Global| Oct 23 2019

Global| Oct 23 2019French industry Climate Hits Its Lowest Reading Since March 2015

Summary

The climate gauge for French industry fell to 99.4 in October from 101.6 in September, marking its lowest point since March 2015. French manufacturing claimed for a plateau of readings in early-2015 to a peak at 113.5 in January 2018. [...]

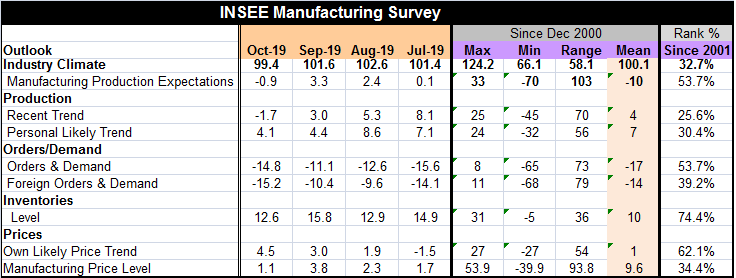

The climate gauge for French industry fell to 99.4 in October from 101.6 in September, marking its lowest point since March 2015. French manufacturing claimed for a plateau of readings in early-2015 to a peak at 113.5 in January 2018. The climate gauge then began to deflate and it deflated rather more rapidly late in 2018 and that erosion continues. Currently, the climate gauge sits at its 32.7 percentile, just in the bottom one third of its queue of observations since 2001.

The climate gauge for French industry fell to 99.4 in October from 101.6 in September, marking its lowest point since March 2015. French manufacturing claimed for a plateau of readings in early-2015 to a peak at 113.5 in January 2018. The climate gauge then began to deflate and it deflated rather more rapidly late in 2018 and that erosion continues. Currently, the climate gauge sits at its 32.7 percentile, just in the bottom one third of its queue of observations since 2001.

Reading down the right column of rankings, it is clear that there is a lot of moderation and weakness and not any strength to speak of in this survey. The queue percentile standings place each indicator in its historic queue of observations, ranking the current value according to its own history to produce a strong relative statement of where the indicator currently stands compared to where it has spent most of its time since December 2000. A few categories are in the 50% to 55% zone, a touch above their median standing for the period. The personal likely sales trend has a (nearly) top one-third standing. Inventories have the highest standing (unfortunately since that means the responses about inventory-building are still high at a time that the same responses for orders and production are lower). That situation for inventories signals an imbalance in the making.

All of the components are weaker in October than they were three-months ago in July except overall orders & demand and the likely price trend.

While manufacturing production expectations has an above median 53.7 percentile standing, the recent trend of production has a 25.6 percentile standing and the personal likely trend of production has a 30.4 percentile standing. These responses suggest that the expectation for production overall is more upbeat than the current trend and more upbeat than firms’ expectations for their individual situations.

Overall orders and demand have a slightly above-median reading, but foreign orders are much weaker and considerably below their historic median. France is getting weakness imported through its international channel.

Inventories continued to show building going on at a faster-rated pace that other activity components and that pace has not slowed much in recent months.

As to prices, firms are more upbeat on their own ability to raise prices ahead than they are expecting the price level in general to rise – they are about twice as upbeat on their prospects for price hiking compared to prospects overall.

Summing up

On balance, France shows that a good deal of weakness is in train. Momentum is for the most part negative and the current standings of important components are moderate-to-weak for the most part as well. These results for France strongly suggest that a wave of weakness is continuing to wash over the French economy as Europe braces for Brexit and as the ECB continues to fight over the degree of stimulus it is providing in the EMU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief