -4.3% | -7.4% |

| Capital | -1.0% | -1.2% | 2.4% | 0.3% | 1.2% | 1.9% | 3.5% |

| Intermediate | -0.4% | -2.9% | 1.3% | -8.0% | -4.7% | -2.7% | -7.5% |

| Memo | |||||||

| Auto | -2.9% | -7.6% | 2.8% | -27.6% | -21.8% | -5.7% | -21.2% |

| Italy IP excluding construction | |||||||

| Saar except m/m | Jun-08 | May-08 | Apr-08 | 3-mo | 6-mo | 12-mo | Quarter-to-date |

| IP-MFG | 0.2% | -1.5% | 0.4% | -3.3% | 1.5% | -2.0% | -2.5% |

| Consumer Goods | 1.9% | -3.2% | 2.9% | 6.1% | 3.7% | 1.4% | -0.1% |

| Capital Goods | -0.8% | -2.5% | 1.7% | -6.4% | 8.3% | -1.9% | -2.3% |

| Intermediate | 0.5% | -1.7% | 0.5% | -2.5% | -1.3% | -3.7% | -3.9% |

| Memo | |||||||

| Transportation | -1.3% | -1.5% | -0.5% | -12.3% | 7.6% | -1.6% | 1.1% |

by Louise Curley August 11, 2008

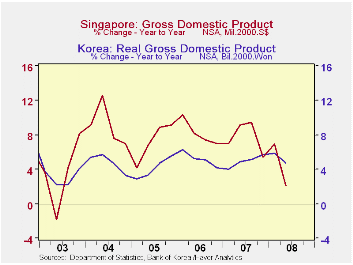

Second quarter data on the national accounts of the emerging countries of the Pacific Rim are becoming available. More than two weeks ago, South Korea announced that its seasonally unadjusted second quarter GDP increased 4.8% over the corresponding quarter of last year, down from a 5.8% increase in the first quarter. Today, Singapore announced that its second quarter increase over the same quarter of last year was up only 2.1%, compared with 6.9% for the first quarter. The year over year changes in the seasonally unadjusted real GDP for South Korea and Singapore are shown in the first chart.

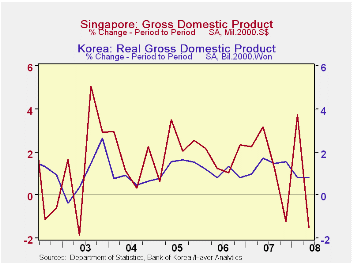

On a seasonally adjusted basis, South Korea's GDP increased 0.83% from the first to the second quarter, the same as in the first quarter from the fourth quarter of 2007. Singapore on the other hand, experienced a 1.5% decline in its second quarter GDP, compared with an increase of 3.72% in the first quarter, as shown in the second chart showing the period to period change in the seasonally adjusted data.

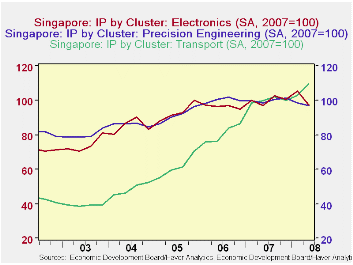

Singapore published data on production "clusters" about two weeks ago that suggested the slowing in the manufacturing sector would affect the second quarter GDP adversely. The third chart shows the indexes (2007=100) for three of the clusters: Electronics, Precision Engineering and Transport. The transport cluster continued to forge ahead in the second quarter but the Electronics and Precision Engineering clusters declined.

| SOUTH KOREA AND SINGAPORE | Q2 08 | Q1 08 | Q2 07 | Q/Q % chg | Y/Y % chg | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|---|

| South Korea Real GDP (Bil 2000 Won) | ||||||||

| Seasonally Unadjusted | 206813 | 193700 | 197403 | -- | 4.77 | 798057 | 760251 | 723127 |

| Seasonally Adjusted | 207532 | 205829 | 198125 | 0.83 | -- | -- | -- | -- |

| Singapore GDP (Mil Singapore Dollar) | ||||||||

| Seasonally Unadjusted | 58219 | 58503 | 57019 | -- | 2.10 | 229090 | 212626 | 196474 |

| Seasonally Adjusted | 58558 | 59688 | 57535 | -1.52 | -- | -- | -- | -- |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief