Global| Dec 21 2016

Global| Dec 21 2016French Inflation Rises and An ECB Policy Dilemma Lurks

Summary

France is the perfect picture of the oncoming ECB dilemma. Inflation is rising (PPI here) but not so high. The PPI and core CPI (note sideways momentum in core CPI and mild uptrend in core PPI) show modest pressure on year-over-year [...]

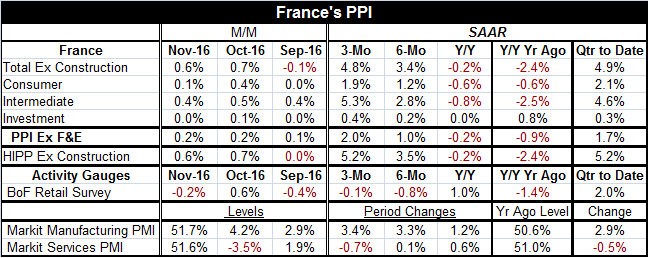

France is the perfect picture of the oncoming ECB dilemma. Inflation is rising (PPI here) but not so high. The PPI and core CPI (note sideways momentum in core CPI and mild uptrend in core PPI) show modest pressure on year-over-year trends. Yet, the domestic activity variables are not a source of price pressures; they are not showing much strength. The retail gauge for France (BoF) is still contracting and the Markit PMI gauge is showing only bare bones expansion for manufacturing and for services. As it is, the French MFG PMI is already surging well beyond the gains being recorded in the French index of manufacturing production. These facts mirror trends in the EMU region. Yet, the Bundesbank's Jens Weidmann is pounding on the table already about how the ECB must make its policy decisions solely on the basis of the inflation rate. To me, it's as though Weidmann is warning a starving man about eating too much when he is only looking at a picture of food. But that is the situation in Europe.

France is the perfect picture of the oncoming ECB dilemma. Inflation is rising (PPI here) but not so high. The PPI and core CPI (note sideways momentum in core CPI and mild uptrend in core PPI) show modest pressure on year-over-year trends. Yet, the domestic activity variables are not a source of price pressures; they are not showing much strength. The retail gauge for France (BoF) is still contracting and the Markit PMI gauge is showing only bare bones expansion for manufacturing and for services. As it is, the French MFG PMI is already surging well beyond the gains being recorded in the French index of manufacturing production. These facts mirror trends in the EMU region. Yet, the Bundesbank's Jens Weidmann is pounding on the table already about how the ECB must make its policy decisions solely on the basis of the inflation rate. To me, it's as though Weidmann is warning a starving man about eating too much when he is only looking at a picture of food. But that is the situation in Europe.

Reality bites- twice

There are at least two realities to the current inflation trend. One is that inflation remains low and below the ECB target as well as below central banks' objectives in nearly all major money center countries (i.e., no global inflation pressures). The second reality is that inflation also is rising and doing so somewhat rapidly. But it is rising from such a low base; it is still below the objectives or targets that central banks have established. The only exception to this 'rule' is in the U.K. where inflation is rising at an even more rapid pace and is boosted by the phenomenon of a weak and weakening currency making real inflation more of a palpable threat there.

The real dilemma part 1

On the surface, this seems to be a small and inconsequential dilemma about the waiting game. Since inflation is rising, it is just a matter of time before rates need to rise. And this seems to be the Weidmann approach. But if that is so, why is Mr. Weidmann so vociferous and why is he nagging the ECB before 'the fact' - by this I mean long before it is really even appropriate to hike rates? The answer is two-fold. One part is that the inflation in the EMU has undershot for a long time. There are probably EMU members that believe that a period of allowing some overshooting would be appropriate. Of course, no one with a Bundesbank pedigree would ever think such a thing. For one thing, policy is simply forward-looking inflation oriented and there is no sense in the ECB's 'charter' that the ECB is a price level targeting (although there is a reason you might think that). If there ever has been a period of overshooting, it has usually been followed by a period of undershooting that has kept 'average inflation' in line and consistent with the Bank's objective and mandate. But this is not enshrined as a policy directive. That ECB inflation soul be a little below 2% tells you where the ECB's bias lies.

The real dilemma part 2

The fact that the current inflation in the pipeline is mostly from oil is a separate issue over which policymakers might have different judgements as to the inflation risk. Because the inflation impulse is from oil, there may not be much impact on the core rate (ex food and energy). The Bundesbank has played the inflation game much like the Hawks at the Fed. While inflation has been low, the anti-inflation crowd has tended to try to direct attention to the core which has been higher and more stable. Or they have emphasized the growth in the central bank balance sheet as an eventual inflation risk. The minute that headline pace jumps over the core rate, the view will switch immediately the headline rate which is the only rate the ECB claims to focus on regardless of which hawkish bait and switch tactics are used by central bankers when they play a game of 'where's Waldo' with the inflation rate.

A good record in EMU so far

Among the original EMU members, only four of 11 have compounded rates of inflation greater than 2% per year since the EMU was formed. They are Luxembourg (2.4%), Spain (2.2%), Portugal (2.01%) and Ireland (2.01%). We could split hairs and say only two are noncompliant and one of these is a financial center where price competitiveness hardly matters. In the wake of all the imposed austerity, nearly every EMU member is now long-run inflation compliant- despite some with interim transgressions. Thus, in effect it has been as though the ECB has been price level targeting and as though nearly every country has too. Still, big differences in competitiveness have developed within the region because Germany has run inflation rates so far below the ECB mandate (1.48%). From its inception, the EMU (weighted) inflation rate has risen at a compounded rate of 1.7%. That is well within its mandate of a little less than 2%. In fact, it leaves the overall EMU price level some 5.5 percentage points below a strict 2% target path benchmarked to the date of the monetary rule's implementation. And while this bit of arithmetic seems to be indicative of a policy of price level targeting, the ECB only seems to apply the principle after inflation that has been too high. (To Bundesbank members, there is no such thing as inflation being too low.) That bias accounts for its undershooting.

French activity in profile

The French data show this set of facts very clearly. Activity has been weak; there is little real growth acceleration. A year ago retailing (BoF index) was down by 1.4% over 12-months, now the retail index is up by only 1% from this weak base over the past year and still showing declines on balance over three-months and six-months. The manufacturing PMI is an exception of sorts in the spirit of the same arguments as I made above. The manufacturing diffusion index from Markit is up by 1.2 points over 12-months but by over three points over three-months and six-months. It shows some momentum, but the index level for manufacturing is still stuck at 50.6, a value barely signaling any expansion at all. After a period of pronounced weakness, France is only barely showing Industrial production (IP) growth. For services, the story is much the same with the year ago services PMI at 51; now, one year later, it is only up to 51.6. Services are showing bare bones increases as well. The French economy has been and continues to be weak. Yet its PMI gauges show some upward momentum, but only a fool would fail to see this as a fragile phase of expansion. France will not want the ECB to be quickly reversing its easing mode.

French inflation trends

The inflation trends for France are shown in the table as well as on the chart. The chart shows that back as far as 2006 the French inflation rate has been below 2% with one moderate exception, roughly in 2008. Apart from that, French core CPI inflation has been below the 2% target set for the EMU as a whole. The PPI, a more volatile measure, had several runs above the 2% mark some of them quite substantial and even the PPI core had several significant overshoots. What matters for ECB policy, however, is the EMU-wide HICP - period! I use the data for France as an illustration and to point out the cross currents in the French economy which actually mirror the cross currents in the EMU. Also the graph illustrates that PPI moves are sometime unrequited in terms of CPI trends. Not every PPI bulge and dip gets translated into the CPI (or HICP). The pressure we see in the PPI may worry some, but may not turn out to be a cause for concern. By looking at past growth current trends and several inflation indicators, you can easily see how policymakers could sit down at the table with different views. Jens Weidmann wants one view only: that of inflation on the table and inflation to come.

The policy problem

Inflation hawks tend to react to and extrapolate from the potentially most disruptive result rather than from a consistent framework. One thing is clear, however, and this is that the ECB has undershot its target for a long time and the Bundesbank does not want that to be used as an excuse for any overshooting. This is the same sort of dilemma that seems to permeate the Fed. I calculate year-to-date inflation for the U.S. going back of over 25 years - a much longer period than the Fed has 'targeted' inflation. The year-to-date rate for the headline and core PCE, nonetheless, stays below 2% on all horizons over all year-to-date periods of 25 years or less. We have been for a quarter century in a period of price stability! For the Fed and for the ECB, their 2% (or just less than 2%) goal has been hit consistently (over 17 years for the ECB) and on a backward looking year-to-date basis. The ECB has reached its objective throughout its lifetime. And yet we have members of the Fed and ECB that want to forget history when setting policy today. At the same time, it is clear that growth is what has been lacking and that inflation is not even threatening even if some small overshoot were to occur. The main 'threat' is the potential for a shift in the relative price of oil to appear temporarily as an inflation bulge. Under any reasonable model of expectations formation, there is no basis for forming expectations of inflation above 2% in the major monetary center countries/regions- U.K. excepted. There is a near-term risk from OPEC and oil prices, but OPEC's record on controlling the cartel is so poor; I'm not even sure we can call OPEC a real threat. So, oddly, despite all the attempts at stimulus, based on outcomes, policy continues to err on the side of being too restrictive and that is a problem that central bankers need to think about. A policy meant to keep inflation at or just below 2%, but that tries instead to never let it rise to 2% or above could be one of the worst monetary policies to put in play during these times. You know, it's something to think about...yes, even in Germany.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief