Global| Aug 09 2013

Global| Aug 09 2013French IP Falls Unexpectedly

Summary

French industrial production fell by 1.4% in June, a surprising development that was largely unexpected. The optimism gene has spread in Europe; expectations are that Europe has turned the corner and that growth is going to continue [...]

French industrial production fell by 1.4% in June, a surprising development that was largely unexpected. The optimism gene has spread in Europe; expectations are that Europe has turned the corner and that growth is going to continue to proceed and, probably, to build momentum. And while the data show that something like this may be in progress, Europe is still in the fragile part of the turnaround and it's not clear that Europe has the momentum to sustain the upturn, nor is it clear that Europe can avoid the kinds of negative events that could create a definite setback.

French industrial production fell by 1.4% in June, a surprising development that was largely unexpected. The optimism gene has spread in Europe; expectations are that Europe has turned the corner and that growth is going to continue to proceed and, probably, to build momentum. And while the data show that something like this may be in progress, Europe is still in the fragile part of the turnaround and it's not clear that Europe has the momentum to sustain the upturn, nor is it clear that Europe can avoid the kinds of negative events that could create a definite setback.

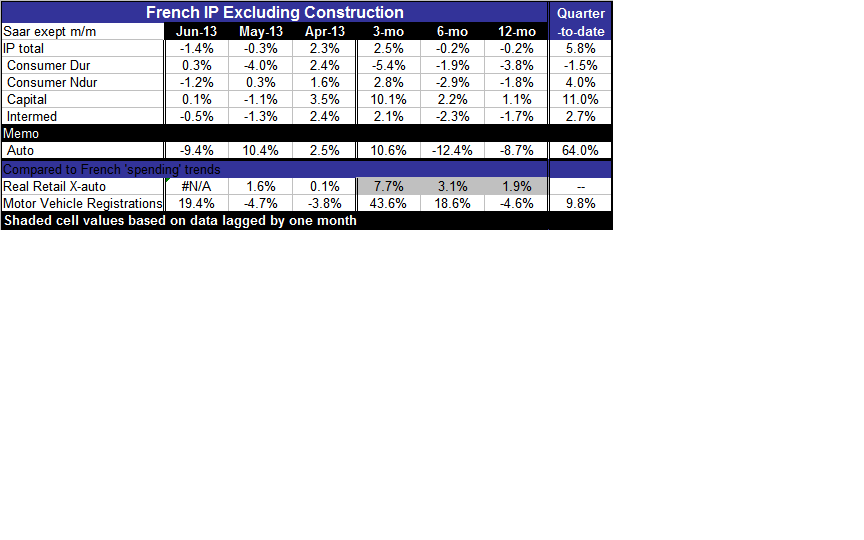

However, the 1.4% decline in French industrial production in June still leaves the three-month growth rate at a 2.5% annual rate with a -0.2% annual rate decline over six months as well as over 12 months.

In the month of June, French consumer durable output rose by 0.3% after falling by 4% in May. Consumer nondurable output fell by 1.2% after rising 1.3% in May. French capital goods output increased by 0.1% after a 1.1% a decline in May. Intermediate goods output fell by 0.5% putting in back-to-back declines after falling 1.3% in May.

Month-to-month data for France- as well as any other country - tend to be pretty volatile for industrial production. The 3-month growth trends bring a little more clarity to the patterns of French output along with the quarter-to-date metric now that the second quarter data are complete even though they're not finalized.

When we look at French data over three-months and over the quarter-to-date, the results are somewhat more reassuring. The quarter-to-date calculation is put on a comparable basis with the calculation for GDP; it looks at the percentage change of the average of industrial production for April, May and June over its average for January, February and March, annualized. It is a true annualized quarter over quarter calculation. As such it can be quite different from the three-month calculation which looks at the percentage change in June over the base in March, taking only those two months into account instead of all six-months of the two quarters.

The three-month growth rates show us that French industrial output, like German industrial output, is being led by the capital goods sector. Capital goods output is rising at a 10.1% annual rate over 3-months better than its 2.2% pace over 6-months and 1.1% rise over 12-months. This is a true acceleration. Intermediate goods output had been slipping, posting a -1.7% drop over 12-months, a -2.3% annualized rate of decline, over 6-months, but has now turned around to post a +2.1% annualized growth rate over 3-months. Similarly, consumer nondurable output is falling 1.8% over 12-months and falling at a 2.9% annual rate over 6-months but has turned around to grow at a 2.8% annual rate over 3-months. Consumer durable goods output in France is the step-child of growth: its growth rate is -3.8% over 12 months, that improved to -1.9% over 6-months but then it had a relapse and is now falling at a 5.4% annual rate over 3-months.

The quarter-over-quarter growth rates for French industrial production echoed the same trends. There, consumer durables output is down by 1.5% at an annual rate on the quarter, consumer nondurable output is up at a 4% annual rate for the quarter, capital goods output is up at a strong 11% annual rate for the quarter while intermediate goods output is up at a 2.7% annual rate.

The basic data for French output exclude the volatile construction sector which is a common comparison for countries in the Euro Area. While the drop in output in June was a surprise, the trend shows that that back-up is only moderate and is not reversing the building momentum in French industrial production across most sectors. The consumer durable goods sector remains the most troubled sector for French output.

Output of autos is always volatile, too. Auto output in June fell by 9.4% month-to-month after rising by 10.4% month-to-month in May. However, the auto sector is increasing output at a 10.6% annual rate over 3-months after falling at a 12.4% annual rate over 6-months and an 8.7% annual rate over the last 12-months. In the quarter-to-date, however, vehicle output is rising at a stunning 64% annual rate.

We can compare that to motor vehicle registrations in France. We see motor vehicle registrations rose 19.4% in June after falling 4.7% in May; they also fell by 3.8% in April. Motor vehicle registrations are up at a 43.6% annual rate over three months and 18.6% annual rate over six months; they are still falling by 4.6% year-over-year. But in the quarter-to-date motor vehicle registrations are rising to a 9.8% annual rate.

The trends in the chart above show that auto output in France definitely tends to follow the trends in motor vehicle registrations. Once registrations begin to perk up, output begins to turn around and once registrations have begun to cool off, output continues to rise as it tends to overshoot the trends in vehicle registrations. We see several examples of that in the chart. Currently registrations are in a rebounding phase even though the year-over-year growth rate is still negative. The monthly decline is becoming progressively smaller, and auto output has gotten out ahead of that improving trend. Some of that might also reflect the somewhat sharper improvement in auto demand outside France.

Vehicle registrations in the EU region are beginning to turn around, too. Month-to-month vehicle registrations in the EU were falling for six months in a row from March 2012 to September 2012; from October 2012 to February 2013 they cut that tendency to five out of six months; by May of this year that was reduced only three drops out of 6-months and in June of 2013 it's down to two drops in the past of six months.

The French turnaround has been a little bit behind that, although that's in part because French sales were not nearly as adversely affected from March to September of 2012 as they were in the Euro Area as a whole. Currently, vehicle registrations in France are off in only about half of the months going back to October 2012. Meanwhile, the year-over-year declines in vehicle registrations have been steadily trimmed from double digits from July 2012 to March 2013 to a current year-over-year decline of under 5% in June of 2013. That's progress. Meanwhile, French registrations are up in two of the last three months and at three of the last five months.

While France's consumer spending on (and output of) durable goods in general is lagging as we can see from the weak output of consumer durable goods, there are substantial improvements being made in the industrial sector for France. The auto industry is a reasonable barometer for economic recovery in most countries. In the US, for example, there has been a very steady increase in unit auto and truck sales from the bottom of the recession with the only clear aberrant fluctuation coming from the period of time when the government introduced its 'cash for clunkers program.' However, in the US case, unit sales seem to have slowed over the last 7-to-8 months.

In Europe, auto sales continue to be slow. Their year-over-year growth rate in the whole of the European Union is still negative and is still near double digits and a -9.3% rate. Still, that 9.3% decline represents a great deal of progress from the -20.3% year-over-year decline back in December 2012. The European Union, as a whole, has put four straight months of month-to-month auto registration increases together for the first time Since February 2011. France is part of that progress.

We will continue to monitor the auto sector as well as the rest of the European economies. Monthly setbacks are going to be part of the process. Even solid economic rebounds rarely give you monotonic output progression. Although the trends in France are encouraging and they are part of encouraging picture for all of Europe, there remain issues...

Having bent my need to the conventional wisdom of Europe and France being on the mend, I will recall that in the OECD leading indicator report yesterday France's indices were still struggling. France generally has made less budget progress than most of the other countries of the European monetary union as it did not adopt the austerity model and instead chose to keep much of its domestic spending in place, raising taxes instead of cutting back on government largess. And, despite that, we have French farmers protesting, smashing over 100,000 eggs daily which they say represents 5% of French daily production because they want a 5% production cut to help raise prices. Regulations requiring that they raise hens in larger cages are causing egg production to be more expensive.

France is one of the countries in the European Union the benefits disproportionately from the common agricultural policy (CAP). The policy provides price supports for farmers in the EU. What we see in France is that despite even greater difficulties around it, there doesn't seem to be much taste on the part of the French consumer or voter to suffer at all in silence. Protesting, revolution, and militant agriculturalists (egg smashing, in this case; at least it beats 'manure dumping,' which has been done in the past) are all part of the culture. So while we can look at and chronicle economic trends as turning up, we have to remember that France still has some significant fiscal progress to make, especially in comparison with other European Monetary Union members that already have 'been there' and 'done that.' And that's a good reason to remain wary on the prospects for a continuing French economic recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief