Global| Mar 10 2017

Global| Mar 10 2017French IP and Manufacturing PMI Show Some Weakening

Summary

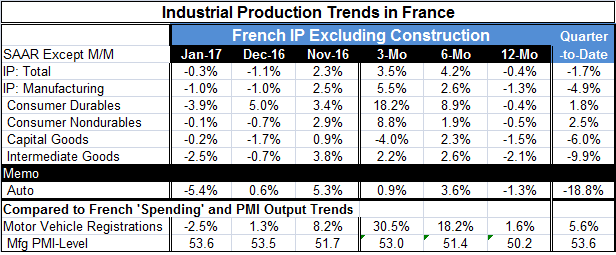

French industrial production fell unexpected in January, marking the second decline in IP in a row. Coming at a time when the Markit survey for manufacturing has been going up, that result was quite unanticipated. But once again, it [...]

French industrial production fell unexpected in January, marking the second decline in IP in a row. Coming at a time when the Markit survey for manufacturing has been going up, that result was quite unanticipated. But once again, it is a reminder that the Markit diffusion indices measure breadth not strength. Total output, manufacturing output, consumer nondurables output, capital goods output and intermediate goods output each show two back-to-back monthly declines. In that sense, the IP report also shows that output declines are broad-based and that the headline is not being dragged into negative territory by one rogue extremely weak sector.

French industrial production fell unexpected in January, marking the second decline in IP in a row. Coming at a time when the Markit survey for manufacturing has been going up, that result was quite unanticipated. But once again, it is a reminder that the Markit diffusion indices measure breadth not strength. Total output, manufacturing output, consumer nondurables output, capital goods output and intermediate goods output each show two back-to-back monthly declines. In that sense, the IP report also shows that output declines are broad-based and that the headline is not being dragged into negative territory by one rogue extremely weak sector.

Overall output, manufacturing output and output in each consumer goods category, that is all output except capital goods and intermediate goods is still showing output acceleration on growth rates from 12-month to six-month to three-month.

However, in the quarter-to-date which is still a nascent calculation, only consumer durables and consumer nondurables show increases in output. Quarter-to-date weakness is the result of having had a sharp run up in output in November. While December shows a drop in output that drop was smaller than the rise in November; now, the early readings for the first month in January show that these two months of readings have slipped compared to November and output readings for most French sectors now reside below their Q4 average.

Separately, auto output is not accelerating sequentially. In France motor vehicle registrations are still showing pent up demand and gathering acceleration from 12-month to six-month to three-month that is not reflected in a step up of auto production.

The Markit manufacturing PMI gauge has continued to move up across this time profile. The 53.6 level for the French manufacturing PMI in January is well above its 52.3 average for the fourth quarter despite the drop in January IP on the heels of a December drop. The PMIs continue to show that the manufacturing sector is gathering pace. But the IP data on the whole seem to show more holes. It is not just a matter of one month's difference or one category. IP trends show weakness for intermediate goods and capital goods. Meanwhile other questions come into play when we consider consumer spending.

Real retail sales for France are not in yet for January. But inflation adjusted French retail spending apart from autos moved up strongly in October then it failed to advance in November and backtracked in December. New real retail sales in Spain today showed a real sales decline creeping to the Spanish profile. Germany and the U.K. also have reported out January sales and both of them show declines. Despite the fact that optimism has been building in Europe especially over strong surveys and the Markit PMI results, there is evidence of a fly or two in the growth ointment for Europe.

The ECB met yesterday and made only minor policy alterations. But it is clear that as much as Draghi talked about the need to keep stimulus in play for now he also had an eye on a future with a much less accommodative policy in mind. I still do not see the critical mass of data piling up on the positive side of the ledger. There have been some positive reports, but there also are flaws and failure of strength to build on the initial appearance of strength. Growth conditions in Europe still need to be affirmed. Strength still needs to demonstrate that it can show up and stay.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief