Global| Dec 10 2020

Global| Dec 10 2020French IP Index Still Lags Below Pre-Covid-19 Levels in October

Summary

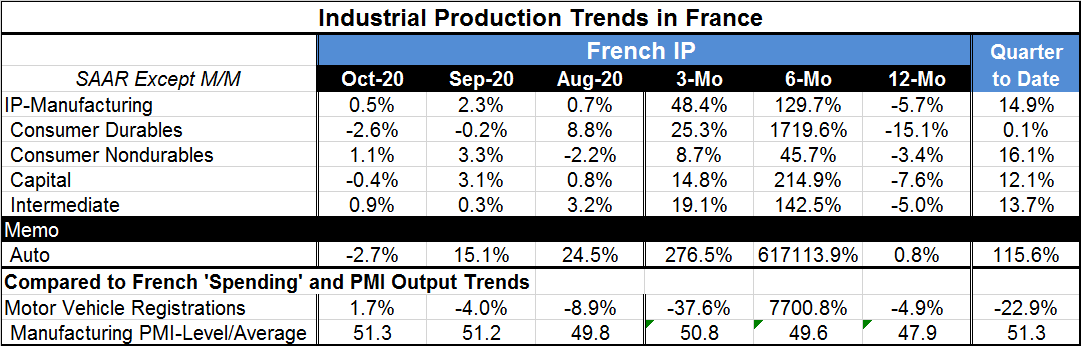

French manufacturing IP rose by 0.5% in October after a 2.3% gain in September. IP is up at a 48.4% annual rate over three months, at a 129.7% annual rate over six months and yet still lower by 5.7% over 12 months. Such has been the [...]

French manufacturing IP rose by 0.5% in October after a 2.3% gain in September. IP is up at a 48.4% annual rate over three months, at a 129.7% annual rate over six months and yet still lower by 5.7% over 12 months. Such has been the damage and destruction wreaked in trying to control Covid-19.

French manufacturing IP rose by 0.5% in October after a 2.3% gain in September. IP is up at a 48.4% annual rate over three months, at a 129.7% annual rate over six months and yet still lower by 5.7% over 12 months. Such has been the damage and destruction wreaked in trying to control Covid-19.

In the quarter-to-date, IP is rising at a 14.9% annual rate. The output of consumer durable goods is lagging while consumer nondurables is slightly leading the growth rate of other sectors with capital goods and intermediate goods output both at double digit rates of expansion.

Auto output and vehicle registrations have gone through a roller coaster of ups and downs with the table at this point only memorializing the ‘ups.' The Corona-19 virus and the lockdown to maintain its spread have put the French economy through an incredible stress-test of sorts as it did with much of the rest of the world. The auto data show this off the best. The manufacturing PMI data in the table are now smoothed and not showing any degree of the chaos that the virus helped to create. But the chart shows that the PMI gyrated in step with the index of industrial production in manufacturing.

France is currently embroiled in the end game of a second lockdown to curtail the next wave of virus. This second wave peaked with daily infections up to 88,790 on November 7, a huge step up from the 7,578 daily peak back at the end of March. But since early-November, the French infection rate has been steadily and rapidly falling. Although the total infection curve and the number deaths curves are still rising, the number of deaths is far below the numbers that the peaks reached back in April despite the far higher rate of infection in this wave! The comparisons are really quite striking.

These trends imply that a lot of has been learned about dealing with a treating the virus and that the virus must have killed a number of extremely vulnerable people the first time around. This time around in France, it is infecting people with stronger immune systems who can get infected and recover.

In any event, France is making progress and stemming the second wave and this success is putting the economy back into gear. Of course, the data from October do not begin to reflect the setbacks to economic data that are yet to be reported for November when the virus ran wild and when lockdown steps were taken. A nationwide lockdown was implemented in France on Wednesday, October 28 and was set to be in place for one month. This is the act that subdued the second wave's spread. All France's restaurants, bars and nonessential businesses were ordered shut down starting that very Friday, and French President Emmanuel Macron said people should return to full-time remote work wherever possible. These steps proved sufficient to reduce the infection rate sharply, but they also will have taken a toll on the economy in data we have yet to see.

We do not know if there will be a third wave in France. There has been a set of reinfections across Europe and currently in the United States. But there is a vaccine that is already being deployed in the U.K. and vaccines are being mooted for early use in the U.S. and in other countries. However, vaccine supplies will be scarce to start and it is not clear how long it will take before a large enough swath of the local populations is immunized to put the virus off its game. That will depend on a number of variables including the health officials' priorities in designating the order for inoculation from this scarce resource. Will they choose to inoculate to damp the spread the fastest… or to protect the most vulnerable first? Of course, front line hearth workers will get their doses before anything else is done.

For now the French economy is coming out of its second round of intensive care over the virus. It is re-normalizing. But the future is still clouded even with the presence of several effective vaccines that are ready to go. ‘Soon' we may be able to get back to considering economic matters using only economic analysis instead of constantly deferring to medical realities. But there may be another six or even nine months before that world opens up to us. Until it does, we are all at risk in one way or another.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief